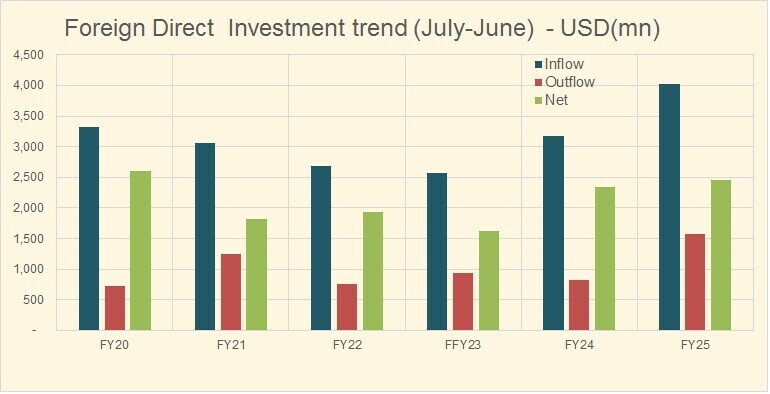

Foreign direct investment (FDI) in Pakistan edged up in FY25, reaching $2.46 billion—just a 4.67 percent increase from $2.35 billion in FY24. While this modest rise may appear encouraging, it falls short of signalling a strong investment revival.

Instead, it reflects a patchy and uneven recovery, with gains in a few sectors and countries offset by ongoing weaknesses elsewhere.

Beneath the surface, the numbers reveal a deeper story—one of selective investor interest, persistent volatility, and structural challenges that continue to weigh on Pakistan’s long-term investment appeal.

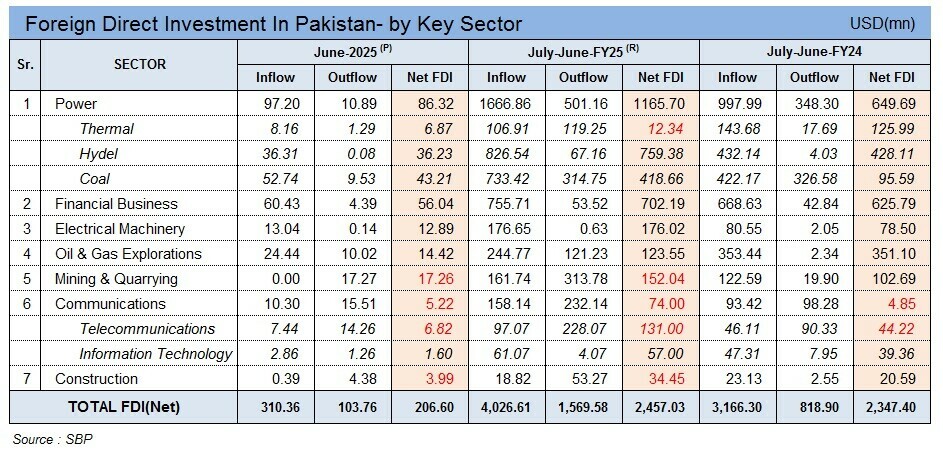

Much of the headline growth was driven by a surge in power sector investments, which more than doubled from $649 million to $1.17 billion in FY25. This was led by capital inflows into coal and hydropower projects.

The financial sector also posted growth with FDI rising from $642 million to $703 million in FY25, highlighting increased interest in Pakistan’s banking and fintech ecosystem. Similarly, investments in electrical machinery and mining suggested growing attention toward the country’s industrial and extractive potential.

Yet, this momentum was uneven. Sectors such as telecommunications experienced a net outflow of $131 million in FY25, up from $44 million the previous year.

Construction also saw a decline, signalling waning investor confidence in real estate and infrastructure development. These outflows likely reflect divestments and exit by foreign firms, underscoring the lingering risks perceived by multinational players.

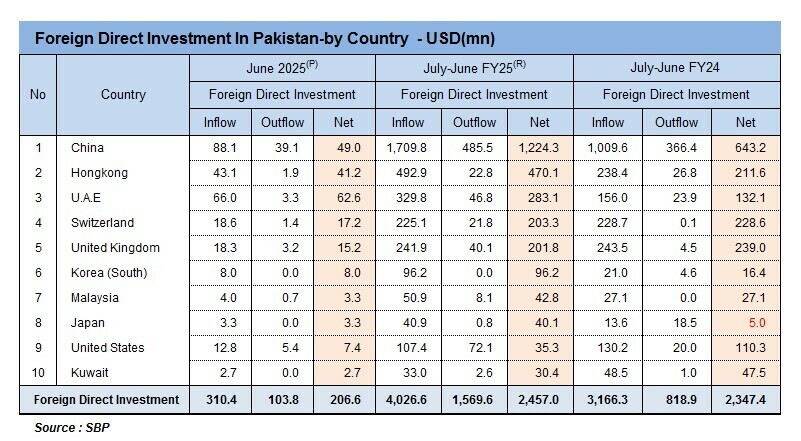

Country-wise, China emerged as the dominant investor, nearly doubling its net FDI to $1.22 billion in FY25, reaffirming its long-standing economic partnership with Pakistan. The UAE and Hong Kong also increased their investments.

In contrast, US-origin FDI plummeted from $110 million to just $30 million—highlighting alignment with regional capital but a continuing reluctance from Western investors.

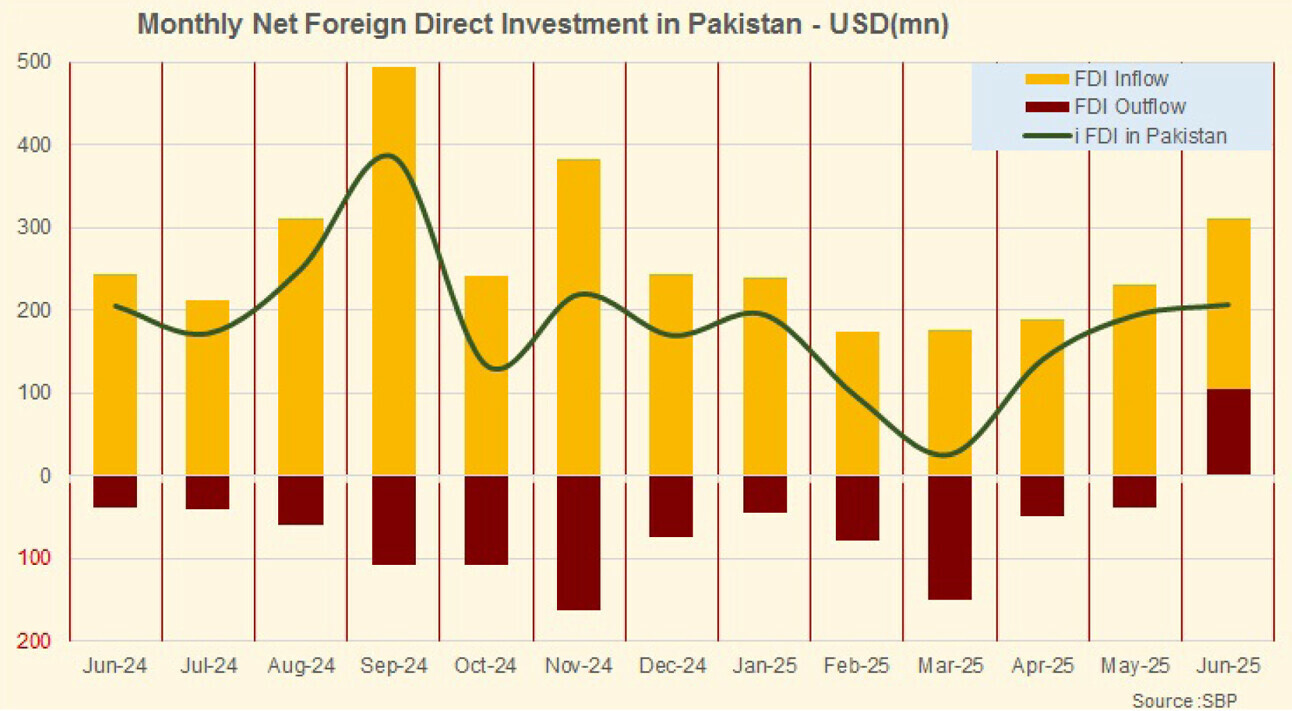

Monthly trends further highlighted volatility: FDI peaked in September and November 2024, followed by inconsistent flows for the remainder of the year. This choppiness reflects an uncertain investment climate where structural concerns undercut temporary optimism.

These structural issues are not new. Over the past five years, Pakistan has witnessed a steady decline in the presence of global giants. Oil majors like Shell and TotalEnergies have exited; tech firms such as Uber, Careem, and Microsoft have scaled back or withdrawn altogether; and pharmaceutical multinationals, including Pfizer, Sanofi, Eli Lilly, and Bayer, have divested their operations.

The reasons are familiar: unpredictable tax regimes, foreign exchange controls, difficulty repatriating profits, and an overregulated formal sector that struggles to compete with the informal economy.

Even in FY25, despite achieving a rare combination of a $2.1 billion current account surplus and a second consecutive primary fiscal surplus, investor hesitation remained. These macroeconomic wins were primarily attributed to increased remittance inflows and the State Bank’s aggressive dollar buying, which helped stabilize reserves.

But while macro indicators improved, they did little to restore trust in Pakistan’s investment climate. Structural weaknesses partly explain the cautious mood among foreign investors.

Portfolio investments stayed negative despite a booming stock market, and investor concerns about inconsistent tax policies, regulatory overreach, and a high burden on formal sector businesses persisted.

Even Sectors like information technology and exports continue to show promise, but their scale remains insufficient.

FDI in FY25, though slightly higher at $2.4 billion, still fell short of what is needed. If Pakistan wants to maintain a stable external position while promoting growth, it needs steady inflows—not just from remittances, but also from foreign investors.

Comments

Comments are closed for this article.