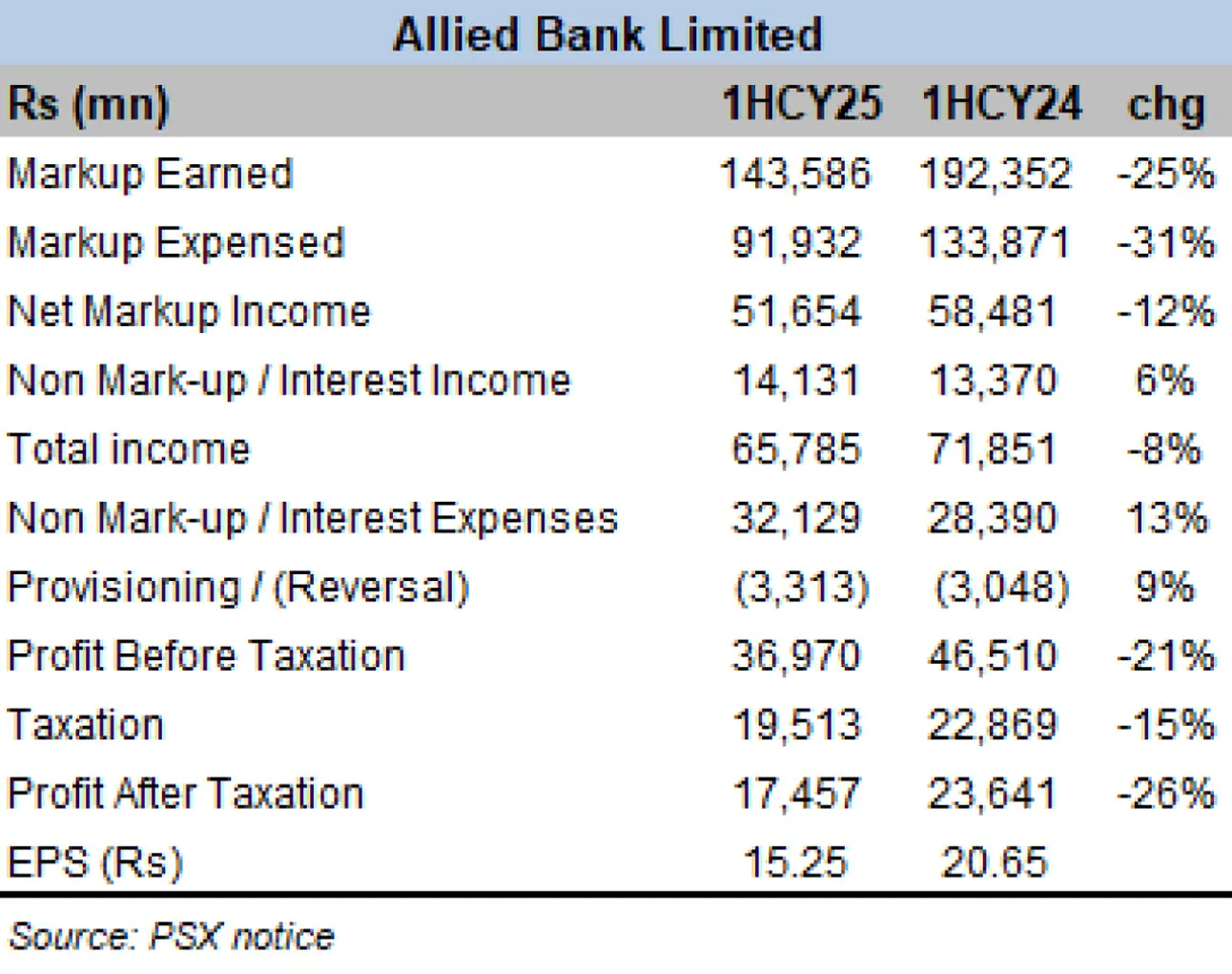

Allied Bank Limited (ABL) announced its financial results for the first half of 2025, alongside an interim cash dividend of Rs4 per share, taking the year-to-date payout to Rs8/share.

Expectedly, profits have humbled from the same period a year ago, as a significantly reduced average interest rate along with double-digit rise in non-mark-up expenses weighed down on profitability.

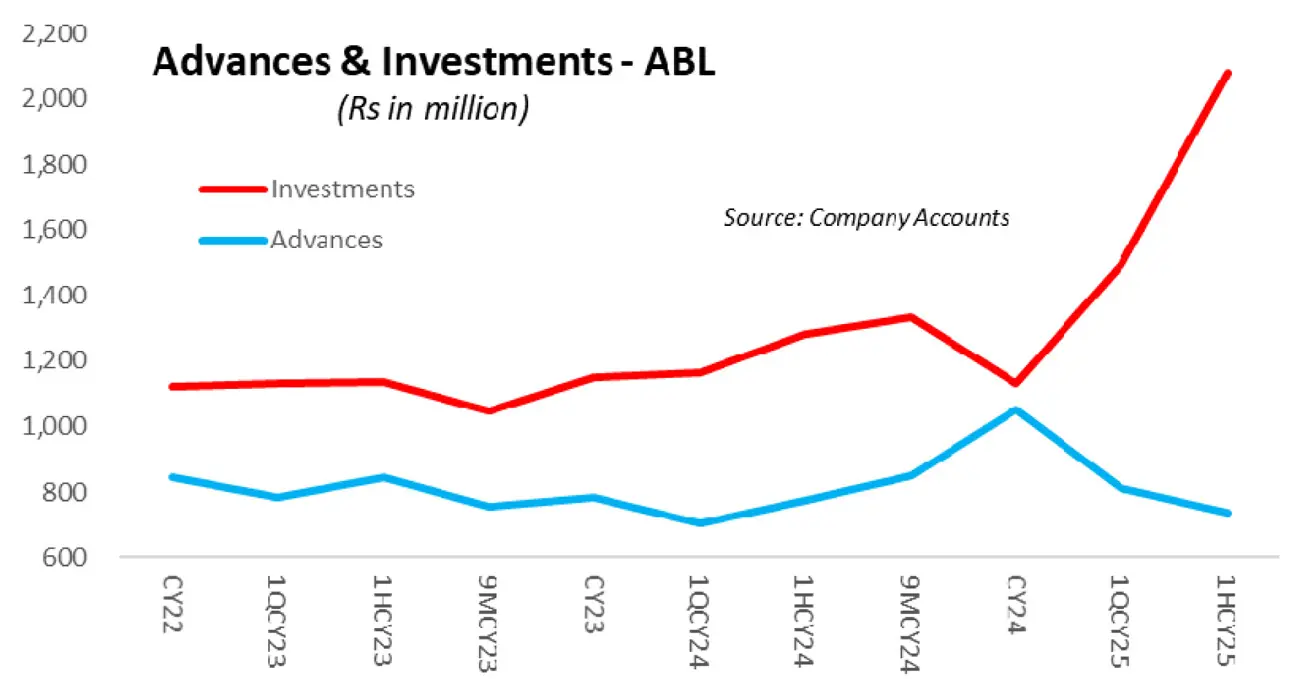

As has been the case across the industry, investments once again came to the fore of asset book expansion. The investment portfolio at ABL by the end of 1HCY25, had almost doubled over December 2024 –a staggering addition of Rs950 billion.

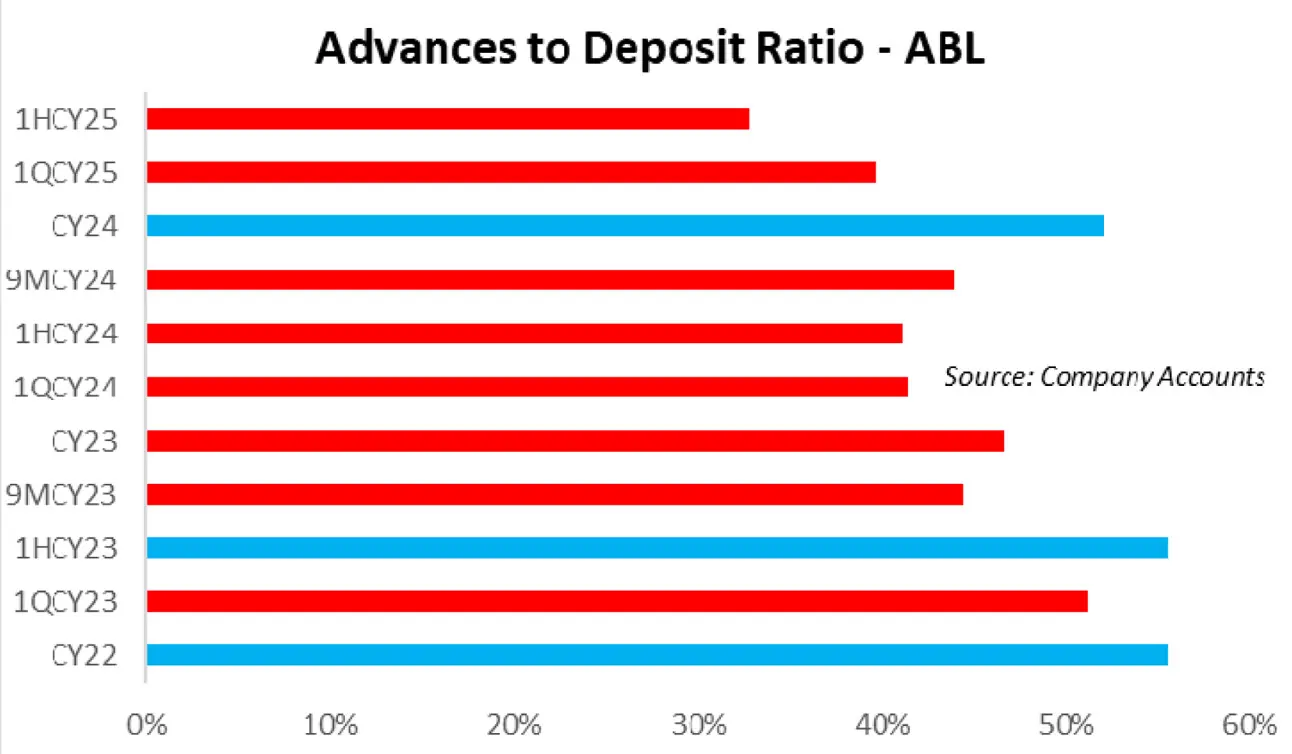

The Investment to Deposit Ratio (IDR) clocked in at 92.6 percent – levels unheard of in memory. These numbers are usually associated with coverage ratios. This is by far the steepest rise in investments over any three or six-month period.

Advances, on the other hand, shed Rs315 billion over December 2024. At Rs736 billion – ABL’s advances book appears the thinnest for any half year period in at least three years.

Recall that the advances portfolio had crossed Rs1 trillion mark at the end of CY24 – as banks rushed to meet the ADR requirement in order to avoid higher taxes. The 30 percent dip over December 2024 is significantly higher than the industry wide drop of 16 percent in the same period.

The SBP data shows loans to Non-Banking Financial Institutions (NBFI) were responsible for half of the Rs2.3 trillion sector dip in advances over December 2024 – despite just a 5 percent share in total advances.

It is no secret the NBFIs were extended loans towards the end of CY24 to window dress he balance sheets by most banks to avoid higher taxes. Allied Bank’s ADR slipped a colossal 19 percentage points from December 2024 to under 33 percent – lowest in a very long time, if not ever.

On the liabilities side, ABL’s deposits saw a healthy 11 percent increase from December 2024, reaching Rs2.2 trillion – this is still lower than the industry average growth of 16 percent.

The deposit base continues to be anchored in current accounts. Details numbers are awaited, but ABL is expected to have continued improving its CASA ratio compared to the year-ago period.

Non-markup income growth moderated, as income from foreign exchange dipped from a year ago. Fee and commission income remained strong, while capital gains more than doubled year-on-year—buoyed by favourable returns on Eurobonds and federal government securities. That said, operating costs rose sharply, with administrative expenses increasing by 13 percent year-on-year, well above the average inflation during the quarter. Consequently, the cost-to-income ratio deteriorated significantly, by more than 8 percentage points year-on-year.

With much improved macroeconomic indicators from a year ago, the return of private sector credit has not surfaces wit the same fervor as anticipated earlier.

Government borrowing appetite, on the other hand, has shown no signs of cooling off anytime soon. More of the same appears in store for at least another quarter, before the banks start rushing to lend towards the end of the year.

Comments

Comments are closed for this article.