BR RESEARCH: Hub Power Company Limited’s performance and outlook

HUBC is Pakistan’s largest Independent Power Producer, operating 3,581 MW across thermal, hydel, and coal projects. Its portfolio includes the Hub and Narowal residual-fuel-oil plants, a majority stake in Laraib’s hydropower facility, and a joint venture with China Power International Holdings in the 1,320 MW CPHGC coal plant.

The company has expanded into Thar coal with majority stakes in Thar Energy Limited and ThalNova Power Thar, both 330 MW mine-mouth lignite plants. To support growth, HUBC operates through two subsidiaries—HPSL for operations and maintenance, and HPHL for new investments—and also holds an 8 percent stake in Sindh Engro Coal Mining Company, which supplies coal to its Thar projects.

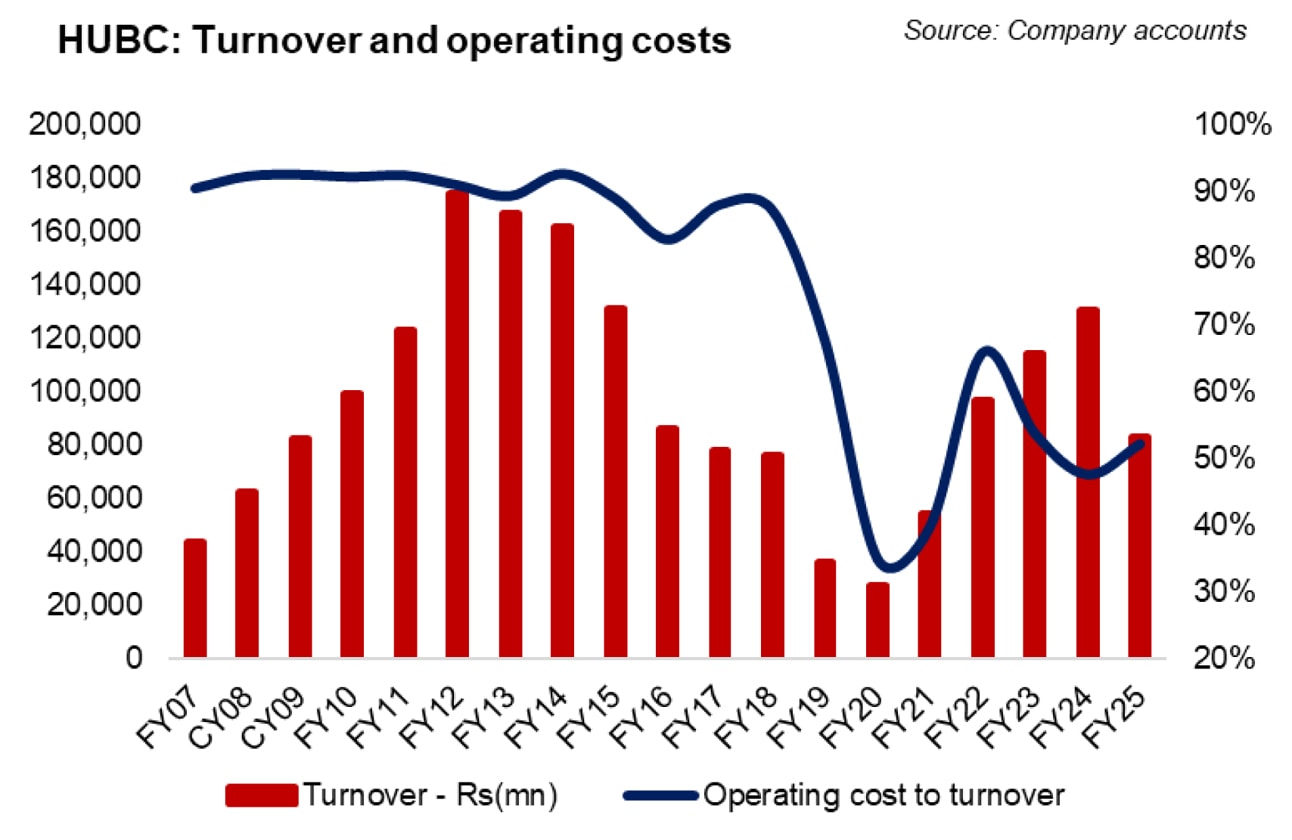

Past Performance FY15 was a transformative year for HUBC, with strong shareholder returns and a successful business turnaround. Despite a slight drop in load factors due to boiler maintenance, consolidated earnings rose by 48 percent year-on-year.

In FY16, earnings grew by 7.5 percent, but revenues fell 34 percent due to lower furnace oil prices, reduced generation bonuses, and lower electricity demand.

FY17 saw a significant drop in earnings, driven by higher maintenance costs at the Hub and Narowal plants, unfavorable exchange rates, and losses from early-stage TEL and CPHGC projects. Increased administrative expenses also contributed to a 9.2 percent decline in profits.

In FY18, earnings rose by 3 percent, despite lower revenues. This modest growth was due to reduced maintenance costs, although profits from Laraib were lower, and financing costs increased. Load factors at the Hub and Narowal plants dropped due to reduced electricity demand and maintenance work.

FY19 was challenging, with furnace oil-based generation falling 60 percent, slashing HUBC’s base plant load factor to 7.87 percent. Revenues dropped by 42 percent, but lower operating costs helped the company maintain flat earnings growth of 2 percent, despite higher finance costs and capital expenditures.

FY20 was impacted by the COVID-19 pandemic and government scrutiny of IPP returns. However, HUBC’s earnings more than doubled, driven by its 1,320 MW coal-fired plant and currency depreciation. Growth was tempered by higher finance costs, increased taxes, and a one-off equity transfer to the Government of Balochistan.

In FY21, HUBC’s revenue grew 13 percent, supported by a 40 percent increase in power dispatches and improved load factors across its plants. Earnings rose by 34 percent due to profits from CPHGC and lower finance costs.

FY22 saw a 15 percent drop in earnings, mainly due to lower profits from associates and higher finance costs. However, revenues increased by 78 percent, driven by higher utilization of the base and Narowal plants. Despite this, gross profits were flat, and no dividends were declared due to high fuel and commodity prices.

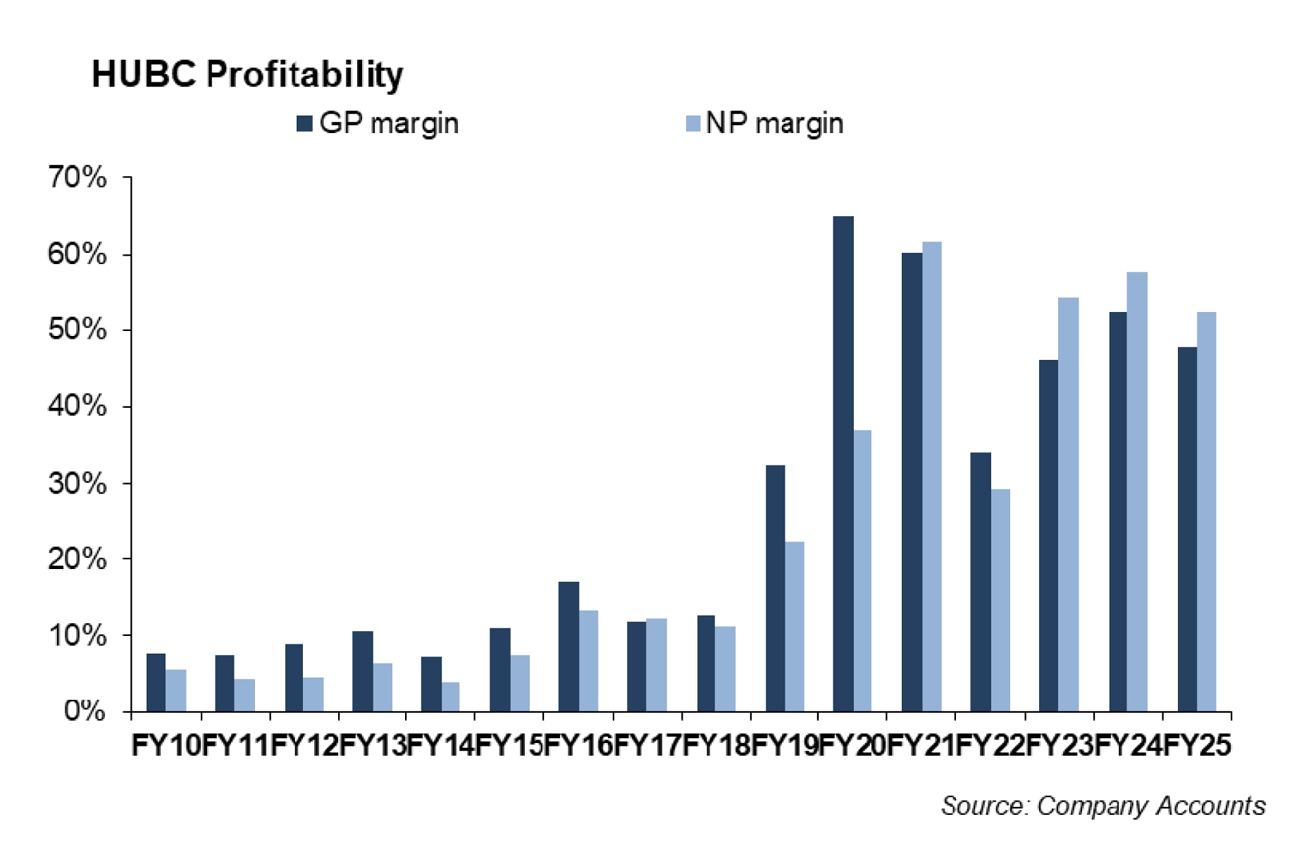

The Hub Power Company Limited (HUBC) reported its highest-ever profit for FY23, driven by its diversification strategy and a greater share of profits from associates and joint ventures. This growth was fueled by its coal investments, particularly from the China Power Hub Generation Company (CPEC), which has been contributing since FY20, as well as the addition of the ThalNova Power Plant in February 2023 and TEL later in FY23.

Consolidated revenue increased by 18 percent, primarily due to higher furnace oil prices, despite a 9 percent decline in electricity dispatches. HUBC's bottom line surged by 110 percent year-on-year, thanks to controlled expenses, higher other income, and a significant rise in profits from associates. However, rising finance costs, which increased by 144 percent due to higher interest rates and TEL’s finance costs, partially offset the profitability gains.

In FY24, Hub Power Company Limited (HUBC) delivered a robust financial performance, reporting consolidated earnings of Rs75 billion, reflecting a 22 percent year-on-year increase. This growth was driven by higher dispatches from Thar Energy Limited (TEL), the devaluation of the PKR against the USD, and improved operational efficiencies. Overall revenue growth stood at 14 percent year-on-year.

While TEL and ThalNova Power Thar (TNPTL) showed strong performance with increased generation, China Power Hub Generation Company (CPHGC) saw a decline.

HUBC's gross margins improved, benefiting from currency devaluation and contributions from new power plants. Despite a 38 percent rise in finance costs, net margins increased, supported by a 44 percent rise in profits from associates due to the commencement of operations at TEL and TNPTL, along with the currency impact.

The company announced a total dividend of Rs20 per share for FY24, down from Rs30 in FY23, due to increased capital expenditure and new investments.

HUBC’s performance in FY25 reflected a year of transition, shaped primarily by the expiry of its base plant Power Purchase Agreement, softer load factors, and an ongoing strategic shift toward diversification. The company decline of 34 percent year-on-year. This reduction was largely the result of the termination of the Hub base plant agreement, which removed a major source of stable capacity revenues.

Revenues also declined 36 percent year-on-year as the company absorbed the impact of both the base plant’s termination and tariff revisions at Narowal Energy Limited.

Despite these headwinds, HUBC maintained strong operational resilience. Availability across the portfolio remained solid, and the Thar-based plants—Thar Energy Limited and ThalNova Power Thar Limited—delivered approximately $290 million in annual foreign exchange savings. While profits from associates and joint ventures softened due to the appreciation of the rupee and an unusually high base year, the company saw a marked improvement in payment cycles.

HUBC in FY26 and beyond

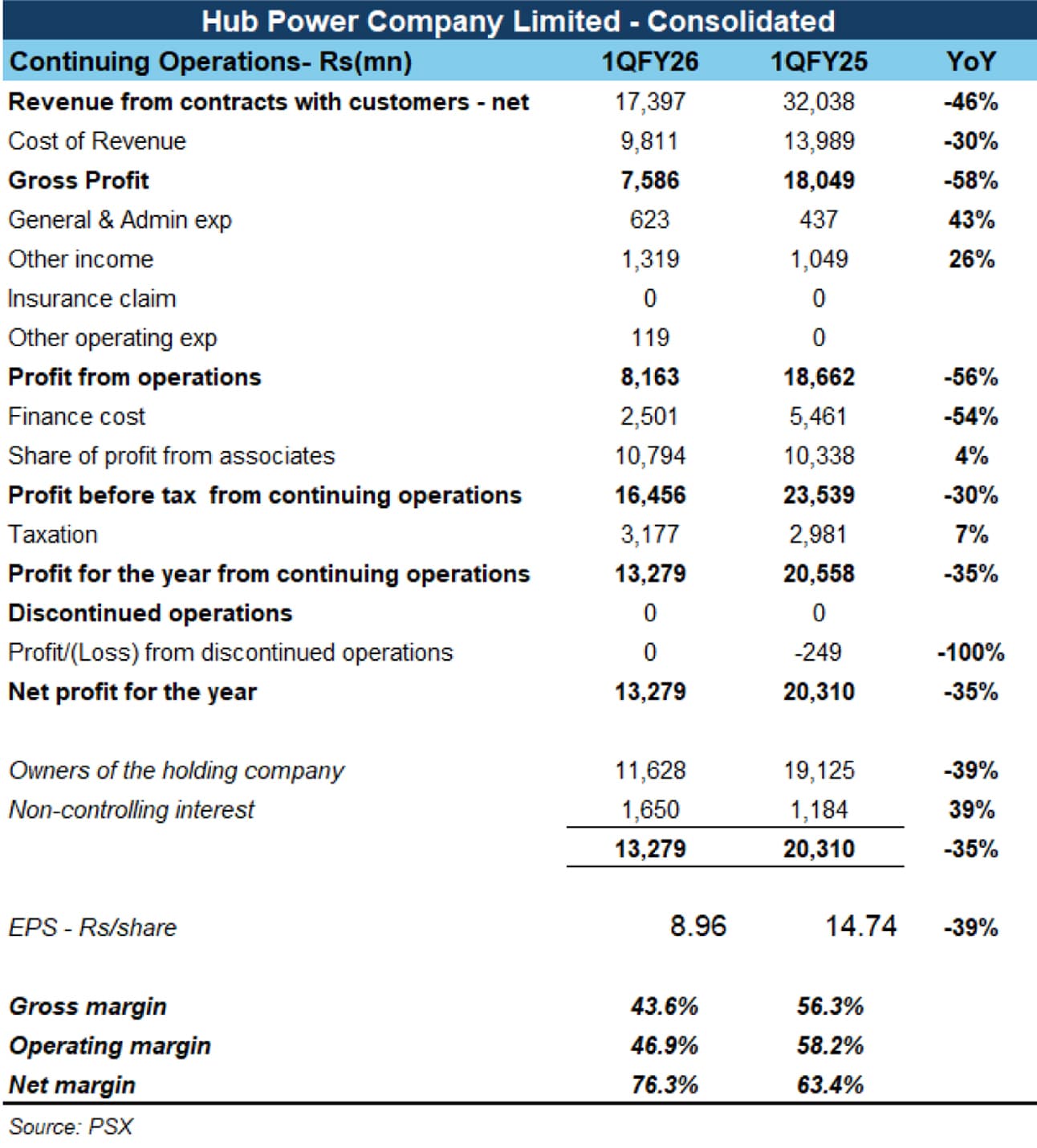

The last couple of years marked a turning point in HUBC’s strategic direction as the company accelerated its expansion beyond power generation into electric vehicles, mineral exploration, and upstream energy. Its partnership with BYD continued to gain momentum. Entering FY26, HUBC posted a 39 percent year-on-year decline in consolidated earnings for 1QFY26, driven largely by the absence of base plant revenues and the revised tariff structure for Narowal Energy Limited.

Despite weaker profitability, the company announced a cash dividend of Rs 5 per share, reflecting strong liquidity supported by sustained dividend inflows from associates.

Net revenue fell 46 percent year-on-year due to lower plant utilization and the removal of the base plant from the generation mix. Gross margins compressed following the Narowal tariff revision and the loss of high-margin base plant earnings. Even so, profitability remained anchored by robust contributions from associates and joint ventures, which delivered Rs 10.8 billion, a 4 percent increase year-on-year, led by China Power Hub Generation Company and initial earnings from BYD’s local operations. Other income rose 26 percent, supported by higher dividends and improved recoveries.

Administrative expenses increased by more than 270 percent year-on-year, reflecting project-related costs associated with BYD and the Thar energy ventures. In contrast, finance costs declined 54 percent, aided by lower interest rates and repayment of project debt.

The earnings mix continues to shift toward CPEC-linked independent power projects—CPHGC, Thar Energy Limited, and ThalNova Power Thar. With both Thar projects approaching their Project Completion Date, HUBC is positioned to unlock new dividend streams in FY26, strengthening future cash flows.

Strategically, HUBC is evolving from a pure-play power producer into a diversified energy and industrial platform. The company has expanded its presence in Thar coal mining through SECMC, upstream oil and gas through Prime International, and minerals through Ark Metals. It is simultaneously building scale in electric mobility and green infrastructure, with the BYD Gharo CKD plant expected to come online in the second half of 2026 and an EV charging corridor planned along the Karachi–Peshawar motorway.

In parallel, HUBC is assessing commercial redevelopment opportunities for its 1,100-acre Hub site, including a potential aluminium smelter leveraging local bauxite and available energy, as well as a Single Point Mooring facility with PSO to enable efficient oil import handling through existing pipeline infrastructure.

Overall, HUBC’s 1QFY26 results reflect a business in transition: near-term earnings are softer due to structural changes, but medium-term prospects are supported by rising associate income, upcoming dividends from Thar projects, and diversification into higher-growth sectors such as electric vehicles, mining, and green energy.

Comments

Comments are closed for this article.