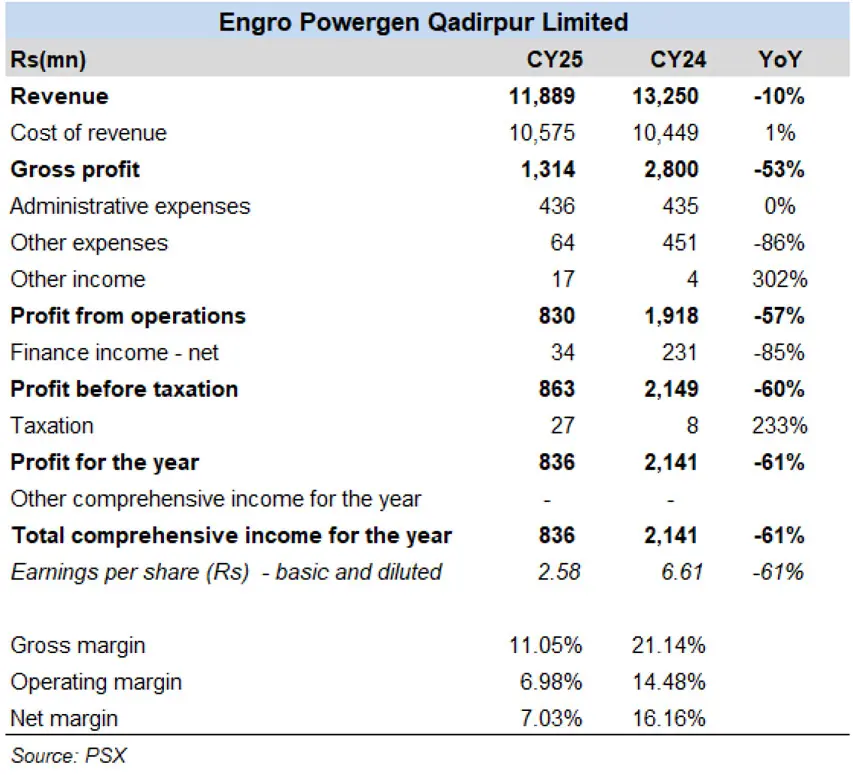

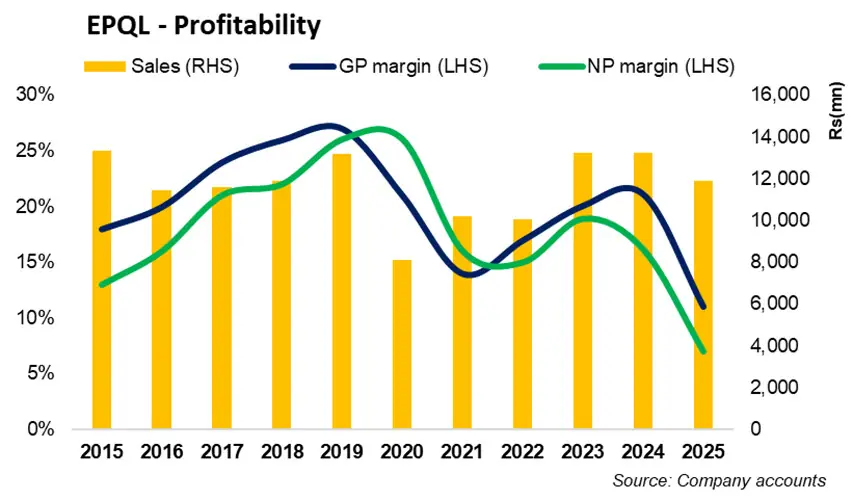

In CY25, Engro Powergen Qadirpur Limited (PSX: EPQL) remained profitable but posted a year-on-year earnings decline. Revenue fell to Rs11.9 billion by 10 percent year-on-year in CY25, largely due to a major scheduled outage and lower capacity payments under the hybrid take-and-pay model.

With weaker topline support and margin pressure, gross profit dropped by 53 percent year-on-year during the year, while profit before tax fell by around 60 percent year-on-year. Profit after tax declined to less than a billion, falling by 61 percent year-on-year in CY25.

However, CY25 was more of a clean-up year despite weaker earnings. A key development in CY25 was balance-sheet repair and liquidity normalization.

According to the company, EPQL received a Rs7.4 billion bullet payment in the first quarter of the year under the broader IPP settlement context, which materially eased working-capital pressure.

Overdue receivables from the power purchaser declined sharply to around Rs1 billion by Dec-25, compared with Rs6.6 billion at Dec-24. The company also cleared overdue payables to key gas suppliers, including SNGPL and PEL, reducing cash-flow strain across the operating cycle.

A notable strategic signal was the strength of shareholder payout. The company used improved liquidity, not stronger earnings momentum, to support shareholder returns in CY25. EPQL announced a total CY25 dividend of Rs11.75 per share (including a final Rs1.25 per share), which appears robust relative to reported earnings and was record annual payout for the company.

Operationally, EPQL’s performance was mixed but not weak in quality terms. Reliability remained strong, with a 100 percent billable availability factor in CY25, while net electrical output stood at 774 GWh. However, load factor eased to 42 percentin CY25 from 45 percent last year, mainly because of the scheduled maintenance outage.

The company strengthened its mixed-fuel plan by securing additional PEL low-BTU gas with formal NOC approval, which helped keep generation stable as permeate gas declined. EPQL’s merit-order positionalso kept it cost-competitive compared with imported-fuel plants.

CY25 was a reset year for EPQL: earnings dropped, but financial risk improved meaningfully. Outlook for the company in the coming year(s) is cautiously positive: EPQL has less cash pressure now, and if new local gas supply rises as planned, higher plant use can drive earnings recovery.

Comments