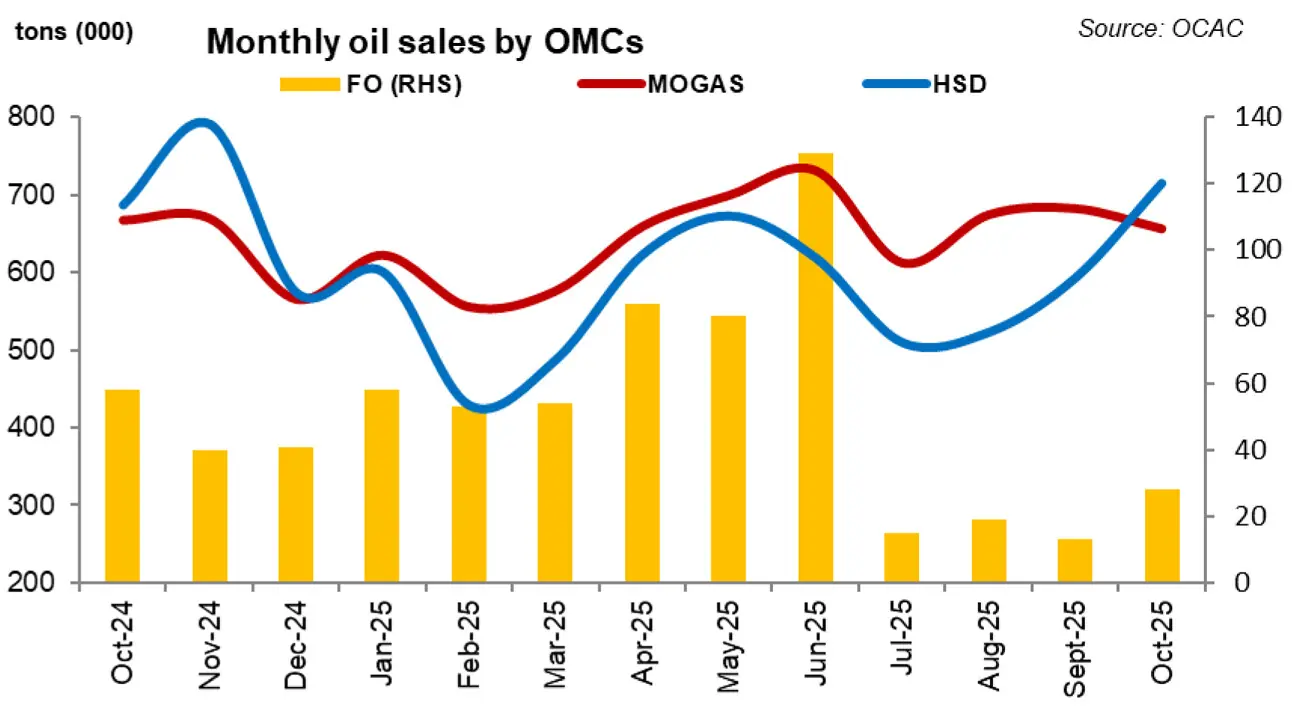

The oil marketing companies (OMCs) posted flattish overall sales in October 2025 at 1.50 million tons, compared to 1.49 million tons in the same month last year, though volumes were up 9 percent month-on-month, reflecting a seasonal lift from the Rabi sowing cycle.

Excluding furnace oil (FO), sales rose 2 percent year-on-year and 8 percent month-on-month driven by stronger demand for high-speed diesel (HSD).

HSD volumes increased 4 percent year-on-year and 21 percent over September supported by farm activity, improved enforcement against smuggled Iranian fuel, and better farm economics.

Motor spirit (MS) sales, however, slipped 2 percent year-on-year and 4 percent month-on-month, as retail prices were up about 8 percent year-on-year—affecting consumption.

Furnace oil volumes continued their structural decline, plunging 52 percent year-on-year to 28,000 tons, as the power sector’s reliance on FO-based generation diminished.

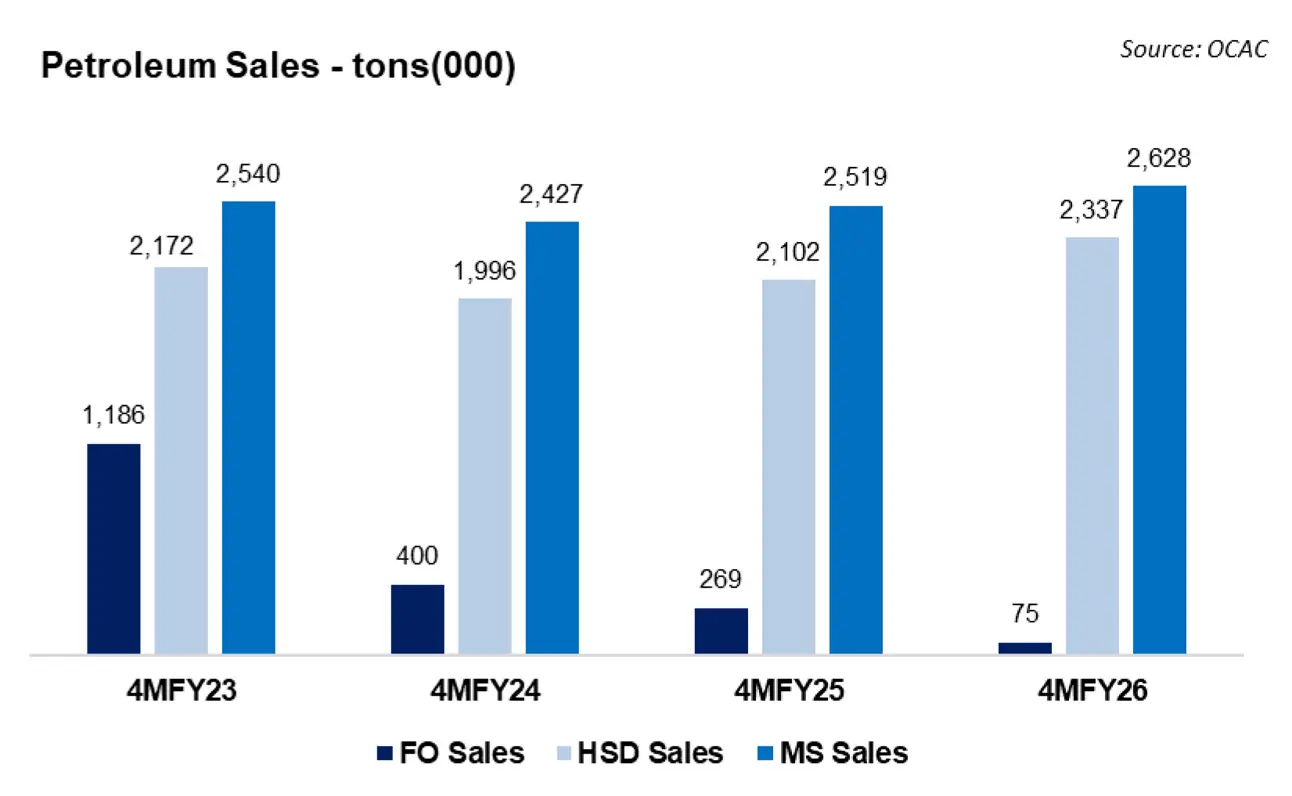

Cumulatively, petroleum sales in 4MFY26 grew 4 percent year-on-year to 5.39 million tons, while excluding FO volumes rose a stronger 8 percent year-on-year. Product-wise, MS sales were up by 4 percent year-on-year, HSD up by 11 percent year-on-year, and FO down 72 percent.

The overall growth in diesel demand reflected improved farm activity and gradual stabilization in industrial and transport sectors, while gasoline consumption remained subdued amid higher prices and weak purchasing power. The continued slump in FO consumption was consistent with lower demand from the power sector and policy disincentives, including a petroleum development levy.

Going forward, market expects the OMC volumes to grow in the range of 7–10 percent in FY26, contingent on economic stability, consistent farm sector activity, and controlled smuggling across the western border. Petroleum levy will keep retail prices elevated and may temper urban consumption.

Seasonal factors, particularly the ongoing Rabi cycle and potential winter demand for diesel in logistics and heating, should sustain near-term volumes. However, high financing costs, narrowing margins, and continued substitution away from furnace oil are likely to keep the overall growth trajectory moderate.

Comments

Comments are closed for this article.