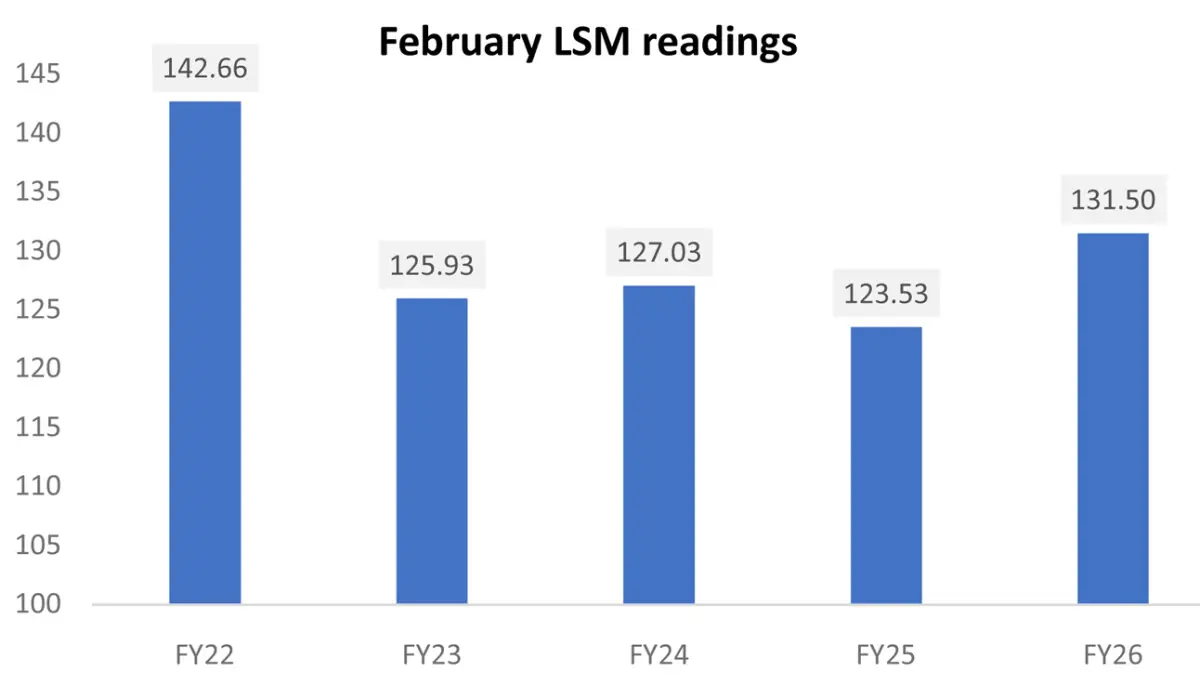

Large-Scale Manufacturing maintained its recovery in February 2026, though at a more measured pace. Year-on-year growth came in at 6.45 percent, taking cumulative expansion for 8MFY26 to 5.89 percent, broadly aligned with full-year expectations.

The February index reading ranks as the second highest ever for the month, trailing only FY22. That gap remains substantial, with the FY22 peak still about 11 percentage points higher, underlining the distance yet to be covered.

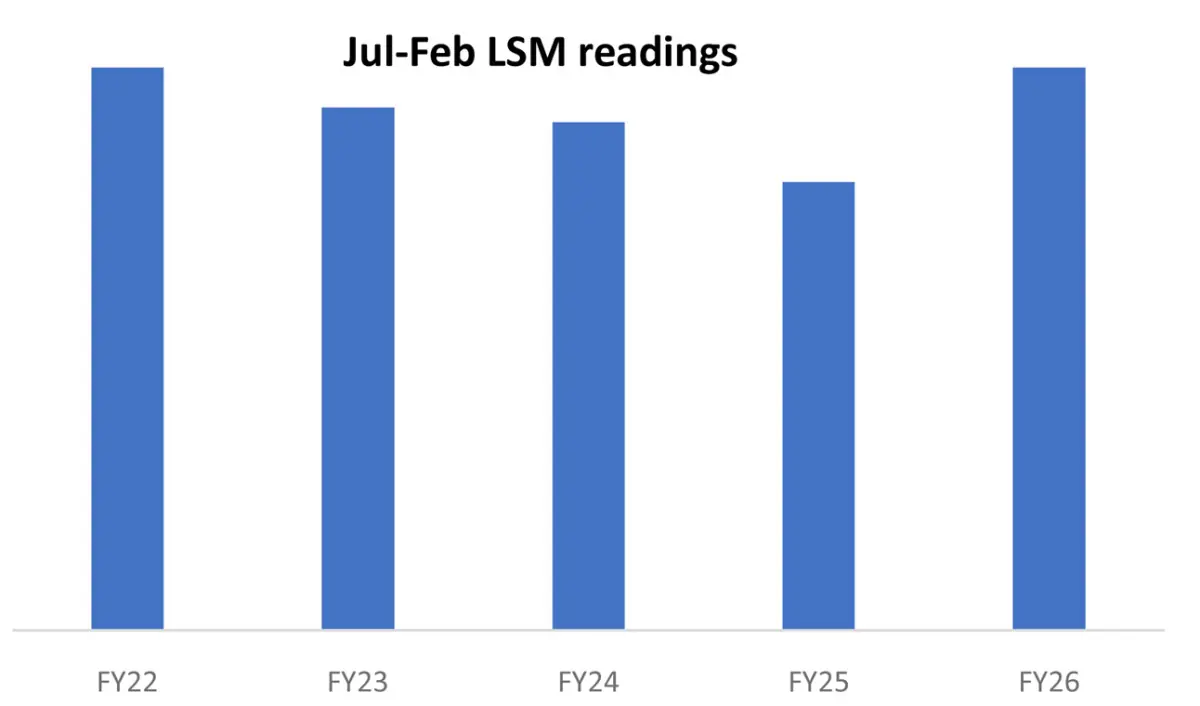

The cumulative picture continues to strengthen. The July to February index is also the second highest on record, only marginally below FY22 levels. More importantly, the recovery remains widely distributed.

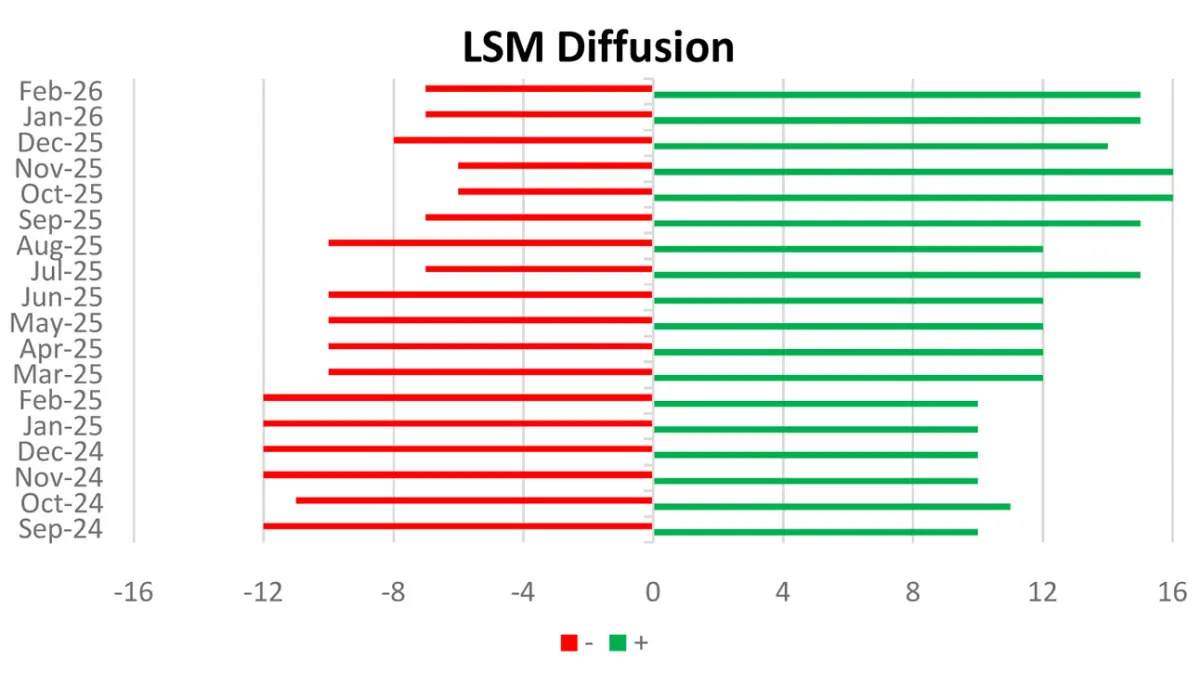

Fifteen of the 22 sub-sectors are now in positive territory, while the seven laggards are largely confined to low single-digit contractions and carry relatively smaller weights. The underlying structure of growth remains intact.

Food has moved decisively to the center of the current expansion. The February food index reached its highest level ever for the month, driven by another surge in sugar production. Output stood at 2.1 million tons, up 29 percent year-on-year, with cumulative production already about 14 percent higher and surpassing the entire output of the previous season. At the current pace, the industry is on track for a record year.

Food was the single largest contributor to February LSM growth, with its impact exceeding the combined contribution of all other expanding sectors.

Wearing apparel cooled after an exceptional January. Readymade garment exports reverted to more moderate levels, bringing cumulative growth for 8MFY26 to around 7 percent. Early indications for March suggest further moderation, with cumulative growth for 9MFY26 easing closer to 5 percent. The segment remains important, but its relative dominance has clearly tapered.

Automobiles continue to anchor cumulative performance, even as growth begins to normalize. Car production remains in double-digit expansion, though the high base effect is now visible.

On a cumulative basis, automobiles remain the largest contributor, followed by wearing apparel and food.

What stands out in the latest data is the continued diversification of growth drivers. Petroleum, beverages, and cement have all made meaningful contributions, reinforcing the shift away from a narrow, sector-led recovery. The base is now sufficiently broad to absorb moderation in any single segment without derailing overall momentum.

Forward signals remain cautiously supportive. Industrial electricity tariffs have declined to levels that are increasingly competitive, in some cases even undercutting alternative energy sources. This, combined with earlier easing in interest rates, is improving the operating environment for manufacturers.

External risks persist, particularly from the evolving geopolitical situation, but the impact so far appears contained and likely temporary.

The benchmark of FY22 remains out of reach. Matching those levels would require LSM growth to average around 23 percent over the remaining four months, an outcome that borders on unrealistic. Even so, the direction of travel is clear. Growth has settled into a more stable range, the base has widened, and the recovery is no longer reliant on isolated sectoral spurts.

Comments