For nearly two years now, currency has been kept on a short leash:nominally stable, yet effectively managed. Exporters can see what the charts already show: an exchange rate that has been frozen in time long enough to lose credibility.

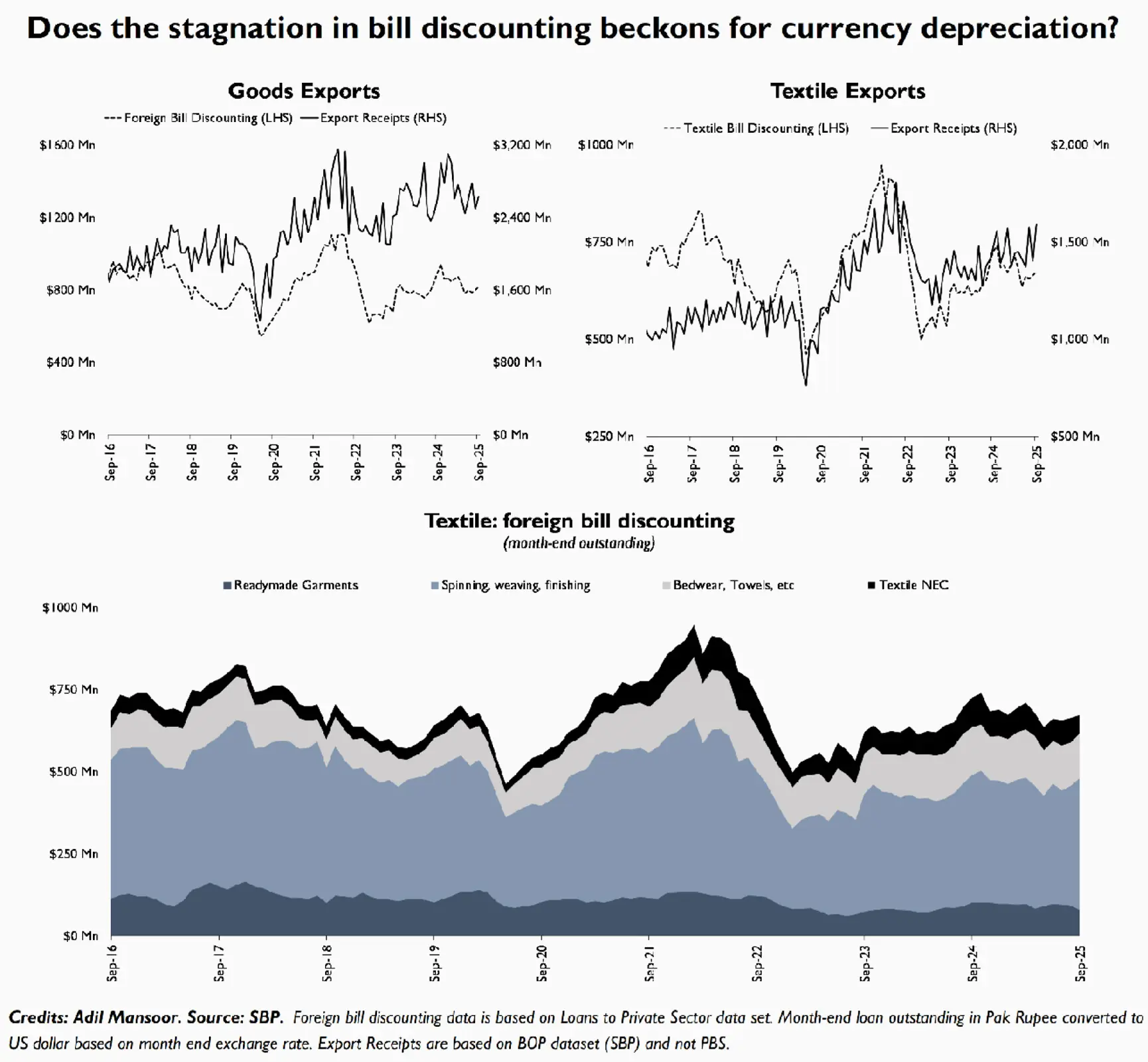

This behaviour reflects that view. Export shipments may not be in freefall yet, but foreign bill discounting remains subdued. In the past twelve months, total exports have inched up barely two percent. During the same period, textile bill discounting has fallen nine percent,while non-textile discounting has plunged by one-third.

The discounting-to-exports ratio has slipped 14 percent. That is not a liquidity issue; it is an indefinite pause. Exporters are holding dollars because they appear certain that currency must adjust, sooner rather than later.

The short-term data makes the same point. Between Jul-Sep 2025, overall exports dropped more than five percent while textile exports barely inched up by a percentage point. Similarly, discounting volumes are stagnant, signalling that exporters prefer to finance themselves offshore rather than convert at home.

Six-month averages tell the same story: receipts are stagnant, but the willingness to part with dollars is even weaker.What once looked like hesitation is now possibly a hardened position. With inflation beginning to creep back up and the policy rate held in stasis, and administrative controls keeping the currency in check, exporters are doing what rational actors do in a managed regime: they wait for the break.

The consequences are already visible. Exporters are not speculating; they are protecting value. Converting today makes little sense when the future rate is expected to be higher.Market participants, particularly appear increasingly inclined to see currency as mispriced.

The policy instinct, however, remains to moralise. State actors lean on kerb market, nudging them to surrender forex liquidity, managing the rate in the name of stability. The irony is that this very stability is what deters conversion. A rate that refuses to move in either direction loses its informational value. When the market stops believing in the price, it stops participating.

There is no mystery here. A currency that has barely budged for twenty-four months despite double-digit inflation and widening fiscal pressures is, by definition, over-managed. Exporters know it. Importers know it. The only people pretending otherwise are policymakers still hoping that optics can outlast arithmetic.

When the correction comes, as it always does, the same exporters will suddenly “bring dollars back,” hailed again as patriots. Until then, the data will keep showing what it shows now: a steady fall in discounting volumes, forward premium, and muted receipts despite active trade.

The rupee’s biggest problem is not speculation; it is absence of faith. Exporters are simply voting with their timing, signalling that a currency kept artificially stable for too long is no longer credible. Whether policymakers acknowledge that signal before the market forces correction is the only suspense left.

Comments

Comments are closed for this article.