Quice Food Industries Limited (PSX: QUICE) was incorporated in Pakistan as a private limited company in 1990. The company’s status was changed into a public limited company in 1993.

The company is principally engaged in the manufacturing and sale of jam, jelly, syrups, pickles, essences, custard powder, juices and aerated drinks as well as other related products. Besides catering to local market, the company has its exports business in USA, Canada, UAE, South Africa, East Africa, UK and Australia.

Pattern of Shareholding

As of June 30, 2025, QUICE has 98.462 million shares outstanding which are held by 4453 shareholders. General public, with a stake of 62.92 percent, forms the largest shareholder category of QUICE followed by sponsors and their family members holding 31.88 percent shares.

Banks, DFIs and NBFIs account for 5.10 percent shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-25)

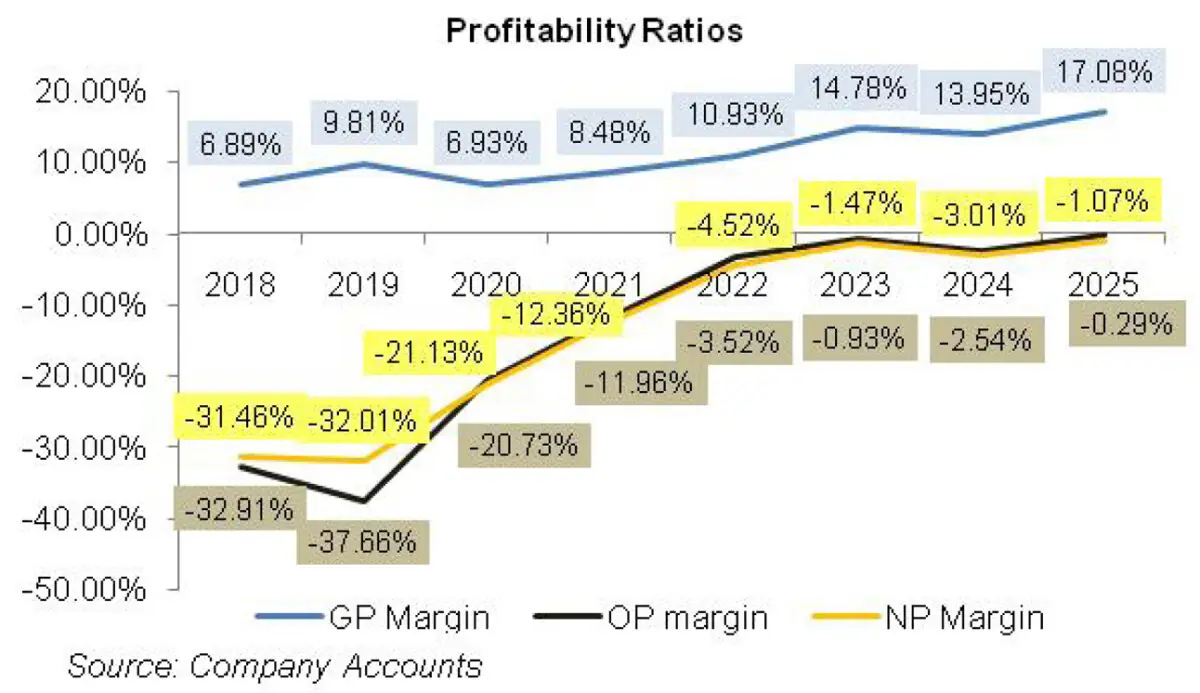

Except for a marginal dip in 2019, the topline of QUICE registered growth in all the years under consideration. Yet, the company was unable to post net profit and operating profit after 2015. The only happy sight is that the gross margin of the company which dipped in 2020 started improving thereafter.

In 2024, GP margin posted a dip followed by attainment of its optimum level in 2025. Furthermore, the magnitude of net losses which had been diminishing since 2021 massively grew in 2024 followed by a contraction in 2025. A detailed financial analysis of each of the period under consideration is given below.

In 2019, QUICE’s topline registered a year-on-year drop of 8.39 percent to clock in at Rs. 116.78 million. This was owing to overall economic slowdown. Not only did the local sales of the company post a slump, export sales also nosedived during 2019. Low volumetric sales resulted in 11.26 percent drop in cost of sales.

Eventually, the company was able to post GP margin of 9.81 percent in 2019, up from GP margin of 6.89 percent posted in 2018 with gross profit in absolute terms posting year-on-year rise of 30.45 percent in 2019.

Distribution cost dropped by 7 percent in 2019 due to a massive drop in advertisement expense.

However, administrative expense didn’t give any breather, thanks to inflationary pressure. Other expense also rose by 68.50 percent mainly because of re-measurement loss on investment and deficit on the revaluation of building. While other income rose by 24.63 percent year-on-year in 2019 on the back of investment income and profit on savings accounts.

However, it was too small in absolute terms to create any impact on the bottomline. Finance cost of the company was negligible and comprised of bank charges only.

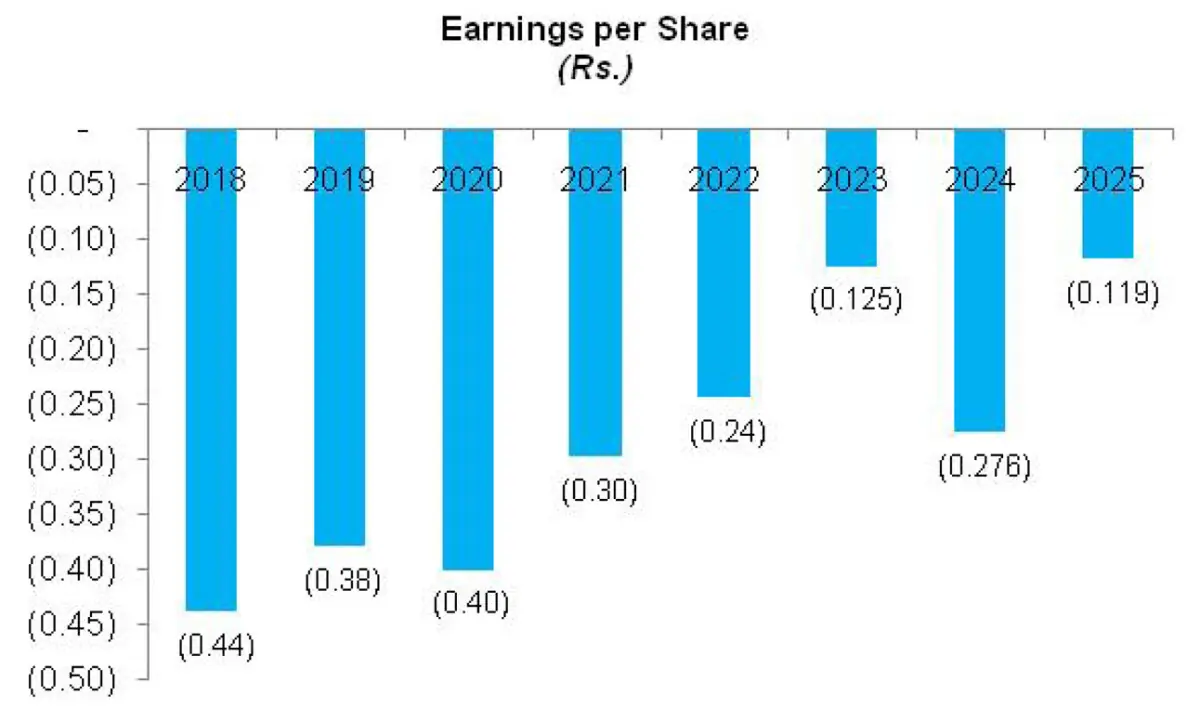

QUICE posted net loss of Rs.37.38 million in 2019, signifying year-on-year drop of 6.81 percent. Loss per share clocked in at Rs.0.38 in 2019 versus loss per share of Rs.0.439 recorded in 2018.

In 2020, QUICE’s topline grew by 59.87 percent year-on-year to clock in at Rs.186.69 million. This was mainly on the back of company’s increased focus on export sales. While local sales boasted a year-on-year increase of 32 percent in 2020, export sales multiplied by 577 percent with primary focus on UK, South Africa and Mauritius region. High cost of sales due to staggering rise in the commodity prices coupled with Pak Rupee depreciation magnified the cost of sales, resulting in a drop in GP margin to 6.93 percent in 2020.

Gross profit, in absolute terms, managed to increase by 12.90 percent during the year. 30.61 percent year-on-year rise in distribution cost came on the back of increased marketing expenses and outward freight and handling charges incurred during the year. Administrative expense declined by 22.73 percent in 2020 as the company streamlined its workforce to 45 employees from 112 employees in the previous year. The company was still not able to make operating profit.

Operating loss for 2020 clocked in at Rs. 38.69 million, down 12 percent year-on-year. The favorable movement of other income and an unfavorable movement of finance cost couldn’t produce any significant impact on the bottomline. The company posted net loss worth Rs.39.44 million in 2020, up 5.53 percent year-on-year. Loss per share stood at Rs. 0.401 in 2020.

In 2021, QUICE’s topline grew by 27.31 percent year-on-year to clock in at Rs.237.68 million. This was mainly on the back of a historic 62 percent growth in the syrup segment of the company owing to its induction in the modern trade markets. Cost of sales grew by 25.19 percent year-on-year in 2021, however, with the rising export sales and depreciation of Pak Rupee, the company was able to record a GP margin of 8.48 percent in 2021.

The company was able to keep a check on its operating expenses which enabled it to lower its operating loss by 26.56 percent year-on-year to Rs.28.42 million in 2021. Other income also boasted a tremendous 73.41 percent year-on-year growth mainly on the back of re-measurement gain on investment as well as capital gain. Finance cost dropped by 37 percent year-on-year in 2021. Net loss of the company stood at Rs.29.37 million in 2021 signifying a 25.54 percent year-on-year drop since previous year. Loss per share clocked in at Rs.0.298 in 2021.

In 2022, QUICE witnessed a stunning 123.94 percent year-on-year growth in its topline which clocked in at Rs.532.24 million. The export sales of the company rose by 150 percent year-on-year in 2022 to clock in at Rs.194.35. Local sales also doubled during the year to clock in at Rs.410.933 million. Unprecedented level of inflation experienced by the country during the year took its toll on the cost of sales which multiplied by 117.94 percent in 2022.

However, better off-take and improved pricing enabled QUICE to post GP margin of 10.93 percent in 2022. In absolute terms, gross profit strengthened by 188.63 percent in 2022. Operating expense grew relentlessly in 2022 owing to inflationary pressure which drove up the salaries and wages expense.

QUICE also expanded its workforce to 111 employees in 2022 versus 55 employees in the previous year Moreover, outward freight and handling expense, distribution claim, marketing expense etc also played a pivotal due role in inflating the operating expense in 2022. QUICE’s operating loss clocked in at Rs. 18.71 million in 2022, showing a downtick of 34.16 percent over last year.

Other income dropped by 68.57 percent in 2022 as company recognized investment income, capital gain and re-measurement gain on investment in 2021 which wasn’t there in 2022. Net loss stood at Rs.24.04 million in 2022, down 18.15 percent year-on-year with loss per share of Rs.0.244.

2023 also proved to be a significant year for QUICE with 57.53 percent year-on-year enhancement in its topline which stood at Rs.838.45 million. Topline growth was mainly driven by export sales which grew by 119 percent in 2023 to constitute 45.42 percent of the gross sales of QUICE in 2023 versus its share of 35.11 percent in 2022. Local sales also mounted by a reasonable 24 percent in 2023.

Cost-push increase in prices as well as Pak Rupee depreciation allowed QUICE to record a stronger GP margin of 14.78 percent in 2023. Gross profit also boasted a tremendous year-on-year growth of 113 percent in 2023. 100.47 percent surge in distribution expense in 2023 was the effect of higher salaries of sales force as well as hike in outward freight and handling mainly because of export sales picking up at an exponential pace and spike in the prices of petroleum and related products.

Administrative expense also surged by 23 percent in 2023 on account of higher payroll expense as QUICE increased its workforce to 189 employees in 2023 versus 111 in 2022. Moreover, higher travelling and communication expense and utilities also pushed the administrative expense up in 2023. Operating loss slid by 58.22 percent in 2023 to clock in at Rs.7.82 million.

Other income greatly buttressed QUICE’s financial performance in 2023 as it multiplied by 308.98 percent due to robust performance of both financial and non-financial assets. Bank charges (finance cost) grew by 282.86 percent in 2023 to clock in at Rs.0.4 million. QUICE was able to trim its net loss by 48.70 percent in 2023 to clock in at Rs.12.33 million with loss per share of Rs.0.125.

In 2024, QUICE posted topline growth of 7.73 percent. Net sales clocked in at Rs.903.26 million in 2024. The growth was led by export sales which posted 42.72 percent year-on-year growth in 2024 and constituted 67.13 percent of the company’s total sales.

In 2023, export sales contributed 45.42 percent of the gross sales of QUICE. The staggering growth recorded by export sales in 2024 was greatly offset by 28 percent decline in local sales due to sustained period of high inflation which brutally took its toll on the purchasing power of consumers. Cost of sales mounted by 8.77 percent in 2024 mainly on account of exorbitant energy cost. Gross profit inched up by 1.71 percent in 2024, however, GP margin dipped to 13.95 percent.

Greater export sales resulted in higher freight charges and increased salaries of sales force. This pushed the distribution expense up by 12.78 percent in 2024. Administrative & general expenses mounted by 13.93 percent in 2024 due to higher payroll expense on account of inflationary pressure. QUICE’s operating loss magnified by 193.45 percent to clock in at Rs.22.94 million in 2024. Other income inched up by 9.3 percent in 2024 due to higher income from saving accounts.

Finance cost which comprised of bank charges plunged by 68.10 percent in 2024. The company posted net loss of Rs.27.145 million in 2024, up 120.14 percent year-on-year. This translated into loss per share of Rs.0.276 in 2024.

In 2025, QUICE’s topline posted a decent year-on-year growth of 21.20 percent to clock in at Rs.1094.76 million. This mainly came on the back of a tremendous 74 percent growth in local sales which clocked in at Rs.760.991 million in 2025.

Conversely, export sales ticked down by 9.37 percent to clock in at Rs.549.514 million. Decline in export sales was the result of geopolitical tensions in the Middle East and Ukraine coupled with higher energy cost and stronger Pak Rupee which made the company’s products lesser competitive in the global market.

QUICE was able to record 48.42 percent stronger gross profit in 2025 on the back of robust local volumes and cost control measures implemented during the year. GP margin accomplished its highest value of 17 percent in 2025. Distribution expense surged by 30.59 percent in 2025 mainly on account of higher salaries of sales force and elevated marketing expense incurred during the year.

Administrative expense also escalated by 19.87 percent in 2025 due to higher payroll expense, utility expense, fee, subscription and professional charges as well depreciation expense stemming from capital expenditure on expansion projects. The company expanded its workforce from 166 employees in 2024 to 185 employees in 2025.

Operating loss slid by 86.10 percent to clock in at Rs.3.19 million in 2025. Other income ticked up by 7.74 percent in 2025 due to higher profit from saving accounts. Bank charges shrank by 51.42 percent in 2025. QUICE recorded net loss of Rs.11.73 million in 2025, down 56.78 percent year-on-year. This translated into loss per share of Rs.0.119 in 2025.

Recent Performance (1QFY26)

QUICE recorded 52.67 percent higher net sales to the tune of Rs.425.74 million in 1QFY26. This came on the back of splendid increase in both local and export sales over the quarter. Gross profit enhanced by 55.96 percent in 1QFY26 with GP margin clocking in at 19.43 percent versus GP margin of 19 percent recorded in 1QFY25. Despite high prices of raw and packing materials, utility charges as well as freight, insurance and handling charges.

The company was able to sustain its GP margin by attaining greater sales volume and undertaking strategic increase in prices. Distribution expense and administrative expense hiked by 70.52 percent and 25 percent respectively in 1QFY25. This was in line with expansion in production and sales.

QUICE boasted operating profit of Rs.7.783 million in 1QFY26, up 36.95 percent year-on-year. This translated into OP margin of 1.83 percent in 1QFY26 versus OP margin of 2 percent recorded in 1QFY25. Other income deteriorated by 34.91 percent in 1QFY26 due to lower profit on saving deposits on account of monetary easing.

Bank charges increased by 366.17 percent in 1QFY26. Net profit enhanced by 187.35 percent to clock in at Rs.3.539 million in 1QFY26. This translated into EPS of Rs.0.036 in 1QFY26 versus EPS of Rs.0.013 recorded in 1QFY25. NP margin ticked up from 0.44 percent in 1QFY25 to 0.83 percent in 1QFY26.

Future Outlook

As the company embarks on its journey to tap new geographical markets and new product lines, its margins are expected to rebound. Cost controls on the basis of better relationship with the suppliers, better pricing strategy, and stability in global commodity prices as well as steadiness in Pak Rupee are all the factors that hint of improvement in the company’s financial performance in the coming times.

Comments