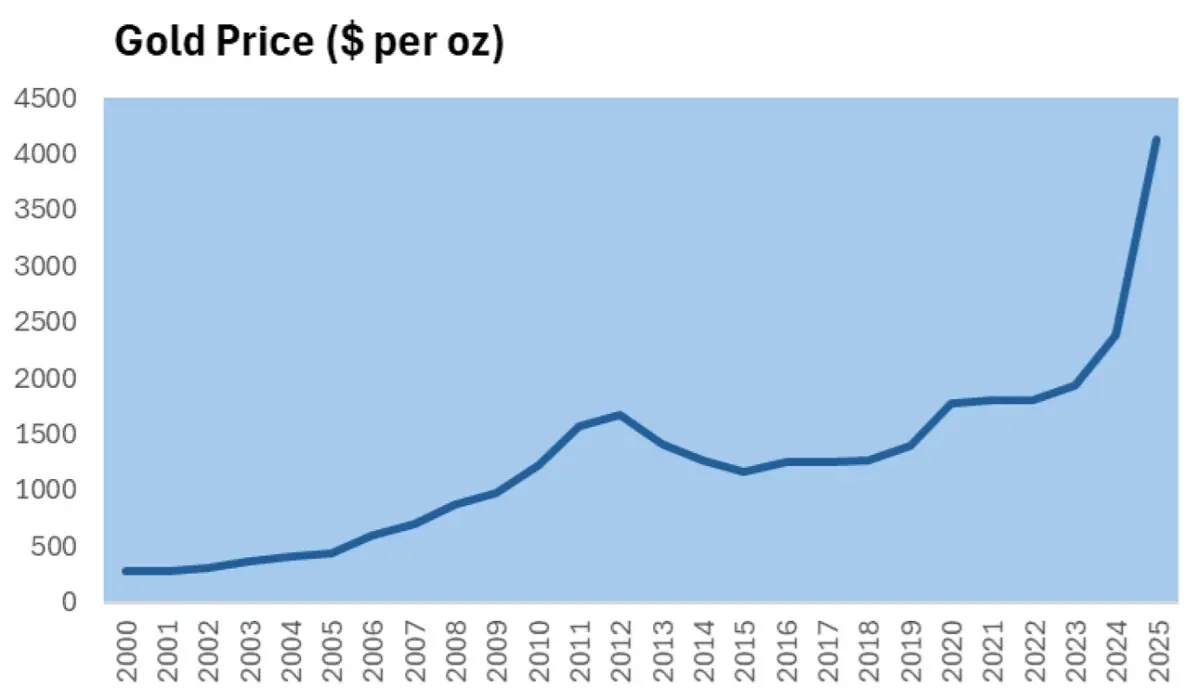

2025 was a record year for gold — not just in price, but also in demand. And this wasn’t simply a standard “safe-haven rally.” It looked more like a full repricing cycle, driven by strong demand at a time when global supply barely moved. The LBMA (PM) gold price set 53 new all-time highs during the year.

The annual average price climbed to around $3,431/oz (up 44 percent year-on-year), while the Q4 average rose further to $4,135/oz (up 55 percent year-on-year), showing how sharply momentum strengthened toward the end of the year. The World Bank described the rally as a classic response to rising uncertainty — fuelled by geopolitical tensions, economic concerns, a weaker US dollar, and supportive monetary conditions — and noted that 2025 was one of the strongest gold rallies since the late 1970s.

The demand story is what really explains the year. According to the World Gold Council (WGC), total gold demand in 2025 crossed 5,000 tonnes for the first time, while the total value of demand reached around $555 billion, up 45 percent year-on-year. A large part of this came from investors.

Gold ETFs saw one of their strongest years, and bar and coin buying climbed to a 12-year high. Central banks also stayed active, continuing to buy gold as a long-term hedge and diversification tool. Jewellery demand, meanwhile, did what it usually does when prices surge — volumes fell. But the important detail is that jewellery demand value still hit a record, which suggests consumers were buying fewer grams, not abandoning gold entirely. Technology demand also stayed steady, with WGC noting resilience supported by AI-related applications.

On the supply side, the response was surprisingly limited. In most commodity markets, a big price jump pulls in new supply quickly. Gold didn’t behave that way in 2025. Total supply rose by only about 1 percent, mine production was only marginally higher, and recycling increased only slightly despite record prices.

The simple takeaway is this: gold prices surged because investors and central banks kept buying, supply stayed tight, and jewellery absorbed the adjustment by buying less in volume. This also fits neatly with the World Bank’s broader point — when uncertainty rises, gold tends to rally because demand rises faster than supply.

Gold has remained elevated and volatile in early 2026, and the same forces are still doing most of the work. When interest rates fall, gold becomes more attractive, and when the US dollar weakens, gold becomes cheaper for buyers outside the US. WGC also points to continued geopolitical tensions, ongoing investor diversification, and supportive financial conditions as reasons investment demand could remain strong through 2026. Another theme that has gained attention is the idea that governments are increasingly building reserves of strategic commodities, including gold — which can keep prices supported, but also make the market more volatile.

READ MORE: Gold, silver most secure choices for investments?

Looking ahead, WGC expects 2026 to remain broadly supportive for gold. It expects investment demand to stay firm through ETF inflows and strong bar and coin buying, while central bank purchases are likely to remain solid and close to 2025 levels. Jewellery volumes may remain under pressure if prices stay high, even if spending holds up in value terms. On the supply side, WGC expects only a modest response, with mine output and recycling broadly similar to 2025. The World Bank’s Commodity Markets Outlook also projects precious metals to hit new all-time highs in 2026, supported by safe-haven demand and central bank buying — though it expects gains to be slower than the extraordinary run seen in 2025.

Major banks are also generally constructive on gold for 2026, largely because they expect investor inflows and central bank demand to keep the market supported. Reuters reports that UBS raised its targets to $6,200/oz for parts of 2026 and expects around $5,900/oz by end-2026, with a wide range of $7,200 (upside) to $4,600 (downside). Deutsche Bank has pointed to gold moving toward ~$6,000/oz if investment demand remains strong, while Goldman Sachs raised its end-2026 forecast to $5,400/oz. Still, the outlook is not one-way. As the World Bank notes, risks remain large: renewed geopolitical escalation or policy uncertainty could push prices higher, while a more hawkish US monetary stance or easing geopolitical tensions could cool demand and lead to a period of consolidation.

Comments