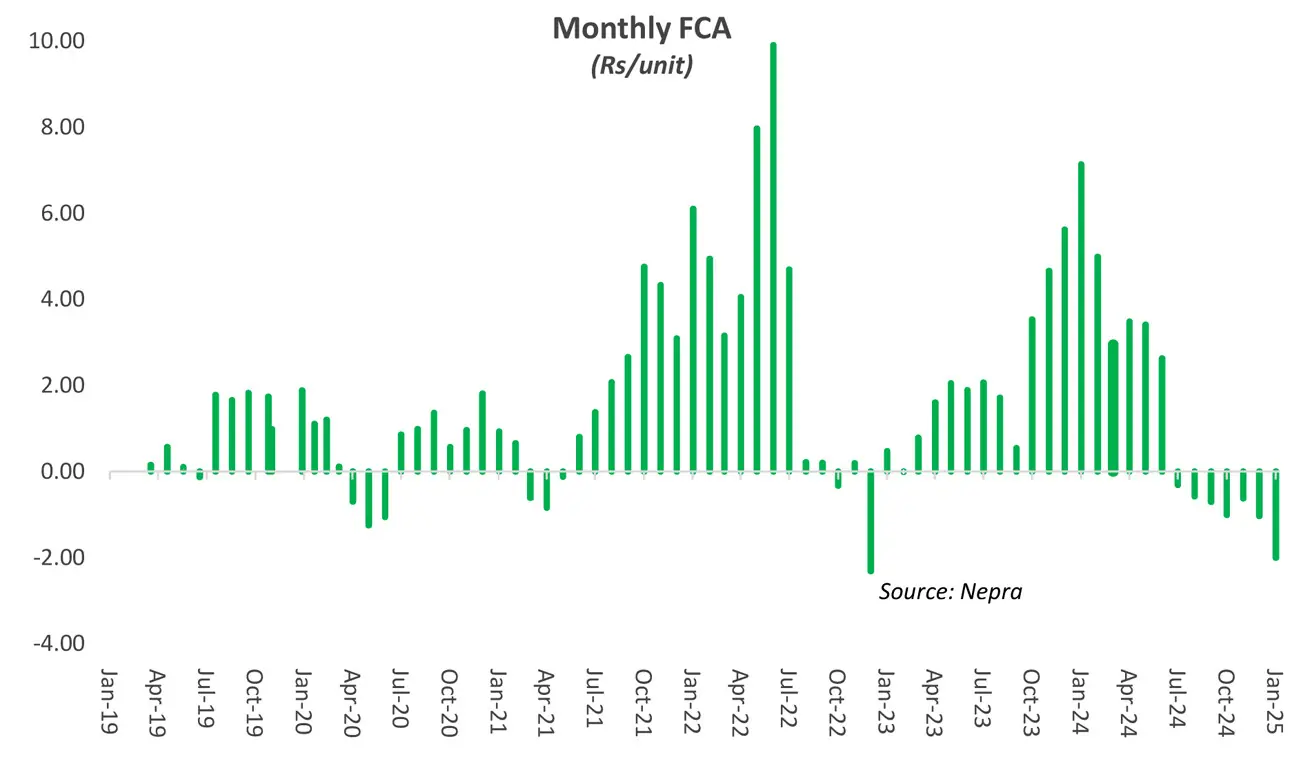

A sizeable relief has been approved in lieu of the July 2025 Fuel Charges Adjustment (FCA), at negative Rs1.79/unit. This marks the steepest negative adjustment since January 2025, and the largest for July in a decade.

The savings stem largely from a better-than-referenced generation mix, even though actual generation fell 10 percent short of projections.

Hydel generation exceeded the reference by 7 percent, lifting its share to 40 percent against the envisaged 33 percent, pulling fuel costs lower. RLNG-based generation, meanwhile, was 19 percent below reference, as daytime load remained weak and demand for RLNG off-take fell.

What has gone largely unnoticed is the steady decline in daytime grid load, displaced by the rapid adoption of solar solutions.

Overall electricity demand has risen, as evident from record solar PV imports — over $2 billion worth in 2024 from China alone. Yet daytime demand on the grid has eased, offsetting the surge in peak nighttime demand, which touched nearly 1,000 MW higher in July 2025 compared to a year earlier.

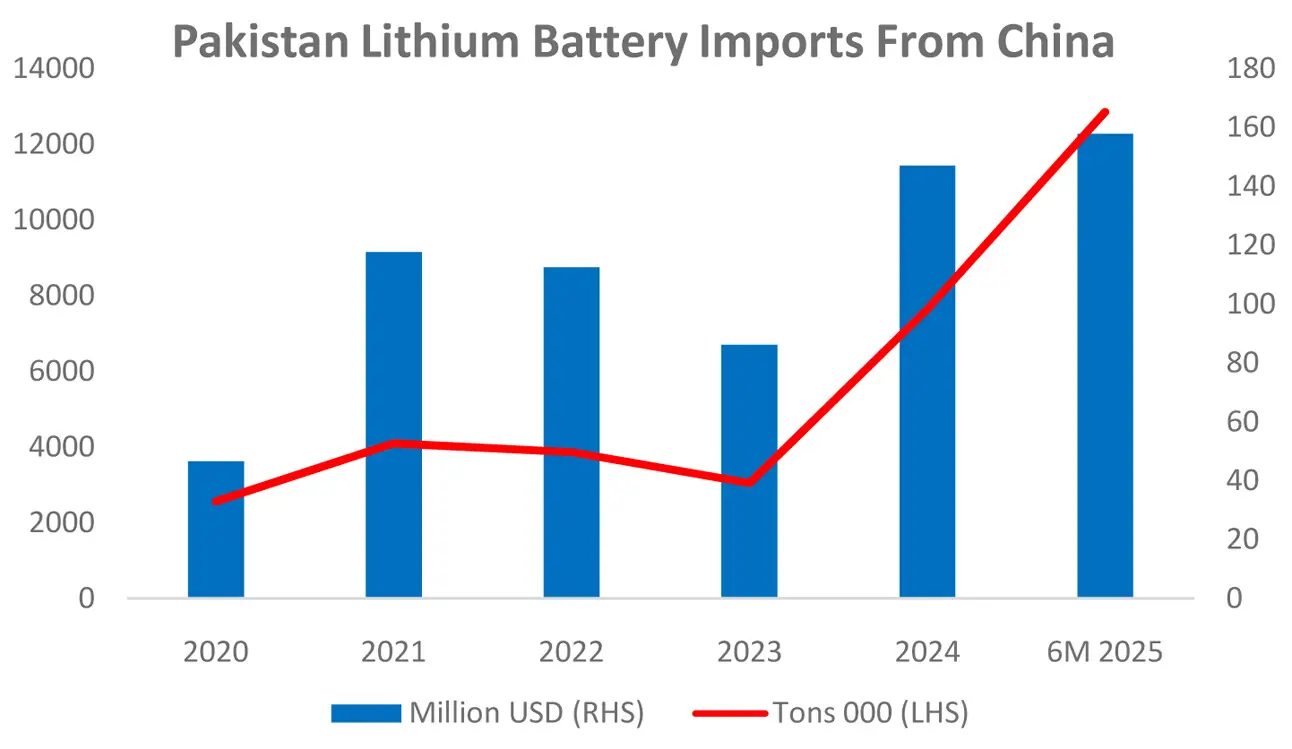

The next phase of the solar revolution is already visible: battery storage. Pakistan imported lithium-ion batteries worth $157 million in just the first six months of 2025, surpassing the entire import bill of 2024. More telling is the volume — up 68 percent year-on-year in only half the time.

As these batteries begin supplementing solar systems, even peak nighttime load may soon come under pressure, accelerating the grid’s loss of relevance.

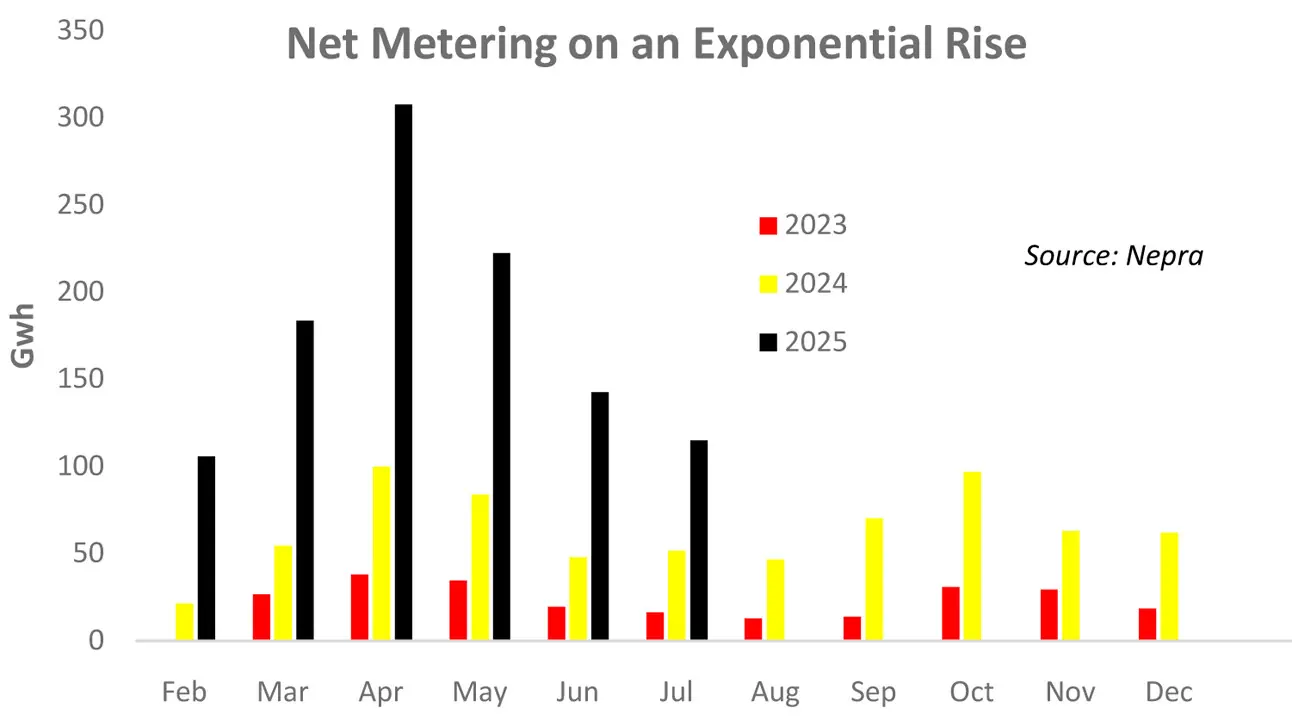

Net metering, still a relatively small cog, highlights the pace of change. Net-metered generation stood at 1.1 billion units in the first seven months of 2025 — triple last year’s level and ten times that of 2023.

From here, supply and demand planning cannot hinge on vague assumptions about solar uptake. The speed of adoption has confounded global observers; Pakistan’s planners should be the first to adapt.

Solar is here to stay, and much of the sector will revolve around it in the near future. For the grid to retain relevance, investments in reliability are now essential to keep bulk industrial users from looking elsewhere.

Comments

Comments are closed for this article.