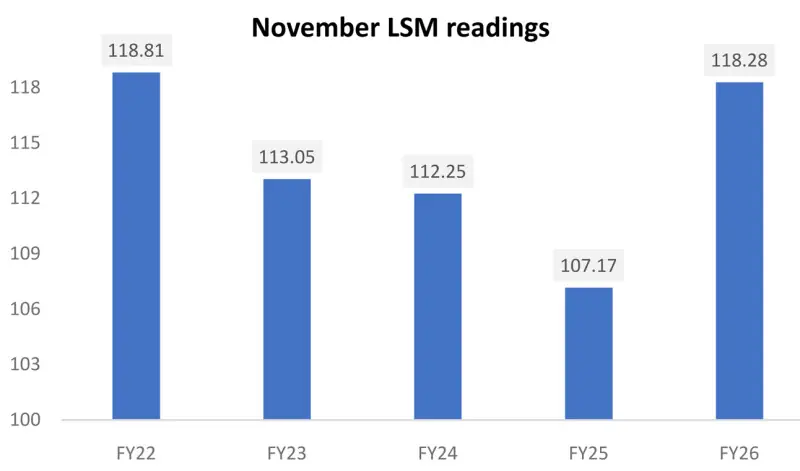

After years of stop-start recoveries, Large-Scale Manufacturing is now exhibiting momentum that is difficult to dismiss as episodic. November 2025 marked a decisive break from past patterns.

Year-on-year growth of 10.37 percent was the strongest since June 2022, while the November index reading matched the highs last seen in November FY22.

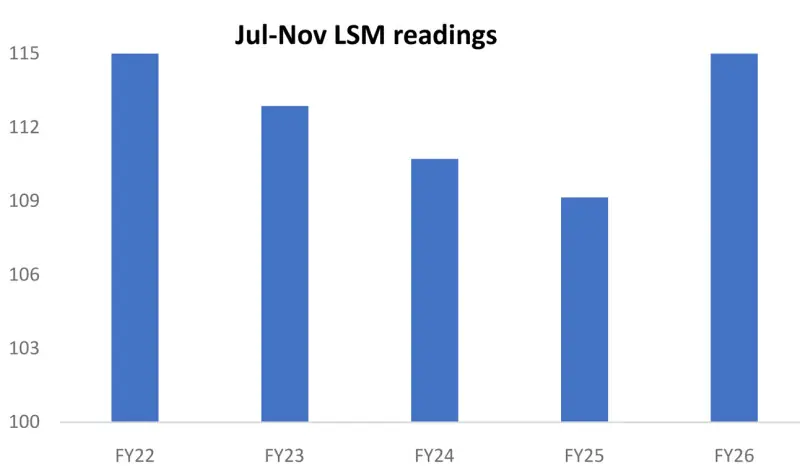

On a cumulative basis, LSM growth for 5MFY26 stands at 6.01 percent year-on-year, with the index reading for the July to November period the highest ever recorded for this window.

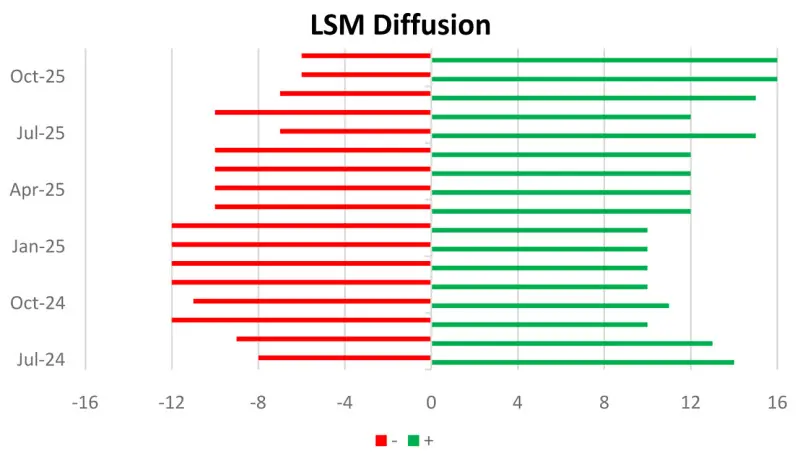

More telling than the headline numbers is the breadth of the recovery. On a cumulative 5MFY26 basis, 16 industries are in positive territory, with only six contracting. For November alone, just four industries remained in the red, the lowest count of negative sectors since February 2022. This confirms that LSM growth is no longer being propped up by one or two outperformers, a recurring feature of earlier recoveries.

Sectoral dynamics underline this shift. Automobiles continue to anchor growth, but petroleum has emerged as the standout performer.

On a cumulative basis, petroleum contributed second most to overall LSM growth after automobiles, while in November alone it made the single largest contribution. Year-on-year growth of 44 percent in November reflects record-breaking production. Both petrol and high-speed diesel reached their highest-ever monthly output, pushing the petroleum index to its strongest level since May 2018.

The food sector is also gaining traction. The sugar season has commenced on a firmer footing compared to last year, providing an early boost to food LSM. With sugar carrying the second-highest weight in the food basket, sustained production between November and March could meaningfully lift cumulative food sector growth in the months ahead.

An unexpected boost in November came from the beverage sector, which despite its relatively low weight made a significant contribution to overall LSM growth. The beverage index for November 2025 was the highest ever recorded for the month, and by a wide margin, driven primarily by strong output of soft drinks and mineral water.

Textiles remain under pressure, but this weakness is increasingly being offset by steady gains in readymade garment exports.

While month-on-month fluctuations persist, year-on-year momentum remains intact, aided by a favorable base. Pharmaceuticals, by contrast, continue to underperform overall, though November did offer a bright spot.

Tablet production rebounded to a 40-month high, suggesting early signs of stabilization within a subdued sector.

Transport-related manufacturing continues to reinforce the expansion. Motorcycle and bicycle sales reached 4-year and 6-year monthly highs, respectively, in November, aligning with broader strength across the automobile value chain. These trends are feeding directly into LSM readings and strengthening the case for durability.

Macro conditions are now turning supportive rather than merely less restrictive. The interest rate cycle has begun to ease, energy prices are materially lower than both one year and two years ago, and incentives on incremental electricity consumption remain in place.

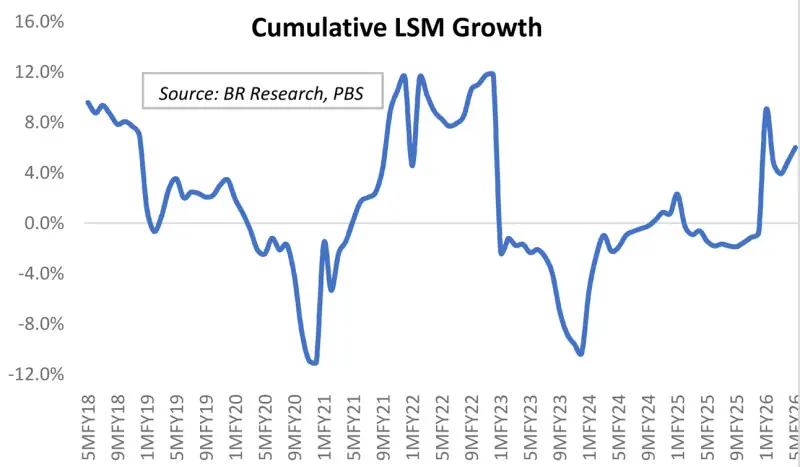

Together, these factors are translating into improved capacity utilization and sustained output gains. LSM growth is increasingly resembling a trend rather than a short-lived rebound.

That said, perspective remains necessary. FY22 continues to serve as the benchmark, and it remains out of reach for FY26. To match those highs, LSM growth would need to average close to 15 percent over the remaining seven months, an outcome that appears unlikely.

Even so, the current trajectory suggests that LSM has decisively turned a corner. The damage inflicted over the past few years has been deep, but the recovery is now broader, more balanced, and materially more credible than at any point since mid-2022.

Comments