Foreign Direct Investment weakened further in Oct-25, adding to concerns about Pakistan’s investment climate despite a few pockets of optimism. SBP data shows net FDI slipping to around $179 million for the month. The overall story hasn’t changed much: Pakistan continues to rely on a narrow set of countries and sectors for inflows, while outflows remain persistently high.

In the first four months of FY26, net FDI stood at $747 million, down sharply from $1.01 billion last year. Gross inflows crossed $1.2 billion, but almost $456 million flowed out in the form of profit repatriation and divestments — keeping net FDI under pressure.

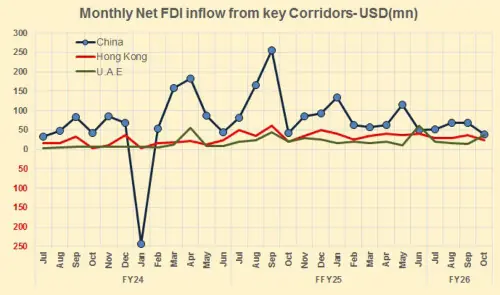

A large part of the decline comes from China and Hong Kong. Together, they contributed $368 million in 4MFY26, roughly half of what they brought in the same period last year ($712 million). Meanwhile, inflows from the “rest of the world” did rise — from $298 million to $410 million — which is encouraging, but still not enough to compensate for the pullback from China-linked investors.

Sectoral performance also paints a mixed picture. The power sector remains the biggest magnet for foreign capital, attracting $297 million in net FDI — but this is just half of last year’s levels, reflecting the completion of large CPEC power projects and the sector’s long-standing financial issues. The financial sector continues to hold steady, drawing $260 million, supported by strong profitability and ongoing reforms.

The communications sector, however, remains a drag. Net FDI fell to –$23 million in 4MFY26, compared to –$11 million last year. Much of this is driven by telecom operators repatriating profits — a reflection of high spectrum costs, and other structural challenges. The IT and software sectors did receive $13.7 million, but the scale remains far below what comparable economies attract or what could offset the decline in telecom sector.

October itself followed the same pattern: inflows of around $318 million, outflows of about $140 million, and a net number that continues to move sideways. Chinese inflows also show clear volatility — a strong rebound in mid-FY25, followed by a steady cooling off as FY26 began.

Three things stand out from the recent trend. First, interest from non-China investors exists, but confidence is fragile.Second, repatriation outflows remain a drag: high profit outflows, especially in telecom and consumer sectors, erode the gains from new capital inflows. Third, investors continue to point to policy unpredictability, regulatory burden, delayed payments in the power sector, and inconsistent taxation as barriers to long-term commitments.

FDI will likely remain subdued in the coming months. Macroeconomic stabilization—IMF program adherence, reserve buildup, and improved FX flexibility—prevents a drastic fall.

But without clear movement on structural reforms, energy sector liabilities, and contract enforcement, Pakistan will continue to attract short-term or strategic capital from a narrow set of partners rather than broad-based, productivity-enhancing investment.

The challenge for policymakers is clear: convert stabilization into confidence, and confidence into capital. Without this shift, FDI will remain stuck in low gear through FY26.

Comments

Comments are closed for this article.