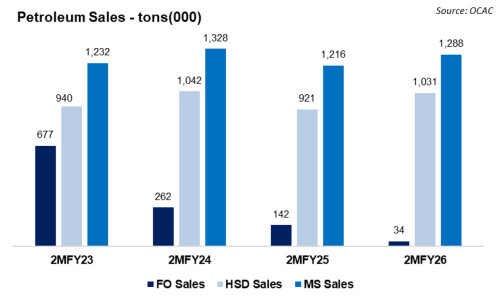

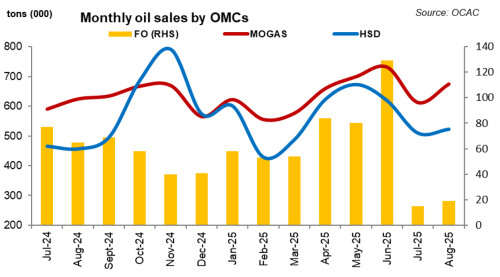

Pakistan’s oil marketing companies delivered another solid month in August 2025, with industry volumes reaching 1.300 million tons—up 7 percent year-on-year and 6 percent month-on-month—taking cumulative sales in 2MFY26 to 2.5 million tons, a 5 percent increase over the same period last year.

The product mix shows broad-based strength outside furnace oil: motor spirit rose up 8 percent year-on-year and 10 percent month-on-month, while high-speed diesel increase by 14 percent year-on-year and 3 percent month-on-month; furnace oil remained structurally weak (-71 percent YoY) but edged 21 percent higher versus July-25 as a few FO-fired units came on line. Ex-FO volumes were up 11 percent year-on-year and 6 percent month-on-month, underscoring that the recovery is being led by retail fuels.

Demand tailwinds were visible across the retail complex. A modest rollback in pump prices, reopening of schools, and a gradual pickup in mobility and economic activity supported MS and HSD, while the premium segment stayed buoyant: HOBC rose 146 percent year-on-year in Aug-25 and 170 percent year-on-year in 2MFY26, reflecting mix shift toward higher-end vehicles.

Aviation fuel (JP) posted its strongest two-month run since 2MFY18, on elevated summer travel. Other fuels like MS and HSD increased by 6 and 12 percent year-on-year, respectively in 2MFY26.

Late-month offtake, however, was tempered by heavy rainfall and flooding across Punjab and adjoining regions—an early signal that weather could briefly interrupt momentum. Furnace oil’s deep contraction is policy-driven as much as structural: the newly imposed petroleum levy has further suppressed FO economics even as Aug-25 volumes ticked up month-on-month on intermittent power-sector dispatch.

The outlook for OMC sales looks positive, though some risks remain. Analysts expect the industry to grow at a steady mid-single-digit pace in FY26, helped by stable fuel prices and a gradual pickup in economic activity.

However, ongoing floods could dampen diesel demand in farming areas. Still, August marked the twelfth straight month of sales growth, with 2MFY26 retail volumes (excluding furnace oil) showing double-digit gains—a strong start that points to a slow but steady recovery driven by consumption.

Comments

Comments are closed for this article.