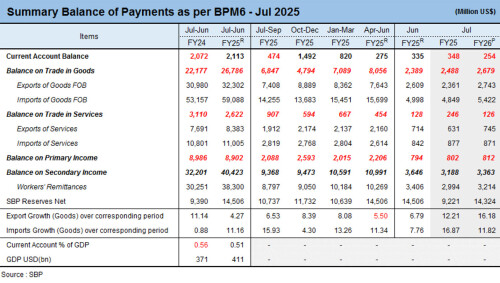

With remittances starting to dip, the current account has slipped back into deficit. The CAD stood at $254 million in July 2025 compared to a surplus of $355 million in the previous month. This $589 million swing is almost evenly split between a widening trade deficit and a decline in home remittances.

Imports are rising, up 8 percent month-on-month and 11 percent year-on-year to $5.4 billion in July 2025. It marks the fifth time in the past seven months that imports have exceeded $5 billion. The 12-month average now stands close to $5 billion—a new norm that is likely to grow as non-oil imports pick up with modest economic recovery. Detailed numbers are awaited, but current trends clearly suggest a broad increase in import demand. With oil prices easing, the import bill may stay manageable, but any commodity price rebound triggered by external shocks could pressure the external account.

Exports remain steady but insufficient to cover rising imports. Goods exports reached $2.7 billion in July, up 5 percent month-on-month and 16 percent year-on-year. However, exports are close to capacity. The rice windfall has passed, and textile exports show no immediate upside as the sector operates near full capacity.

A potential positive aspect lies in Trump’s tariffs: if Indian tariffs remain elevated at 50 percent, Pakistan could capture additional orders in home textiles. In garments and knitwear, however, Pakistan’s main competitors—Vietnam and Bangladesh—face no significant tariff disadvantages. The US is also negotiating on value-addition criteria, which could benefit Pakistan, since its import reliance for re-exports is lower than that of its competitors.

In the near term, though, exports are likely to hover around current levels. Services exports continue to perform well but remain too small to make a meaningful difference. Overall, the goods and services trade deficit widened to $2.7 billion, deteriorating 12 percent month-on-month and 8 percent year-on-year.

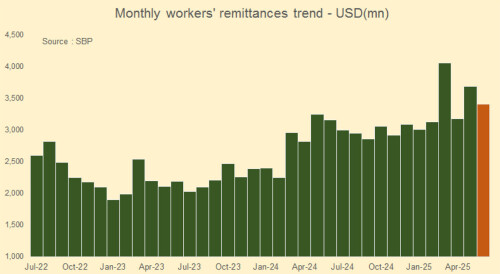

The standout performer last year was home remittances, which hit a record $38.3 billion and helped the current account swing to surplus. In July, however, inflows fell to $3.2 billion, down 6 percent from the prior month. Informal discussions with banks suggest inflows will remain subdued in August as well.

Last year’s higher inflows partly reflected extraordinary efforts by banks to attract remittances to finance their import commitments, as the SBP often restricts dollar purchases from other banks. Some larger banks incurred losses of Rs5–10 billion in the first half of CY25 and are unwilling to bear such costs again.

As a result, remittance growth is likely to remain muted, while rising imports will keep the current account in deficit, complicating the SBP’s efforts to raise forex reserves above $17 billion in FY26. The June-end target of $14 billion last year was achieved, with reserves reaching $14.5 billion, but they have since slipped slightly to $14.2 billion as the capital and financial accounts continue to show modest improvement.

Comments

Comments are closed for this article.