The government’s latest motion for determination on the rebasing of electricity tariffs for CY26 appears, at first glance, to mark a reversal in a long-running trend.

Protected domestic consumers are now envisaged at 17.23 million, down sharply from 20.48 million in the July 2025 rebasing exercise.

After nearly four years in which the protected category had effectively doubled, this headline reduction seems to suggest a structural correction is finally underway.

That impression, however, does not survive a closer reading of the consumption data.

In proportional terms, protected consumers still account for 57 percent of total domestic consumers in CY26, only modestly lower than the 61 percent recorded in 2025.

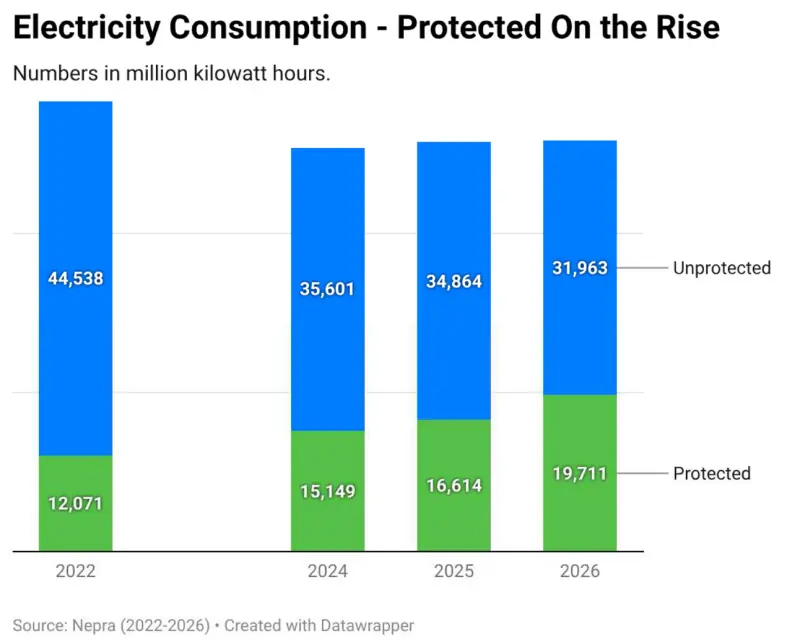

More strikingly, the share of protected consumers in total domestic electricity consumption is projected to rise to 38 percent. This is up from roughly 32 percent last year, representing a near 19 percent year-on-year increase.

In absolute terms, protected consumption is envisaged to rise by over 3 billion units, crossing 19.7 billion kilowatt hours in CY26. This would be the highest annual protected consumption ever projected in Pakistan’s power sector planning.

This creates a peculiar outcome: three million fewer protected consumers are expected to consume three billion additional units of electricity compared to last year. In other words, while the protected headcount is falling, protected consumption intensity is rising sharply.

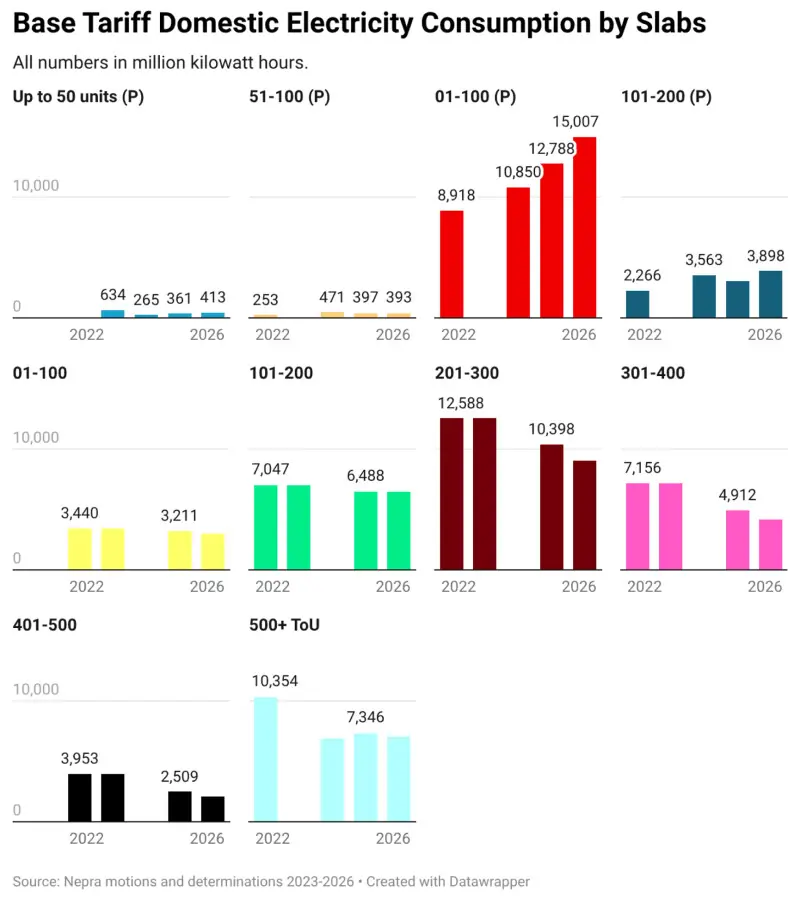

The charts on domestic slab-wise consumption underscore this shift, with visible growth in protected slabs up to 100 units, even as higher unprotected slabs show compression.

The anomaly does not stop there. Total electricity consumers across categories are envisaged to fall by a staggering 3.8 million compared to the previous exercise. Of this, 3.2 million is attributed to domestic consumers, followed by a decline of roughly half a million commercial connections. Yet, the number of unprotected domestic consumers remains broadly unchanged from last year. What does change materially is their consumption profile: unprotected domestic consumption is projected to fall by around 8 percent, or nearly 3 billion units, year-on-year. Even within unprotected slabs up to 400 units, consumption eases, though the contraction is far less pronounced than in protected categories.

On the commercial side, the numbers are even more counterintuitive. A loss of nearly 0.5 million consumers, equivalent to about 15 percent of the base, is not accompanied by any meaningful decline in consumption. Commercial electricity use is projected to remain flat, raising obvious questions about the credibility of demand assumptions or the extent of informal load shifting across categories.

The most plausible explanation cutting across these inconsistencies is the rapid and largely unmetered rise of rooftop solar adoption. Solarisation in Pakistan has been overwhelmingly rural and peri-urban in nature, where consumption slabs are lower and single-phase connections dominate. Since net metering regulations effectively exclude single-phase consumers, the bulk of solar generation continues to sit behind the meter. As a result, grid-recorded consumption falls even when actual electricity usage does not.

This dynamic has been increasingly visible in system-wide load curves. Daytime demand erosion has accelerated, producing a progressively deeper duck curve month after month. Consumers that were previously unprotected are either slipping into protected status or remaining in the same category while migrating to lower consumption slabs. The charts reflect this redistribution clearly: growth in protected consumption coincides with a compression of unprotected demand, despite minimal change in unprotected consumer numbers.

The policy implications are significant. Cross-subsidies, already stretched, are implicitly being asked to do more with less. As more units migrate into protected slabs, the burden of financing these subsidies concentrates further on a shrinking pool of grid-dependent, higher-consumption users. This is occurring even as total domestic consumption itself remains under pressure.

The government, under IMF scrutiny, is reportedly considering a rationalisation of electricity subsidies by linking tariffs to income levels rather than consumption thresholds. Conceptually, this represents a fairer and more targeted approach, and one that better reflects ground realities in a solarising economy. It would also help keep the undeserving out of the subsidy net, a long-standing weakness of Pakistan’s slab-based framework.

However, the pace of change in consumption patterns suggests that incremental policy responses may no longer suffice. The power sector is undergoing a structural demand shift driven by behind-the-meter generation, not cyclical price effects. Tariff rebasing exercises that continue to rely on legacy assumptions about consumption behaviour risk becoming increasingly detached from reality.

The data for CY26 should therefore be read less as an anomaly and more as a warning. Protected consumers may be fewer, but they are consuming more than ever. Unless tariff design, subsidy architecture, and solar integration policy move in tandem—and quickly—the distortions now visible in the charts will only deepen, further complicating the already fragile economics of Pakistan’s power sector.

Comments

Comments are closed for this article.