Pakistan’s oil marketing companies recorded a mixed performance in December 2025, with headline volumes improving year-on-year but weakening on a month-on-month basis.

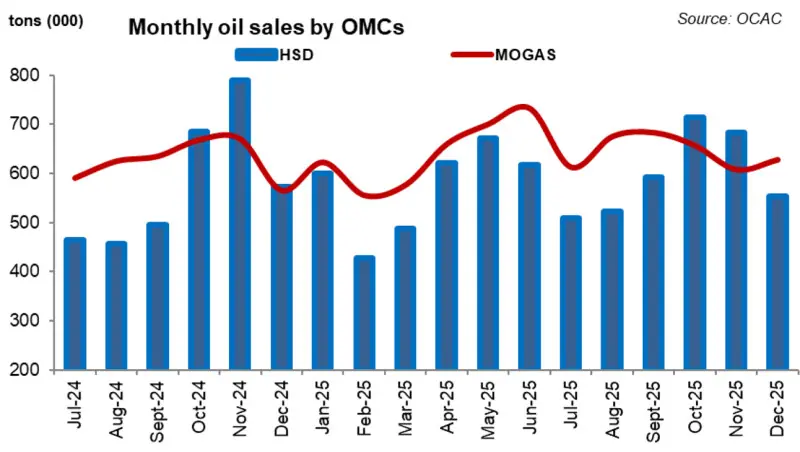

Total industry sales stood at 1.35 million tons, marking a 6 percent increase year-on-year but a 5 percent decline compared to November, reflecting short-term disruptions rather than a reversal in underlying demand trends.

The year-on-year improvement was driven by a combination of easing inflation, modest economic recovery, and better control over fuel smuggling.

In contrast, the month-on-month decline was largely attributable to a nationwide transporters’ strike that began on December 8 and lasted for nearly ten days, temporarily curbing fuel offtake across major consumption centers.

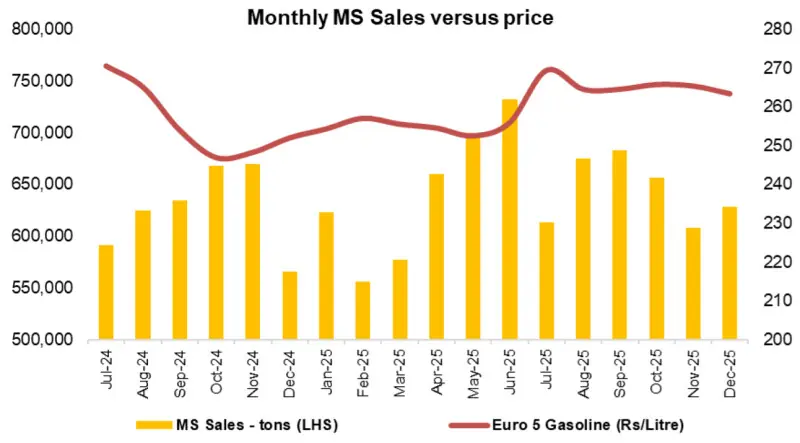

Product-wise, the divergence in demand patterns remained evident. Motor Spirit (MS) continued to outperform, with sales rising 11 percent year-on-year and 3 percent month-on-month, supported by improving industrial activity and sustained growth in automobile sales.

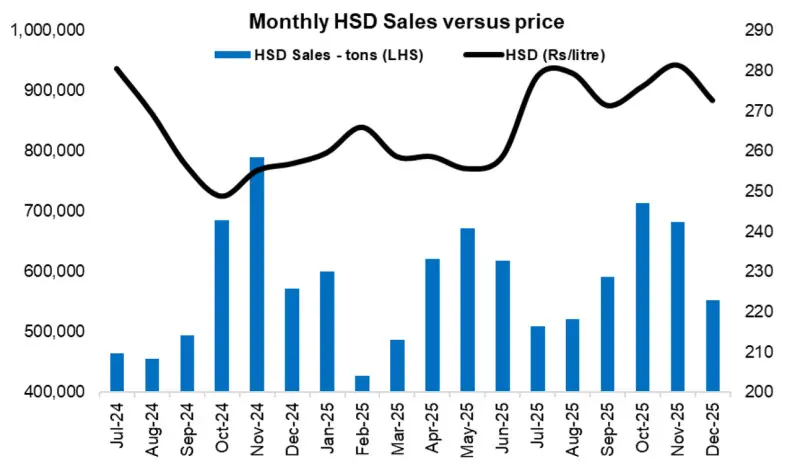

High-Speed Diesel (HSD), however, declined 4 percent year-on-year and 19 percent month-on-month, reflecting seasonal weakness tied to the end of the farming cycle as well as disruptions in heavy transport activity.

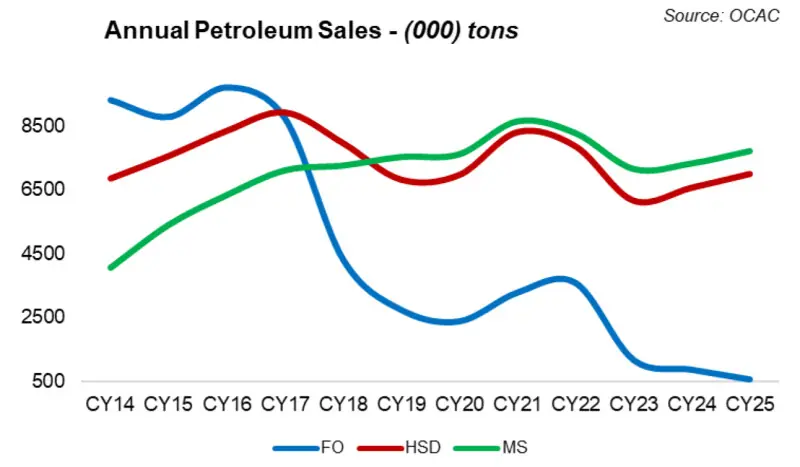

Furnace oil (FO) sales surged sharply, up 40 percent year-on-year and 130 percent month-on-month, largely due to higher FO-based power generation and elevated refinery throughput, making December the strongest month for FO since the imposition of the petroleum levy in July.

On a cumulative basis, 1HFY26 industry sales reached 8.16 million tons, showing a 2 percent year-on-year increase, while ex-FO volumes grew by 4 percent, indicating that core fuel demand is recovering gradually despite lingering macro and logistical constraints.

Overall, the December data underscores that Pakistan’s oil demand recovery remains intact but uneven, with MS acting as the primary growth engine while HSD continues to lag due to structural and seasonal factors. With Petroleum Development Levy collections already reaching around half of the full-year FY26 target in 1HFY26, volume growth rather than pricing will be critical for sustaining sector momentum in the second half of the fiscal year.

Comments

Comments are closed for this article.