SBP holds policy rate at 10.5% in first 2026 MPC meeting

- Decision against market expectations of a cut in key interest rate

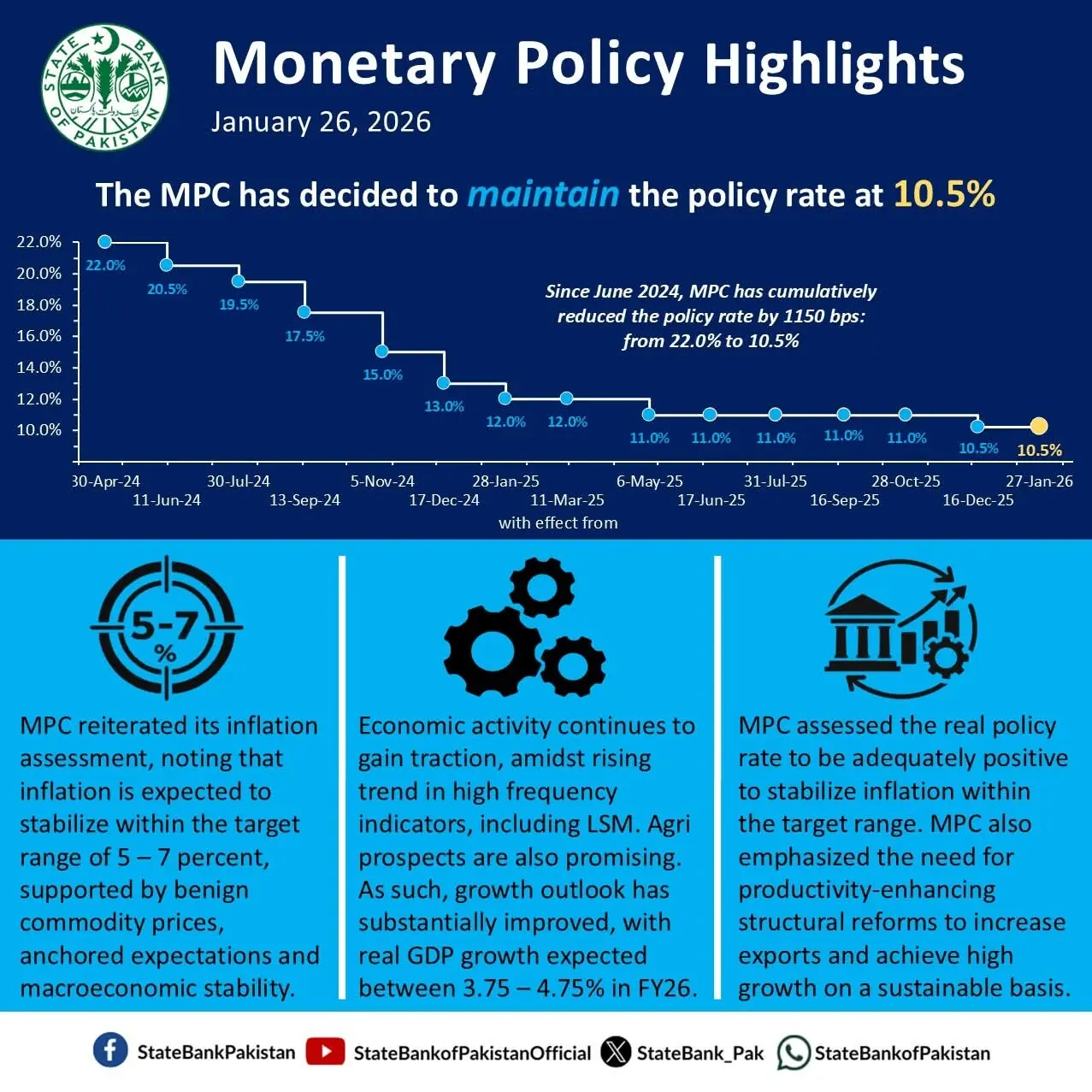

The State Bank of Pakistan (SBP) decided on Monday to keep its benchmark policy rate unchanged at 10.5% in its first Monetary Policy Committee (MPC) meeting of 2026.

SBP Governor Jameel Ahmad announced the decision in a press conference.

Inflation in Pakistan could be above 7% in some months of the current fiscal year’s second half, he said.

The country’s gross domestic product (GDP) would grow by 3.75% to 4.75% this year, Ahmad envisaged.

What MPC says

The central bank later issued a detailed MPC statement on its decision to maintain the status quo. It said:

The committee observed that headline inflation of 5.6% y/y in December 2025 was in line with its expectation. However, core inflation has steadied around a relatively higher level of 7.4% in recent months. Meanwhile, as reflected by the recent high frequency indicators (HFIs), including large-scale manufacturing (LSM), economic activity continues to gain momentum faster than anticipated, mainly led by domestic-oriented sectors.

The committee also noted that the trade deficit has widened in the wake of a substantial increase in imports, particularly import volumes, and a decline in exports. Nonetheless, based on the resilient workers’ remittances and benign global commodity prices, the current account deficit remained relatively contained.

In this backdrop, the MPC noted that the outlooks for inflation and the current account are broadly unchanged from its previous assessment, while the outlook for economic growth has improved significantly. Based on this, the committee deemed it prudent to hold the policy rate unchanged at the current level to ensure price stability and support sustainable economic growth.

On balance, the committee projected inflation to stabilise within the target range of 5-7% in FY26 and FY27, after temporarily exceeding the upper bound for a few months during this calendar year.

“This outlook is subject to risks emanating from volatility in global commodity and domestic wheat prices, unanticipated adjustments in administrative energy prices, and a sharper than assumed pickup in domestic demand.”

At its previous meeting on December 15, 2025, the MPC had reduced the policy rate by 50 basis points (bps) to 10.5%.

Market experts had widely expected the central bank to further reduce the policy rate in today’s meeting on account of easing inflation, external stability and falling bond yields.

Arif Habib Limited (AHL) had anticipated that the SBP was likely to deliver a 75bps cut in the MPC, potentially taking the policy rate to 9.75%, “signalling a long-awaited return to single-digit territory”. However, the central bank decided to unchange the policy rate.

Similarly, Topline Securities, another brokerage house, had also expected a rate cut, citing its recent survey, which showed that 80% of the participants were expecting a rate cut.

The brokerage house had attributed the shift in market perception to lower-than-expected inflation readings in the last two months, better than expected remittance flows, supporting external accounts, and largely stable PKR/USD parity.

Similarly, a Reuters poll had found that the central bank was expected to cut its key policy rate by 50bps, as easing inflation, improving foreign exchange buffers, and a stabilising rupee bolster the case for further monetary easing despite lingering risks.

Of the 10 analysts surveyed, seven had expected the SBP to cut rates by 50bps, two saw a deeper 75bps reduction, while one expected the central bank to hold rates unchanged.

Apart from analysts, business leaders also urged the government to bring the policy rate down to single digits, citing easing inflation.

In a statement, Saqib Fayyaz Magoon, Chairman of the Businessmen Panel Progressive (BMPP) and Senior Vice President of the Federation of Pakistan Chambers of Commerce & Industry (FPCCI), had warned that persistently high borrowing and energy costs had been inflicting serious harm on industrial output and export competitiveness.

He said the government should capitalise on the improving inflation outlook to offer immediate relief to the business community by lowering the cost of financing.

Saqib stressed that the policy rate should be brought down to single digits without delay and called for a cut of at least 100bps, which he described as a long-standing demand of the business community.

The committee noted the following key developments since its last meeting:

- First, real GDP growth was provisionally reported at 3.7% y/y for Q1-FY26, mainly led by the industry and agriculture sectors.

- Second, both consumer and business confidence improved, whereas inflation expectations of these stakeholders eased.

- Third, SBP’s FX reserves surpassed the end-December target, reaching $16.1 billion as of January 16, mainly led by SBP’s ongoing interbank FX purchases.

- Fourth, FBR revenue growth decelerated to 7.3% in December, falling short of the target.

- Lastly, the IMF has slightly upgraded its global growth forecast for 2026, while also highlighting the risks from elevated global tariff uncertainty and volatile commodity prices amidst geopolitical developments.

In view of these developments, the MPC assessed the real policy rate to be adequately positive to stabilise inflation within the target range of 5–7% over the medium term.

The committee also emphasised the need for coordinated and prudent monetary and fiscal policy mix – as well as productivity-enhancing structural reforms – to increase exports and achieve high growth on a sustainable basis.

Comments

Comments are closed for this article.