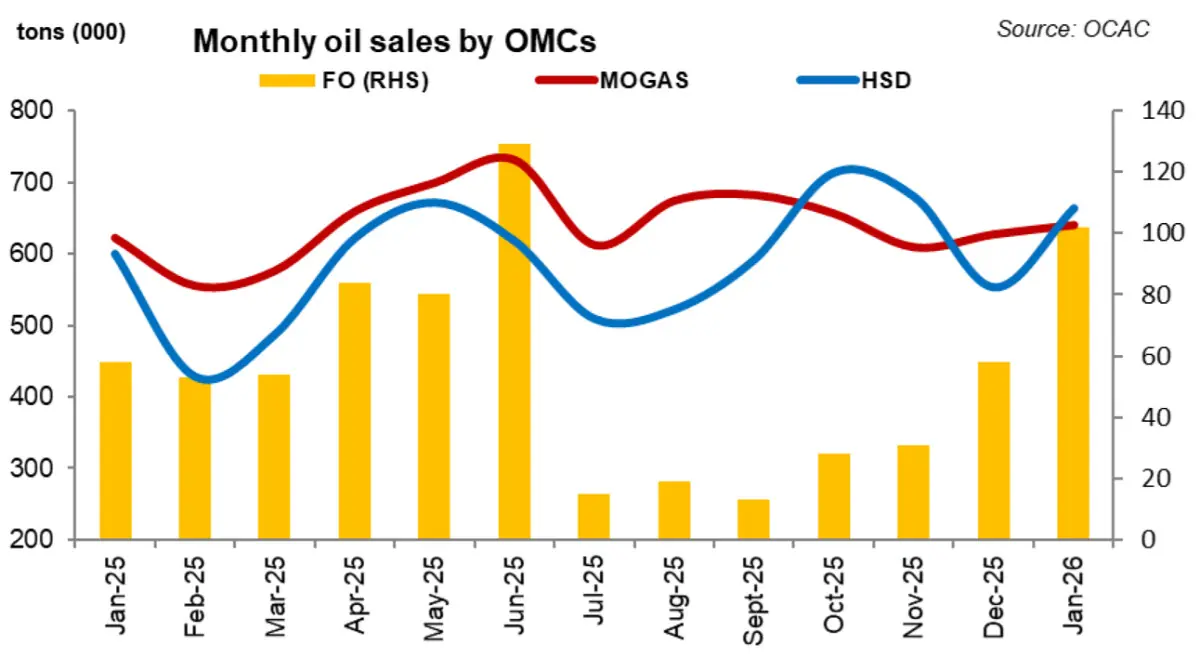

The OMC sector recorded a strong rebound in Jan-26, with total petroleum product sales rising by 10 percent year-on-year and 12 percent month-on-month. The monthly recovery was broad-based across major transport fuels and largely reflects a combination of lower retail prices, normalization of demand after disruptions in December, and gradual improvement in underlying economic activity.

In Dec-25, sales had been suppressed by a nationwide strike that disrupted distribution for roughly ten days, creating a low base that amplified the month-on-month rebound in January.

Product-wise, high-speed diesel remained the main driver of growth. HSD sales increased by 11 percent year-on-year and 20 percent month-on-month, supported by lower pump prices, improved farm activity, and better enforcement against smuggling.

Motor spirit sales showed a more modest but still positive increase of 3 percent year-on-year and 2 percent month-on-month, consistent with gradual recovery in urban mobility and automobile usage. Excluding furnace oil, total sales stood reflected a 7 percent year-on-year and 9 percent month-on-month increase, underscoring that the core demand recovery is concentrated in transport fuels rather than residual fuel use.

Furnace oil sales, while structurally declining over the medium term, showed a temporary spike in Jan-26, rising by 76 percent month-on-month with the highest level in seven months. This increase was driven by seasonal factors, including lower hydel generation during winter months and higher reliance on thermal power generation, as well as higher refinery throughput.

Despite this monthly jump, furnace oil remains on a clear downward trajectory on a cumulative basis due to policy measures, including a significantly higher petroleum levy introduced in the FY26 budget, which continues to discourage its use.

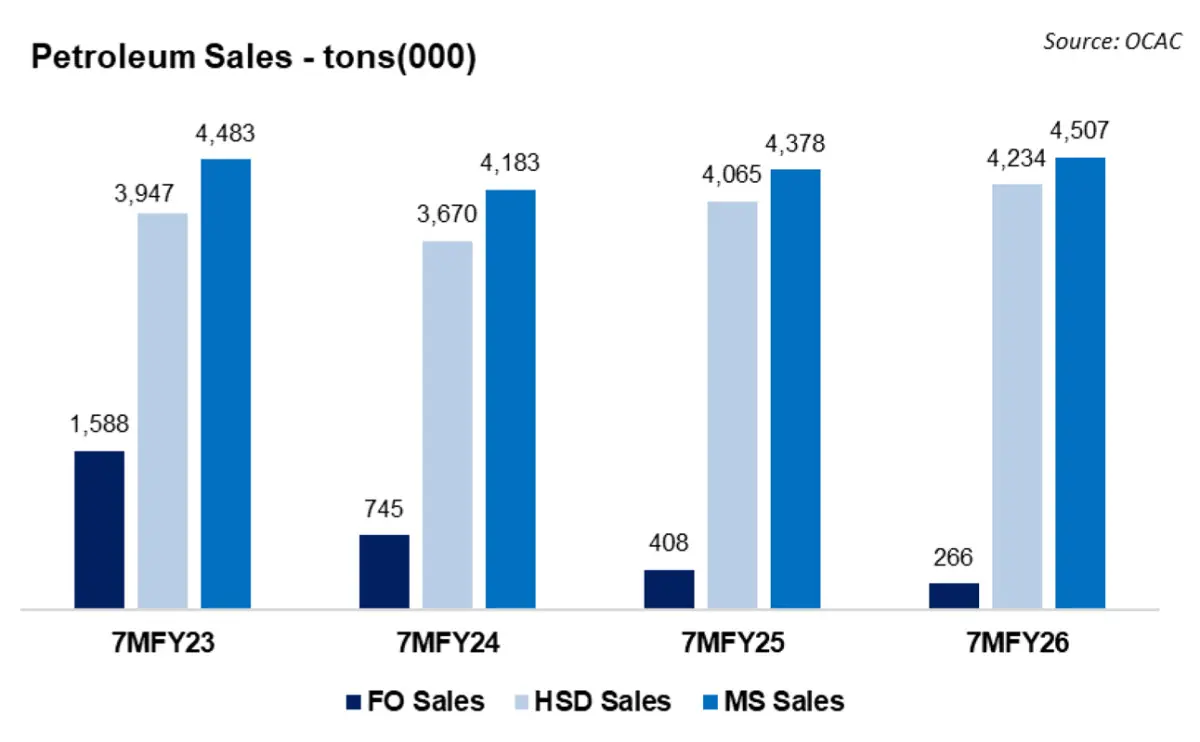

On a cumulative basis, oil sales in 7MFY26 represented a 3 percent increase compared to the same period last year. This headline growth masks an important shift in composition. Both motor spirit and high-speed diesel volumes posted growth of 3–4 percent year-on-year, while furnace oil volumes declined sharply by 36 percent year-on-year. Excluding furnace oil, cumulative sales for 7MFY26 increased by about 5 percent year-on-year, highlighting a healthier underlying demand trend tied to transport, agriculture, and logistics rather than power generation.

The broader macro backdrop has been supportive. Easing inflation, relatively stable fuel prices compared to last year, improved control over illicit fuel inflows, and a gradual pickup in large-scale manufacturing activity have all contributed to firmer demand. Lower month-on-month fuel prices in Jan-26—around a 4 percent reduction in motor spirit and a 6 percent reduction in diesel—provided a direct boost to consumption, particularly for diesel-intensive segments such as freight transport and agriculture.

The outlook for OMC sales over the remainder of FY26 appears cautiously positive. Industry-wide volumes are expected to continue growing in the mid-single-digit range, with most forecasts pointing to full-year growth of around 7–10 percent, driven primarily by diesel and petrol demand. Key upside risks include further improvement in economic activity, continued enforcement against smuggling, and stable or lower international oil prices.

However, structural headwinds remain, particularly for furnace oil, which is likely to stay under pressure due to policy disincentives and the ongoing shift in the power generation mix. Overall, Jan-26 reinforces the view that Pakistan’s oil demand is stabilizing and gradually recovering, with growth increasingly concentrated in transport fuels rather than legacy segments.

Comments