Financing fiscal deficit and lending to private sector: ineffectiveness of monetary policy

The Monetary Policy Committee decided to keep the policy interest rate unchanged at 10.5 percent, marking an aggregate decline of 11.5 percent in the policy rate since May 2024. However, the transmittal of this interest rate into investment activities, industrialization, and employment opportunities is a big question mark.

The most significant barrier to the transmission of monetary policy is the flow of domestic credit from commercial banks to the federal government to finance its budget deficit. Banks generally prefer risk-free lending to the government over financing the private sector, because it is an easy option for the banks to invest in government securities without taking a risk or assessing the feasibility of investment in private sector projects.

This risk-free lending to the government provides an opportunity for the banks to invest the depositors’ money in government securities. The credit to the government as a percentage of outstanding deposits of commercial banks was more than 98 percent at the end of December 2025, while the share of the government credit in the expansion of the money supply (M2) is greater than 85 percent. The banks listed on the stock market show a massive growth in their earnings. Nearly half of the gross interest income of the scheduled banks was attributable to Pakistan Investment Bonds (PIBs).

The inordinate growth in government borrowing from commercial banks to finance the fiscal deficit is a drastic indicator that hampers the private sector in multiple ways. The huge lending by commercial banks to the government can adversely affect the volume of domestic credit to the private sector, which is required for core economic activities and the enhancement of employment and business opportunities.

On the other hand, the continuous heavy borrowing by the government creates a burden of repayments, which is ultimately transferred to the private sector. To consider lending to the government as a haven is just an illusion. A government with a high debt-to-GDP ratio and continuous growth in borrowing to repay previous loans is strange for the lenders.

It becomes stranger if GDP growth is lower than the required growth, and enhancement in the tax base is not possible. The debt liability of the government is ultimately repaid by the private sector through additional taxes or the withdrawal of subsidies or public services. In this situation, lending to the government can be riskier than advances to private businesses, where earning capacity is visible, and assets can be pledged by the lenders. Unfortunately, the prudential regulations cannot limit the public borrowing from commercial banks.

However, the policymakers in Pakistan should consider the important point that borrowing from commercial banks to repay the public sector debt is a dangerous way of financing. These debts can further damage the economy and businesses. It is an established premise that banks, through their credit policies, can play an important role in alleviating poverty and creating employment opportunities through the creation and enhancement of business opportunities. The inter-connectedness of the banking sector, public sector debt, and financing for private sector business activities is an important concern in the present scenario.

The growth in taxes is a natural outcome of the growing debt service. The debt serving as a percentage of gross national income of Pakistan was 1.9 percent in 2009; now it is greater than 4.8 percent, while it was 15 percent of the export proceeds in 2009, and now it is greater than 43 percent of the export proceeds. The collection of taxes after paying subsidies and adjustments for all refunds, drawbacks, exemptions, and subsidies was around PKR 650 billion in 2009; now it is more than PKR 4.4 trillion. Despite this expansion in taxes, the ‘Tax to GDP ratio’ is strangely lower than the world average. Pakistan is included in the world’s top-most high tax rate countries. These higher rates of direct and indirect taxes, along with the lower tax-to-GDP ratio, reveal the extreme uneven distribution of the tax burden.

The domestic credit to the private sector as a percentage of GDP is extremely low in Pakistan compared to other countries. The magnitude of domestic credit to the private sector as a percentage of GDP is 12 percent in Pakistan. It is 50 percent in India and 136 percent on average in middle-income countries. The world average is 146 percent. Notably, since the last decade, there has been a worldwide increasing trend in domestic credit; however, it has been decreasing in Pakistan year by year. The domestic credit as a percentage of GDP in South Asian countries is lower than in the rest of the world, and the ratio is the lowest in Pakistan (excluding Afghanistan).

The role of credit to the private sector by commercial banks becomes more important in the case of Pakistan because the size of the non-banking financial sector in domestic lending is almost negligible. More than 99 percent of the credit to the private sector in Pakistan belongs to commercial banks. Financial inclusion is one of the drivers of the size of domestic credit. The number of borrowers is an indicator of financial inclusion. The number of borrowers per thousand people is 26 in Pakistan. This number is 84 in Bangladesh and 82 in lower-middle-income countries. There are multiple reasons for the lower number of borrowers in Pakistan. The qualitative controls, including guarantees and collateral, and lack of financial literacy, are some of the obvious reasons.

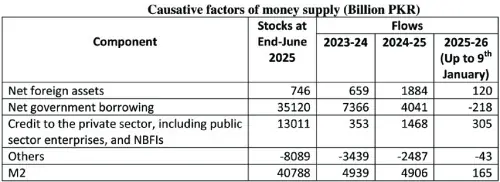

The domestic credit to the private sector has dropped to 12 percent from 20 percent in 2009, though a slight growth in domestic credit was observed after the declining trend in interest rates during the last fiscal year. Domestic credit to the private sector was recorded at PKR 353 billion in 2023-24, PKR 1468 billion in 2024-25, and PKR 578 billion in the first half of 2025-26.

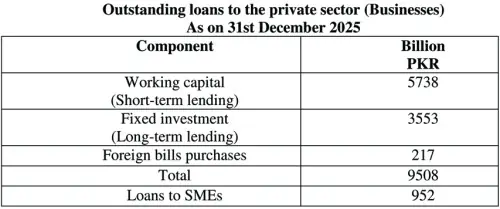

In the recent monetary policy, the State Bank has decided to reduce the average cash reserve requirement for banks from 6 percent to 5 percent, which may enhance the credit to the private sector. However, how much credit to the private sector is used to finance the fixed investment is an important concern. More than 60 percent of this credit belongs to the working capital.

Less than 40 percent of domestic credit is utilized for fixed investment. The investment in fixed assets can lead to the creation of new businesses, expansion of existing businesses, and industrialization, which are the ultimate sources of growth in industrial output and employment opportunities. The share of small and medium enterprises (SMEs) in domestic credit is only one percent, which indicates the priority of the banking sector.

The most important dimension of the lower credit to the private sector in Pakistan is that the interest rates in Pakistan are much higher than the other countries in the region. It is one of the highest interest rates in the world. This difference in the interest rates affects the competitiveness of Pakistani businesses and creates an uncompetitive environment. Neither Pakistani investors can compete with foreign investors, nor can they sell their products at competitive prices. The lack of industrialization and participation in investment activities, and the slower growth of exports, are the consequences of this uncompetitive environment.

The estimated growth in GDP for the year 2025-26 is 3.6 percent, which is lower than the required rate of growth, while the expected rate of inflation is 7 percent. After implementation of the recent monetary policy, the real rate of interest will be 4.5 percent, which is 1 percent higher than the real GDP growth. A usual stance by the policymakers to justify the higher interest rate is the higher rate of inflation in Pakistan. This justification does not provide a solution. To explain the reasons for an uncompetitive environment by policymakers cannot improve the economy. Addressing the reasons and finding their solution is the basic responsibility of policymakers.

To create a balance between an attractive rate of return to the depositors and a competitive rate of interest on lending, the regulatory authorities will have to restrict the interest rate spread. Based on the last 4 decades, it was noted that the interest rate spread is much higher in Pakistan than in other countries. The higher spread of interest rates indicates lower payments to depositors and higher charges from borrowers. It is considered a tool of exploitation. Empirical pieces of evidence show that lower-income households and vulnerable employees are the actual victims of higher interest rates and interest rate spreads.

Copyright Business Recorder, 2026

The author is a professor at Iqra University Karachi.

Comments