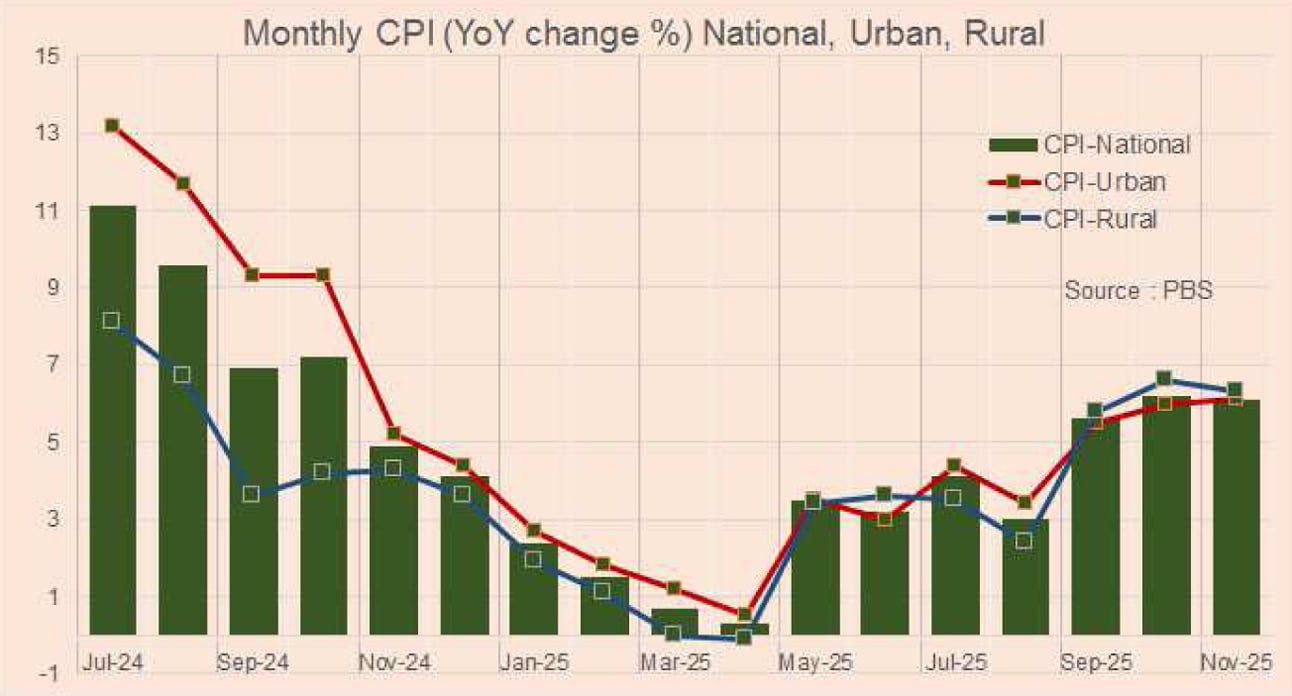

Headline inflation stood at 6.1 percent in November 2025, compared to 6.2 percent in the previous month. The CPI is lower than analysts’ expectations, which ranged between 6.5–7 percent.

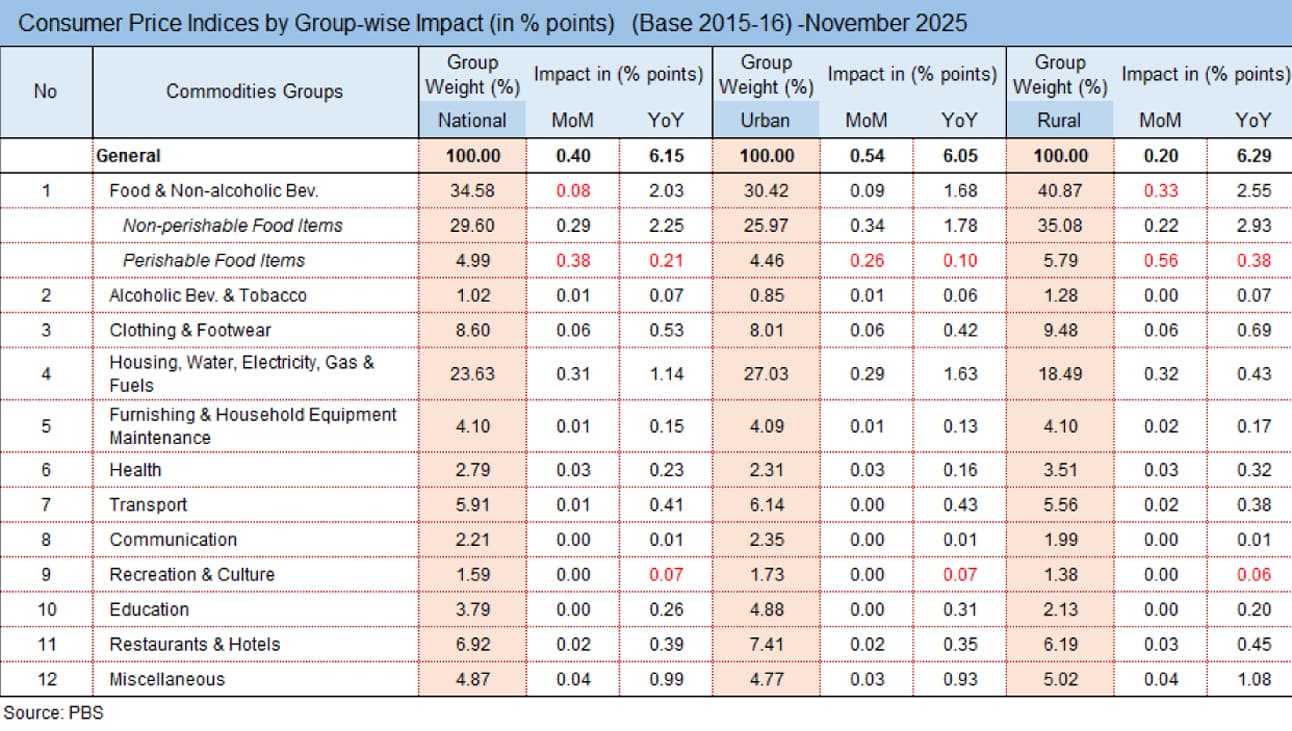

The lower-than-expected reading is due to a decline in food prices of 0.2 percent, whereas industry was expecting a surge of 0.6–0.8 percent. This is mainly due to a fall in perishable items, chiefly tomatoes, and a less-than-anticipated increase in wheat prices, which have started declining in recent weeks.

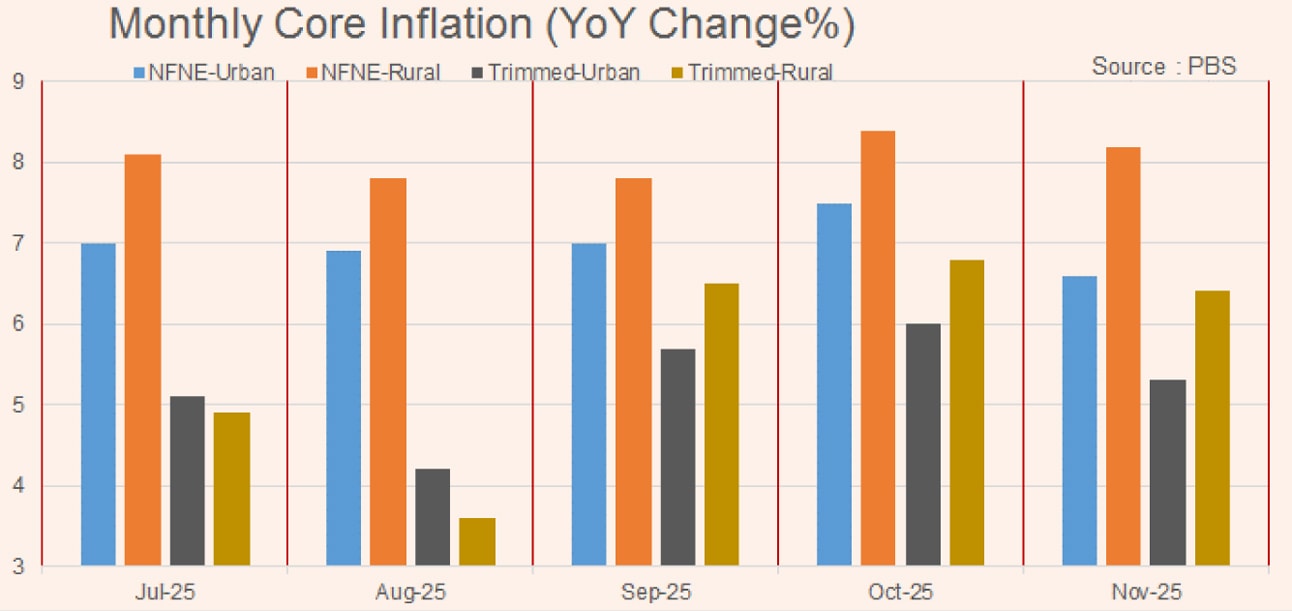

The good news is that core inflation came down to 7.4 percent in November from 7.9 percent in the previous month. The fall is due to a high base effect in last November where there was a one-time upward adjustment in health and footwear indices. Nonetheless, core inflation increased by 0.4 percent month-on-month in November, which is significantly lower than October’s increase of 1.2 percent.

There is a mixed trend in food inflation. Overall, on a monthly basis, the perishable food sub-index declined by 6.7 percent compared to an increase of 13.7 percent in the previous month.

The swing is mainly due to tomato prices, which in urban areas are down by 53.3 percent compared to an increase of 58.6 percent in the previous month. A similar trend is being witnessed in fresh vegetables, while onion prices continue to rise, up by 48 percent in November. Other notable monthly increases in food prices are in chicken, up by 17.4 percent, and eggs, up by 7.9 percent.

The housing and utility index is up by 5.3 percent year-on-year, while the monthly increase stood at 1.5 percent. That is mainly due to upward adjustments in electricity charges, which increased by 7.1 percent month-on-month.

The expiry of the previous quarter’s negative QTA of Rs 1.89 per KWh occurred despite having a negative FCA of Rs 0.48 per KWh. Thus, lower-than-reference consumption in 13 of the last 15 months is negating the impact of falling oil and energy commodity prices. This means that capacity payment per unit is bloating despite a stable currency.

The health price index is up by 1.1 percent month-on-month in November, while the yearly increase stood at 8.3 percent. The hike in prices is seen in medical tests, up by 19.4 percent, and drugs and medicines, up by 1.5 percent. The highest yearly increase is in miscellaneous items, up by 18 percent, while the monthly increase came in at 0.6 percent.

Overall inflation is settling down as wheat prices, which had increased over the past few months, are now tamed, while supply chain bottlenecks in perishable items are ironing out. Overall commodity prices, especially for energy, are low and that is helping to keep transportation and utility prices contained. There are no immediate pressures on core inflation either.

Having said that, base effect is in play in the last quarter of FY26 where headline inflation is likely to touch double digits. The average inflation in FY26 is likely to come closer to the upper band of SBP’s medium-term target of 5–7 percent, and similar is the number likely for core inflation.

Seeing a surge in inflation in the second half of FY26 compared to the first half, the SBP is likely to keep monetary policy tight, as real interest rate is positive by 3–3.5 percent on a 12-month forward-looking basis. Given the affinity of the regime to a sticky exchange rate, a tight monetary policy is warranted to keep the external account in control and to anchor inflationary expectations.

Comments

Comments are closed for this article.