Fazal Cloth Mills Limited (PSX: FZCM) was incorporated in Pakistan as a public limited company in 1966. The principal activity of the company is the manufacturing and sale of yarn and fabric.

Pattern of Shareholding

As of June 30, 2025, FZCM has a total of 30 million shares outstanding which are held by 1491 shareholders. Associated companies, undertakings and related parties have the majority stake of 66.60 percent in the company followed by directors, CEO, their spouse, and minor children accounting for 22.66 percent shares. Around 5.90 percent of FZCM’s shares are held by NIT & ICP and 3.98 percent by local general public. The remaining shares are held by other categories of shareholders.

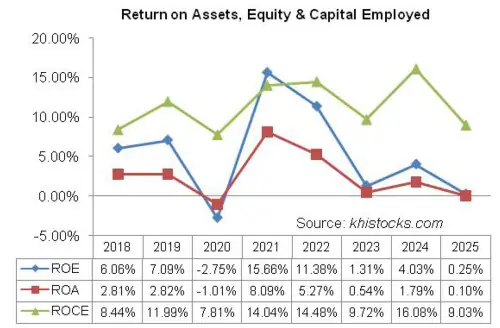

Historical Performance (2019-25)

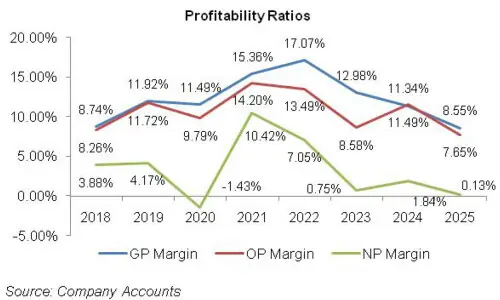

Except for a year-on-year decline in 2025, FZCM’s topline expanded over the period under consideration. Conversely, its bottomline posted growth only in 2019, 2021 and 2024. In 2020, the company posted net loss. Its margins, which registered a noticeable growth in 2019, dropped in 2020 followed by a sound recovery in 2021.

In 2022, gross margin enhanced while operating and net margins dipped. FZCM’s margins posted a drastic decline in 2023. This was followed by an even weaker gross margin in 2024, while operating and net margins ticked up during the year. In 2025, all the margins hit their lowest level. The detailed performance review of the period under consideration is given below.

In 2019, FZCM’s posted 16.15 percent year-on-year growth in its topline which clocked in at Rs.36,341.10 million. This was the result of increase inthe prices and sales volume. Pak Rupee depreciation also played a pivotal role in driving up the company’s export revenue. Cost of sales grew by a lesser margin of 12.11 percent during the year due to availability of electricity and gas at regionally competitive rates.

This resulted in 58.35 percent higher gross profit in 2019 with GP margin jumping up from 8.74 percent in 2018 to 11.92 percent in 2019. Selling & distribution expense slumped by 20.82 percent in 2019 due to lower commission, surcharge and insurance paid on export sales. Administrative expense grew by 8.76 percent in 2019 due to higher payroll expense, vehicle running & maintenance charges, repair & maintenance charges, and depreciation expense incurred during the year.

Other expense mounted by 78.63 percent in 2019 on the back of higher profit related provisioning, loss on disposal of fixed assets, unrealized loss on the revaluation of investment at FVTPL and allowance booked for the impairment of trade debts.

The effect of other expense was completely wiped off by 26.56 percent higher other income recorded by FZCM in 2019 on account of exchange gain and mark-up recognized on advances to associated undertaking. Operating profit strengthened by 64.73 percent in 2019 with OP margin climbing up from 8.26 percent in 2018 to 11.72 percent in 2019.

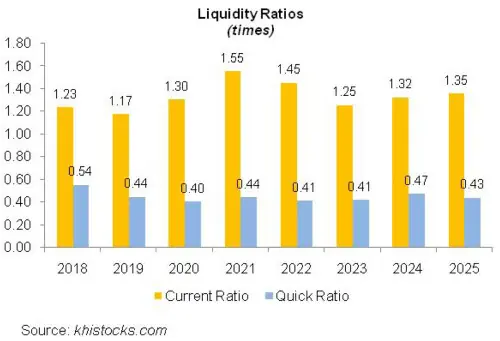

Finance cost mounted by 65.59 percent in 2019 due to higher discount rate and increased borrowings. FZCM’s gearing ratio grew from 47 percent in 2018 to 51 percent in 2019. Net profit picked up by 24.89 percent in 2019 to clock in at Rs.1515.50 million with EPS of Rs.50.52 versus EPS of Rs.40.45 recorded in 2018. NP margin also improved from 3.88 percent in 2018 to 4.17 percent in 2019.

In 2020, FZCM’s topline grew by 9.28 percent to clock in at Rs.39,713.74 million. The company’s local and exports sales volume considerably declined during the year due to COVID-19. Pak Rupee depreciation, however, resulted in greater export sales in Rupee terms.

Cost of sales grew by 9.82 percent in 2020, resulting in 5.30 percent higher gross profit recorded during the year. GP margin slightly ticked down to 11.49 percent in 2020. Selling & distribution expense mounted by 71.26 percent in 2020 due to considerably higher commission paid on both local and export sales.

Administrative expense ticked up by 12.65 percent in 2020 due to higher payroll expense on account of inflation as well as expansion in workforce from 4627 employees in 2019 to 4897 employees in 2019. Other expense increased by 175.42 percent in 2020 due to higher exchange loss incurred during the year. Other income showed no significant movement in 2020.

Operating profit tapered off by 8.72 percent in 2020 with OP margin falling down to 9.79 percent. Finance cost grew by 55.46 percent in 2020 due to higher discount rate for most part of the year and increased borrowings which resulted in gearing ratio of 53 percent. FZCM recorded net loss of Rs.569.496 million in 2020 with loss per share of Rs.18.98.

In 2021, FZCM registered topline growth of 31.27 percent. This took its net sales up to Rs.52,132.24 million in 2021 This was predominantly the result of improved international demand of textile products after COVID-19 coupled with a rebound in local and international prices.

Cost of sales grew by 25.53 percent due to availability of energy at regionally competitive rates and the company’s ability to procure raw materials at reasonable rates amid high commodity prices. Gross profit strengthened by 75.50 percent in 2021 with GP margin attaining a new high level of 15.36 percent.

Selling & distribution expense slid by 2.78 percent in 2021 due to lower export commission incurred during the year. Increase in the number of employees to 5705 in 2021 coupled with inflationary pressure resulted in 16.82 percent higher administrative expense in 2021. Higher profit related provisioning and present value adjustment of long-term loans resulted in 8.76 percent higher other expense in 2021.

Other income fell by 5.91 percent in 2021 due to lower mark-up income on advances to the associated undertaking, Fatima Energy Limited and no gain recorded on disposal of equity instruments of associate. During the year, the company discontinued equity accounting on its investment in Fatima Energy Limited and recognized gain of Rs.216.80 million as the difference between carrying amount and fair market value of investment.

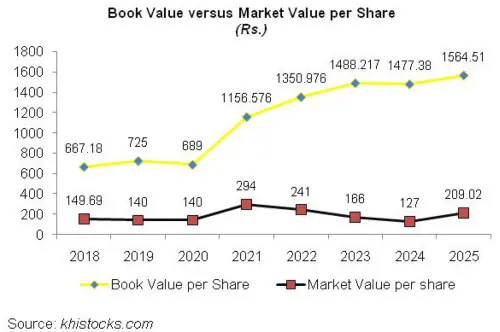

The company recorded 90.49 percent higher operating profit in 2021 with OP margin climbing up to 14.20 percent – the highest level recorded during the period under consideration. Finance cost shrank by 39 percent in 2021 due to monetary easing and reduced borrowings on account of improved liquidity position of the company. Gearing ratio fell to 40 percent in 2021. FZCM recorded the highest ever net profit of Rs.5431.76 million in 2021 with EPS of Rs.181.06 and NP margin of 10.42 percent.

FZCM’s topline mounted by 25.46 percent to clock in at Rs.65,406.26 million in 2022. This was primarily the result of unabated decline in the value of local currency which increased the value of export sales in Rupee terms. Cost of sales grew by 22.91 percent in 2022, resulting in 39.51 percent higher gross profit and the highest ever GP margin of 17.10 percent.

Selling & distribution expense surged by 59.27 percent in 2022 due to higher commission paid on both local and export sales and elevated export development surcharge incurred during the year.

Administrative expense escalated by 28.94 percent in 2022 due to higher payroll expense as number of employees increased to 6934 in 2022. 161.60 percent higher other expense incurred during 2022 was the result of higher profit related provisioning, exchange loss, sales tax receivable written off and loss allowance booked on long-term mark-up accrued.

Other income slid by 12.91 percent in 2022 due to no exchange gain, no notional gain on discounting of GIDC payable and lower mark-up on advances to Fatima Energy Limited. Operating profit grew by 19.14 percent in 2022; however, OP margin slipped to 13.50 percent.

Higher discount rate coupled with increased borrowings resulted in 62.85 percent higher finance cost in 2022. This resulted in a gearing ratio of 46 percent in 2022. Imposition of super tax also proved to be detrimental for FZCM in 2022, squeezing its bottomline by 15.12 percent. Net profit stood at Rs.4610.26 million in 2022 with EPS of Rs.153.68 and NP margin of 7.05 percent.

In 2023, FZCM posted topline growth of 18.79 percent. This translated into sales of Rs.77,696.98 million in 2023. Despite global economic slowdown, the company’s sales volume slightly improved during the year. However, elevated prices of raw materials due to Russia-Ukraine crisis coupled with Pak Rupee depreciation and heightened energy tariff took its toll on the gross profit of the company which diluted by 9.69 percent year-on-year in 2023. GP margin drastically fell to 12.98 percent in 2023. Selling & distribution expense incurred during the year were 16 percent lower when compared to last year’slevel due to lower sales commission and lower export development surcharge. Administrative cost multiplied by 18.15 percent in 2023 primarily due to higher payroll expense on account of inflation. Other expense mounted by 49.22 percent in 2023 due to whopping exchange loss incurred during the year. Other income dipped by 33.39 percent in 2023 as the company recognized no mark-up income on advances and recorded no gain on re-measurement of short-term investment. FZCM recorded 24.40 percent thinner operating profit in 2023 with OP margin slipping to 8.58 percent. Finance cost magnified by 73.62 percent in 2023 due to unprecedented level of discount rate and increased outstanding liabilities which resulted in gearing ratio mounting to 51 percent. The company’s bottomline contracted by 87.29 percent in 2023 to clock in at Rs.586.094 million with EPS of Rs.19.54 and NP margin of 0.75 percent.

FZCM’s topline registered 25.05 percent rebound to clock in at Rs. 97,160.88 million in 2024. This was on the back of improved sales volume of yarn. Conversely, sales volume of fabric dropped during the year. Surge in the prices of raw materials aswell as towering energy tariff pushed the cost of sales up by 27.41 percent in 2024. This resulted in GP margin dropping further to 11.34 percent in 2024, despite 9.23 percent uptick in gross profit in absolute terms. Selling & distribution expense surged by 12.58 percent in 2024 due to higher export development surcharge, higher commission on local sales and higher salaries of marketing staff. Administrative expense also multiplied by 26.79 percent in 2024 primarily due to higher payroll expense This was despite the fact that the company streamlined its workforce to 6538 employees in 2024 from 6927 employees in the previous year. The company recorded 93.33 percent lower than other expense in 2024 due to no exchange loss incurred during the year. The effect of other expense was completely wiped off by 345.45 percent higher other income recorded during the year. This was the result of exchange gain, gain on de-recognition of mark-up upon conversion into preference shares, reversal of loss allowance booked against long-term advances, gain on re-measurement of short-term investment and as well as higher dividend received from Fatima Fertilizer Limited. Operating profit improved by 67.39 percent in 2024 with OP margin rising up to 11.49 percent which was even bigger than the GP margin for the year – thanks to hefty other income. Finance cost surged by 64.30 percent in 2024 due to higher discount rate while outstanding liabilities ticked down resulting in a gearing ratio of 46 percent. Net profit registered an impressive growth of 204.61 percent in 2024 to clock in at Rs.1785.286 million with EPS of Rs.59.51 and NP margin of 1.84 percent.

Unlike all the years under consideration where FZCM’s topline ascended, in 2025, the topline dwindled by 7.37 percent to clock in at Rs.90,002.39 million. Heavy influx of duty-free imported yarn destroyed the local demand of yarn which took a heavy toll on the sales volume of the company. The sales volume of fabric marginally improved during the year, however, couldn’t help the topline. High cost of raw materials which constituted 72.95 percent of the company’s entire cost of sales and elevated power cost which constituted 13.85 percent of the company’s cost of sales squeezed FZCM’s gross profit by 30.14 percent in 2025. GP margin fell to its lowest level of 8.55 percent in 2025. Lower sales volume culminated into 7.68 percent thinner distribution expense in 2025. Administrative expense escalated by 15.32 percent in 2025 particularly on the basis of higher payroll expense, travelling & conveyance charges, depreciation expense as well as repair & maintenance charges incurred during the year. FZCM considerably streamlined its workforce from 6538 employees in 2024 to 6048 employees in 2025. Other expense mounted by 70.27 percent in 2025 due to massive exchange loss as well as loss incurred on the disposal of property, plant & equipment. While other income dwindled by 45.57 percent in 2025, it easily offset other expense. The decline in other income was due to high-base effect as the company recorded exchange gain, gain on de-recognition of mark-up upon conversion into preference shares and reversal of loss allowance booked against long-term advances in the previous year. Operating profit deteriorated by 38.35 percent in 2025 with OP margin falling down to 7.65 percent. Monetary easing pushed down financed cost by 36.72 percent in 2025. Outstanding debt increased during the year resulting in a gearing ratio of 51 percent in 2025. Net profit drastically fell by 93.44 percent to clock in at Rs.117.138 million in 2025. This resulted in EPS of Rs.3.90 and NP margin of 0.13 percent in 2025.

Recent Performance (1QFY26)

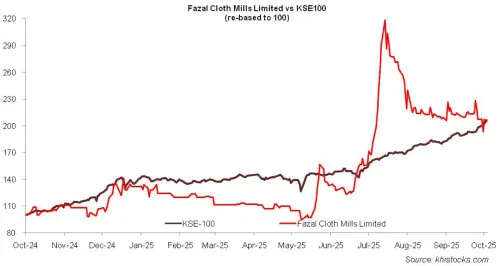

During the first quarter of the ongoing fiscal year, the company posted a year-on-year uptick of 0.61 percent in its net sales which clocked in at Rs.24,333.55 million. This came on the back of an increase in direct exports during the period while local sales and indirect exports tumbled during 1QFY26. Decrease in yarn prices internationally didn’t allow the company to increase its prices. This coupled with appreciation in the value of local currency squeezed the value of export sales in Rupee terms and resulted in 21.59 percent deterioration in gross profit in 1QFY26. GP margin also diminished from 9.41 percent in 1QFY25 to 7.34 percent in 1QFY26. Selling & distribution expense fell by 34 percent in 1QFY26 due to thinner sales volume. Conversely, administrative expense ticked up by 9.33 percent in 1QFY26 due to inflationary pressure and adjustment of minimum wage rate. Exchange loss on export sales appears to be the cause of 229.53 percent higher other expense in 1QFY26, however, it was offset by 71.64 percent higher other income recorded during the period which might be due to higher dividend income. FZCM recorded 15.81 percent lower operating profit in 1QFY26 with OP margin clocking in at 7.49 percent versus OP margin of 8.95 percent recorded in 1QFY25. Monetary easing allowed the company to squeeze its finance cost by 13.48 percent in 1QFY26. Net profit clocked in at Rs.179.57 million in 1QFY26, down 45.92 percent year-on-year. This translated into EPS of Rs.5.99 in 1QFY26 versus EPS of Rs.11.07 in 1QFY25. NP margin slid from 1.37 percent in 1QFY25 to 0.74 percent in 1QFY26.

Future Outlook

Pakistan has kicked off FY26 on a stable note with decent improvement in macroeconomic indicators setting tone for a resilient future. This will likely improve the demand for textile products both in the local and export market. Stability in the value of local currency and decline in inflation will reduce the cost of the company. Monetary easing will also pave way for a thinner finance cost.

The decline in tariffs on Pakistani exports by the US government from 29 percent to 19 percent will give the local manufacturers an edge over their regional counterparts who have been slapped with considerably higher tariffs. The company also plans to add 29 MWh of solar energy capacity which will take the total solar capacity to 51.2 MWh and will be able to meet 21 percent of the company’s energy requirements. All these factors will result in improved sales revenue and healthier bottomline and margins.

On the flipside, adverse weather conditions can affect the local cotton production resulting in higher cotton prices. This will provide a competitive benefit to imported yarn as international cotton prices have significantly receded in FY26 and will continue to remain the same for the remaining part of the year.

Comments

Comments are closed for this article.