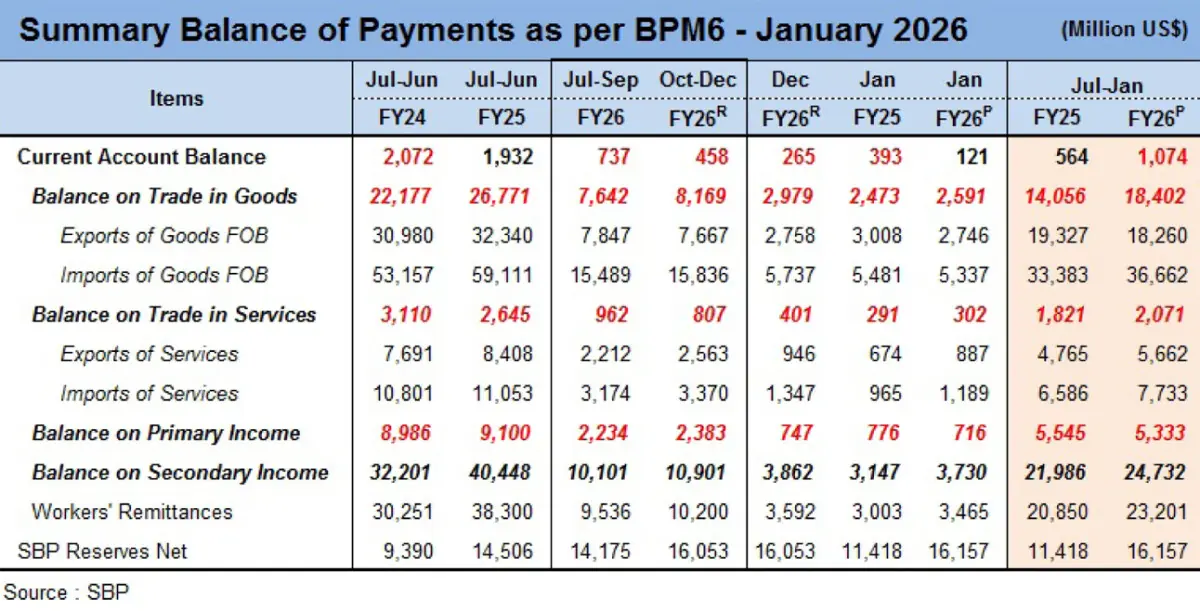

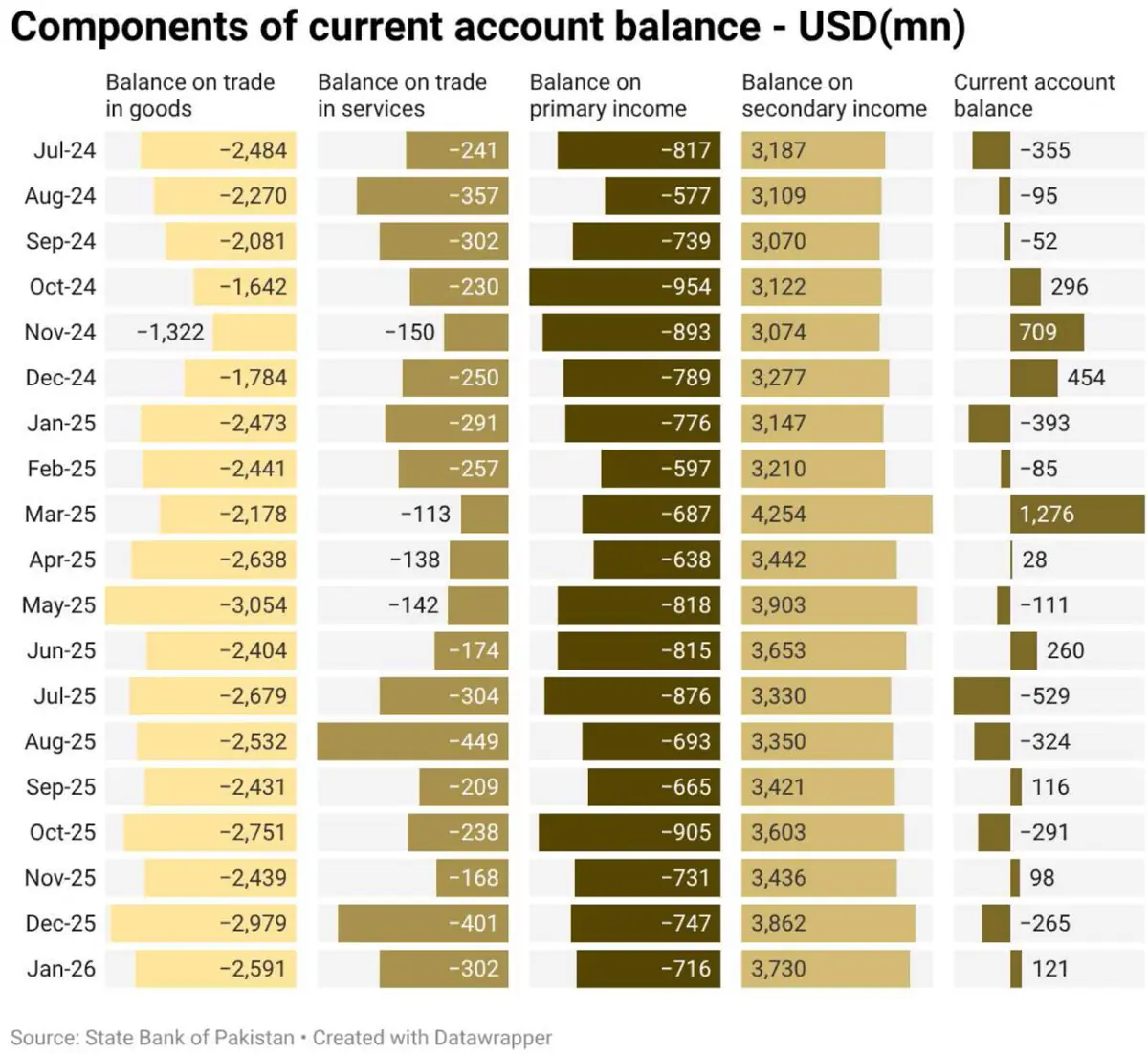

The current account keeps on oscillating between monthly marginal surpluses and deficits, as it posted a surplus of USD121 million in January 2026. Overall, in 7MFY26, the deficit stood at USD1.1 billion as compared to a surplus of USD564 million in the same period last year.

In the calendar year 2025, the current account was almost in balance (USD0.2 bn deficit), however, that was not sufficient to increase the reserves net of debt – as SBP reserves are up by USD4.3 billion while the external debt and liabilities are up by USD7.2 billion. This is even though SBP bought USD5.2 billion from the interbank market during 2025.

The anomaly of SBP buying while debt growth outpacing reserves growth despiteno current account deficit is explained by weakening USD (as other currencies debt grew in dollar terms) and higher profit repatriation at USD2.4 billion on already accrued amounts in 2025.

The bottom line is that current account balance proved to be not sufficient to increase reserves.

That reality is to compel SBP to keep on buying from the interbank and not let current account deficit grow by keeping tight monetary policy or letting the currency depreciate.

The problem is that exports – mainly goods exports, are not performing up to the expectations despite the government having a stated policy of having export led growth. Goods exports dipped by 6 percent to USD18.3 billion in 7MFY26.

The biggest dent is in food exports – plummeted by 35 percent to USD2.7 billion.

Rice exports are down by 42 percent or USD790 million in 7MFY26 -India is back in the exporting market which has a double whammy for Pakistan, as its not only taking Pakistan’s enhanced share but also resulting in dip in the international prices.

The cherry on top is closure of Afghanistan border further hampering rice and other food items exports.

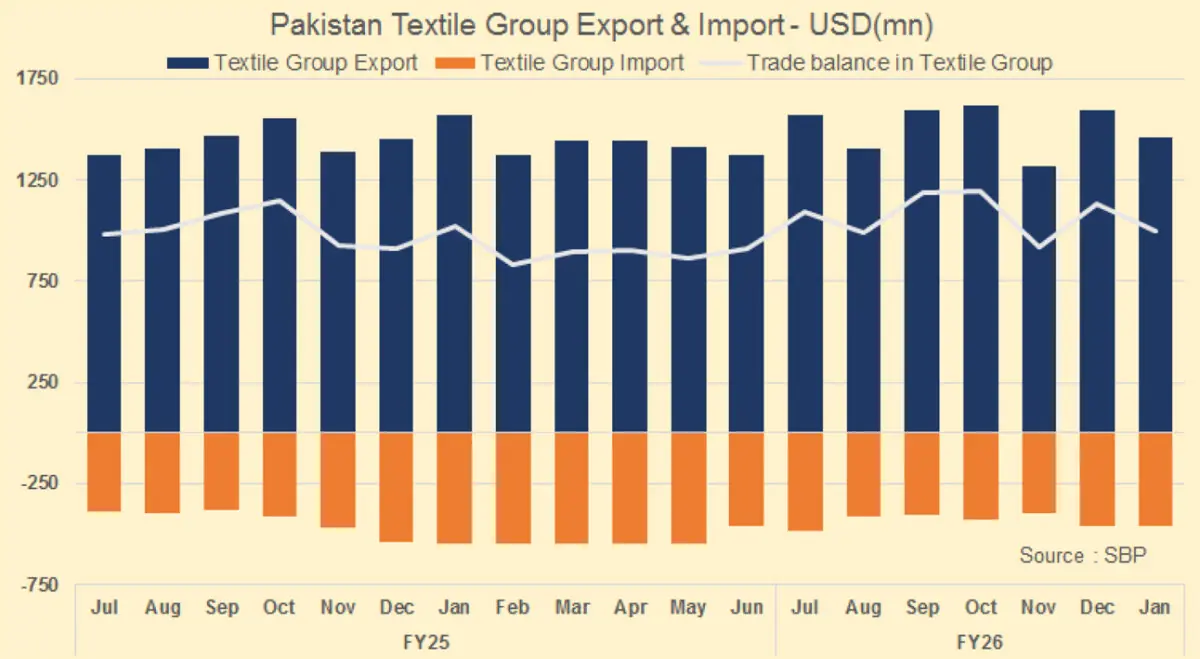

Textile exports marginally up by 3 percent to USD10.6 billion- within cotton cloth exports are down by 12 percent while value added knitwear,bedwear and readymade garments are up by 10 percent, 5 percent and 6 percent respectively.

Although the value-added exports are increasing, which is encourging, overall growth is largely muted due to increasing competitionand shrinking market size.

On the flip, imports are rising despite overall suppressed commodity prices. Good imports are up by 10 percent to USD33.4 billion in 7MFY26.

Unlike food exports, which are dipping, food imports are up by 18 percent to USD4.9 billion in 7MFY26.

The biggest component is palm oil – up by 16 percent to USD2.2 billion– based on PBS data, palm oil quantity imports jumped by 21 percent which is higher than normal growth suggesting that formality in the sector is growing.

Overall food trade deficit stood at USD2.2 billion in 7MFY26 as compared to a mere deficit of USD31 million in the same period last year.

The overall economic growth is picking up, which is evident from 9.4 percent growth in LSM in the 1HFY26 and that is translating into higher imports for mobile phones and automobiles.

The former (based on PBS data) is up by 31 percent to USD1.1 billion – within it (based on SBP data) CBU mobile phones imports are up by 163 percent to USD186 million, as perhaps more I-phones are being imported.

Automobiles growth is outpacing every other sector – transportation imports are up by 106 percent to USD2.0 billion. The highest jump is in CBU busses and other heavy vehicles –increased by 8.2 times to USD194 million.

The biggest component is CKD cars – up by 87 percent to USD1.1 billion – which is visible from numerous newly launched cars being embraced by consumers.

The saving grace is in petroleum products which are dipped by 7 percent to USD8.3 billion in 7MFY26. This is mainly due to lower oil prices – dipped by 15 percent (on average) in 7MFY26 as compared to the same period last year.

Overall petroleum crude and products quantity imports inched up by 17 percent and 8 percent respectively.

Despite lower prices, overall goods trade deficit worsened by 31 percent to USD18.4 billion while the increase in services trade deficit stood at 14 percent to reach USD2.1 billion.

The services exports keep on growing – up by 17 percent to USD7.7 billion – within it both ICT and other business are moving at a decent pace – up by 20 percent and 26 percent to USD2.6 billion and USD1.2 billion respectively.

Nonetheless, the savior to the balance of payment is nothing else than home remittances which is breaking all the records – ity is up by 11 percent on a high base to USD23.2 billion. It is approaching 10 percent of GDP – highest in the country’s history and biggest in countries over 100 million population.

There is nothing to talk about FDI or any other capital or financial account variables. FDI is down by 54 percent to USD787 million in 7MFY26 while general government receipts stood at USD668 million as compared to an outflow of USD327 million in the same period last year.

The overall balance of payment situation is being dominated and controlled by home remittances where too much reliance is resulting in a concentration risk.

The government should work on enhancing exports, otherwise, remittances and imports may keep on moving in tandem and keep the policy makers on toes.

Comments