Pakistan’s electricity grid is fast turning into a case study — on the democratization of energy choices, on the consequences of hasty, short-sighted policy, and on a perennial inability to read the room. Irrelevance may not be imminent, but losing relevance is already happening — and gathering pace.

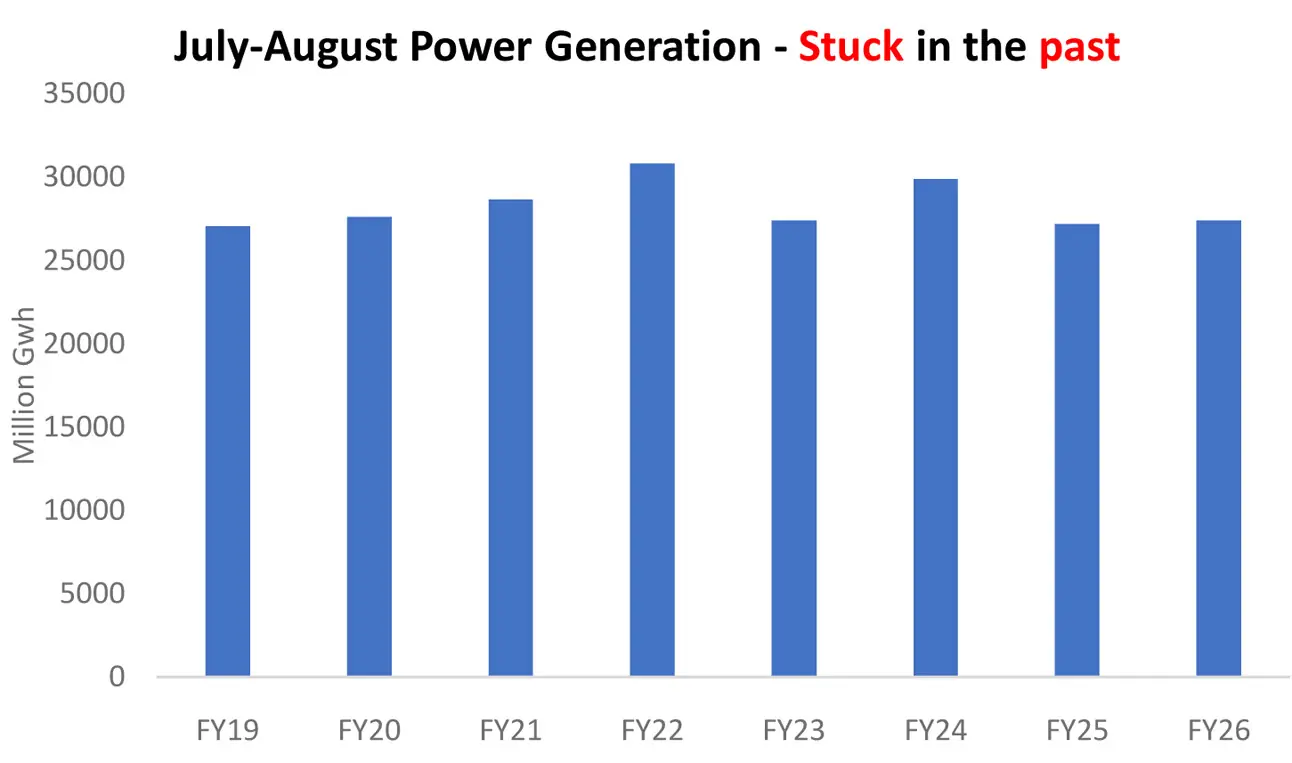

Take August 2025. Headline generation of 13.7 billion units, up 7.5 percent year-on-year, looks like a revival on the surface.

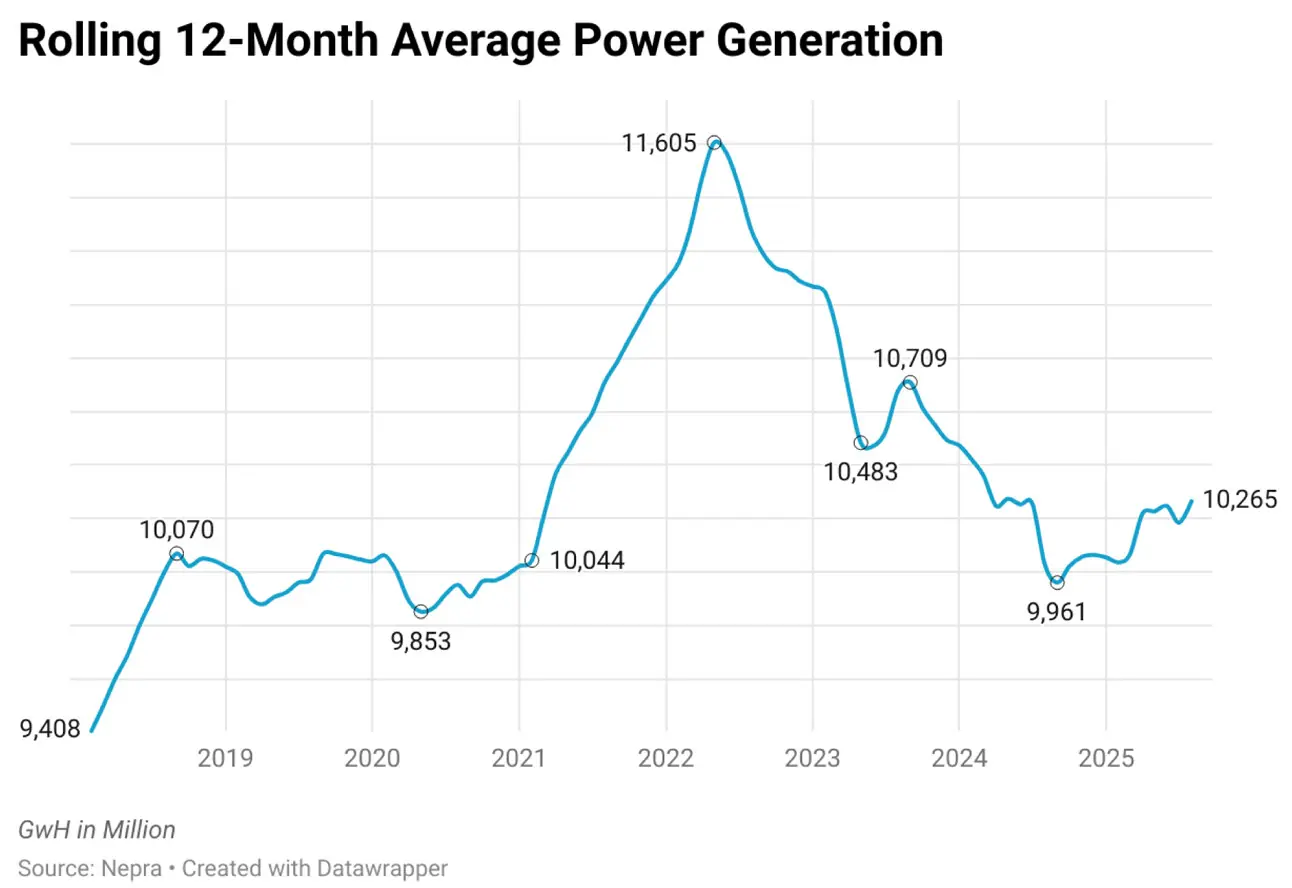

Scratch deeper, and the optimism fades. August 2025 generation is still lower than 2019, and barely ahead of 2018. Electricity demand does not stagnate over seven years in normal economies.

Even war zones often post growth. Pakistan’s official numbers suggest otherwise — but demand has not disappeared. It has simply moved.

Years of inflation, tariff hikes, and policy missteps have nudged users toward alternatives. Some have exited the grid altogether, others run hybrids. The majority remain tied — or stuck — to the grid. But storage technology is racing ahead, and grid loyalty will not last forever.

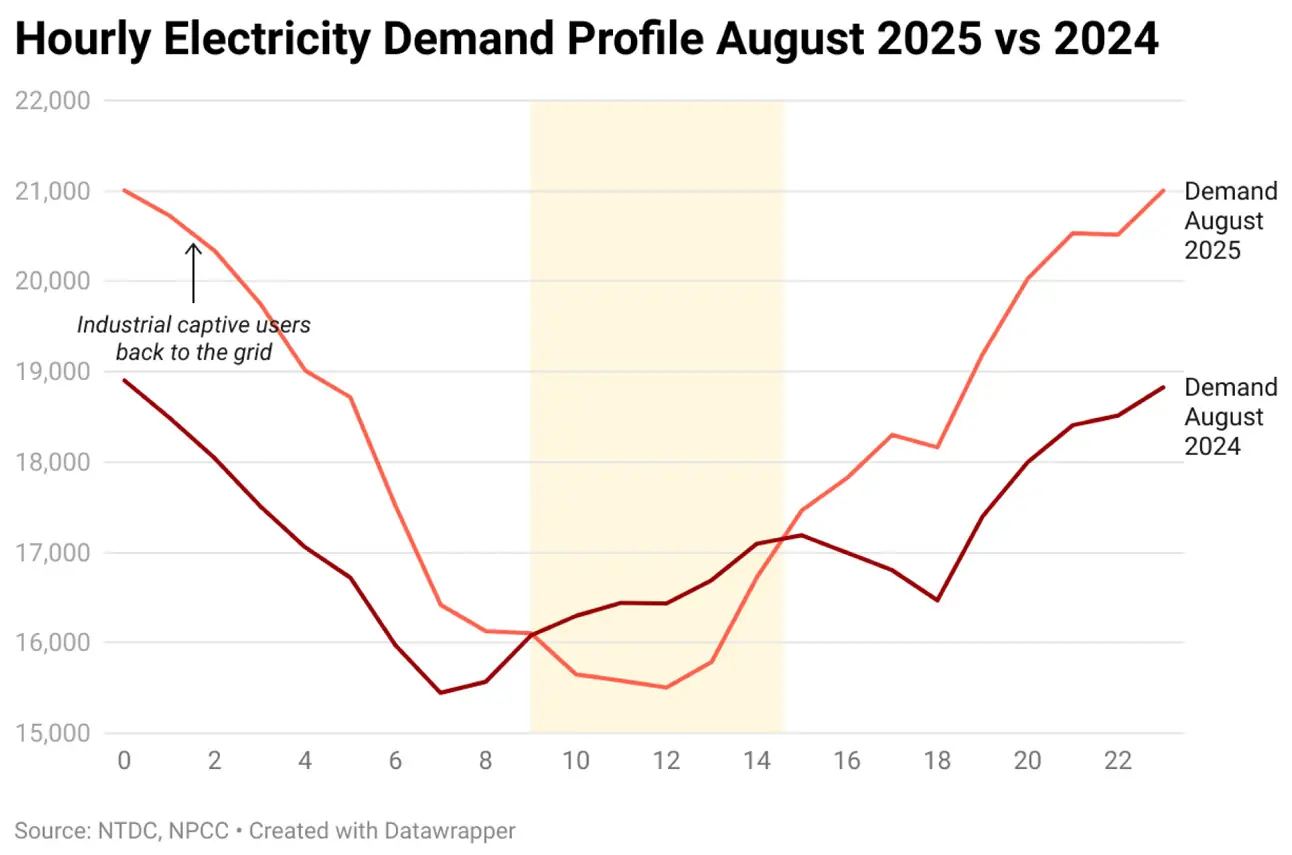

The one bright spot for the grid is the return of captive industrial users. With IMF-driven LNG pricing rendering private generation unviable, industries have crept back to grid supply.

The impact is visible almost instantly in higher industrial draw. These are the consumers the system needs most — the best payers — and their re-entry is not trivial.

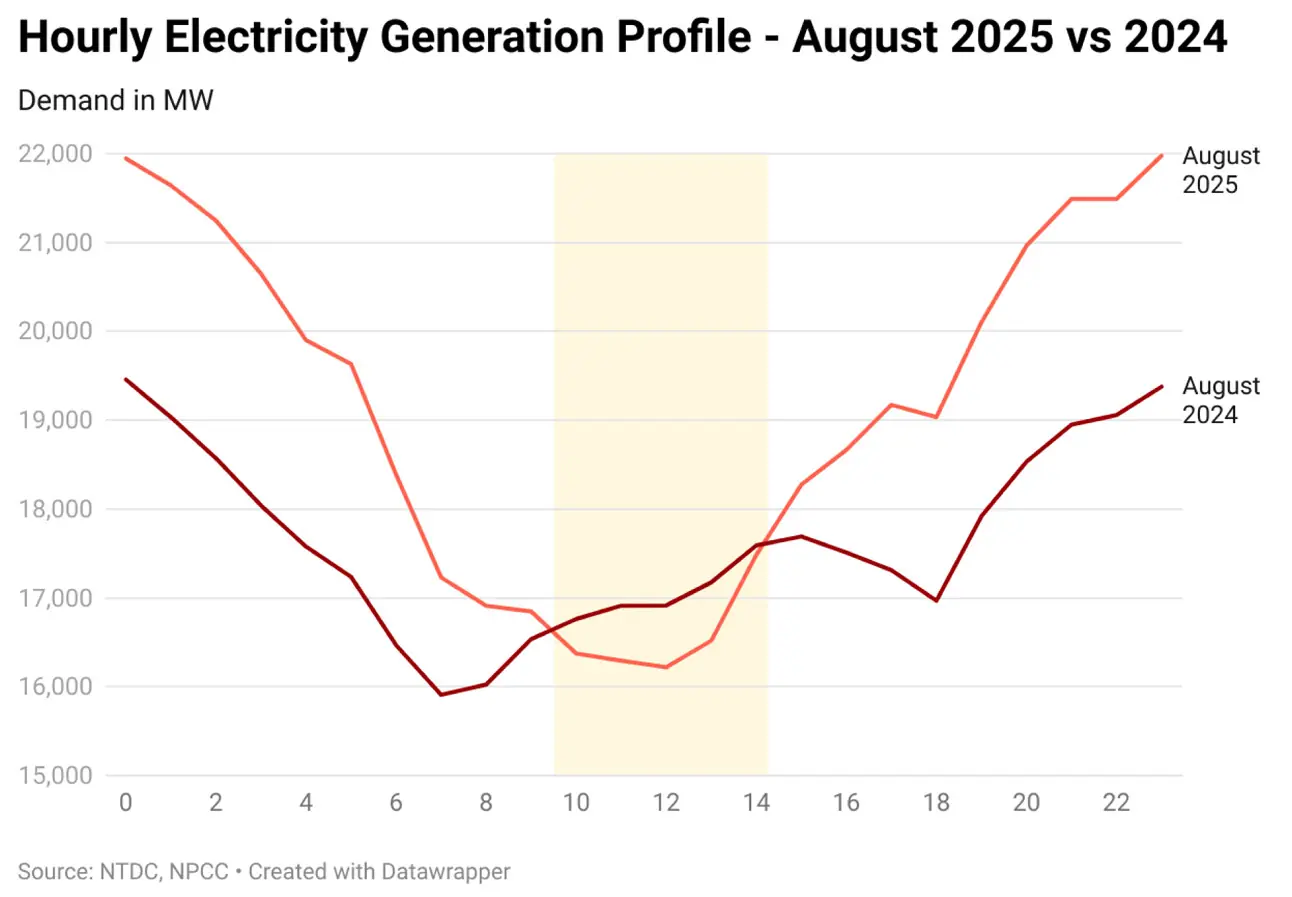

Yet, the demand curve tells its own tale. Despite a 2,000 MW jump in peak demand compared to last year, daytime loads continue to slip — a textbook sign of growing rooftop solar adoption in households and commercial setups. The “duck curve” is now unmistakable. And it comes with a cost.

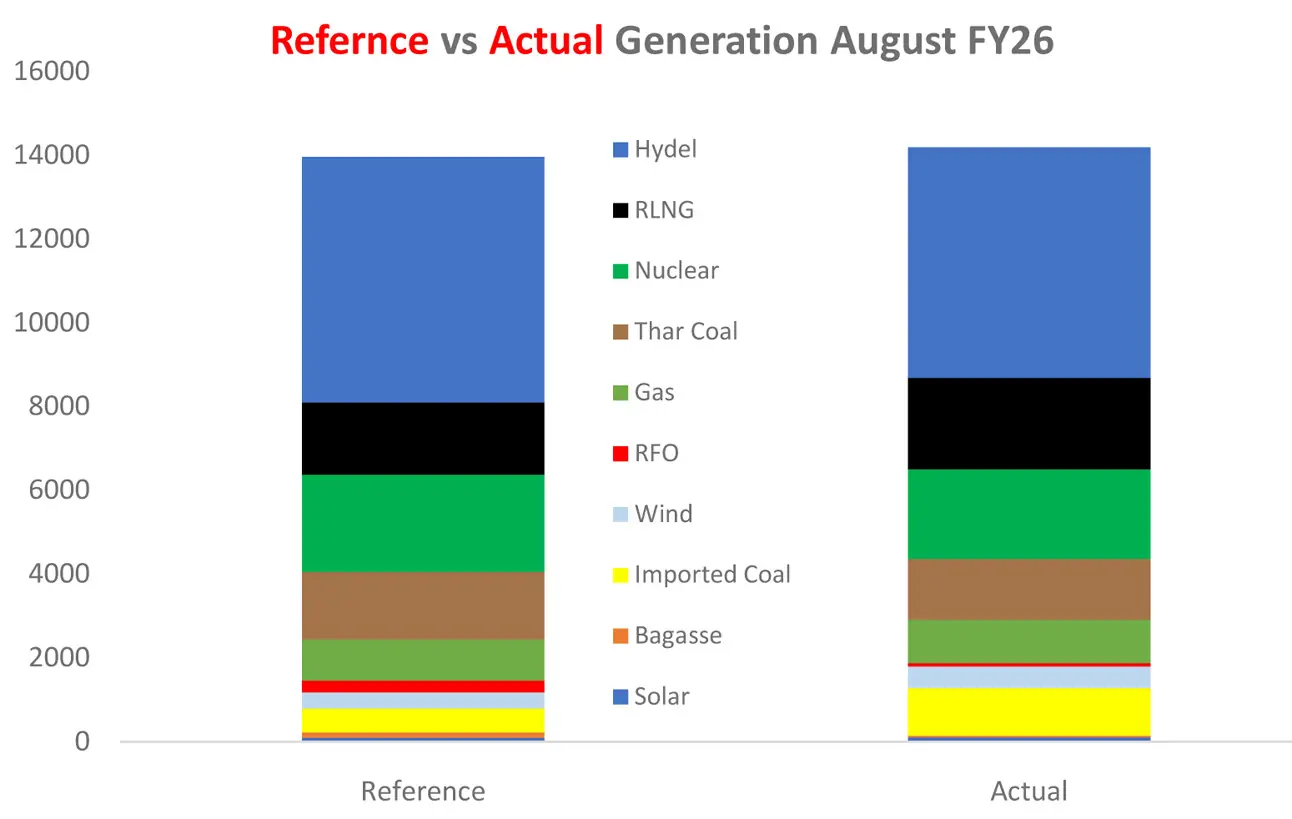

As the sun sets, the grid scrambles to fill the gap, often firing up the most expensive plants first. RLNG and imported coal — the costliest parts of the fleet — recorded generation deviations of nearly a billion units from their reference levels in August. Had these run closer to reference, the monthly FCA would have dropped by Rs1–2/unit. Instead, consumers face yet another upward adjustment.

This is the vicious cycle. Solar takes away the grid’s cheapest hours. The grid responds with expensive peak. Costs rise. More users defect to solar. Repeat. For policymakers, the task ahead is obvious but not easy: make the grid reliable and affordable, fast. Reliability matters more than ever if industry is to stay connected, and industry is the only segment that can stabilize financials.

But the more domestic and commercial users reduce reliance, the tougher it becomes to spread fixed costs.

The financial mess deepens, raising the question: who will buy the discos, even the “good” ones, if the consumer base keeps thinning out?

The August numbers show growth on paper, but the hourly profiles and marginal costs reveal a deeper truth: Pakistan’s grid is not losing demand, it is losing relevance.

And unless course correction comes soon, the hardest part won’t be keeping the lights on — it will be finding anyone willing to stay plugged in.

Comments

Comments are closed for this article.