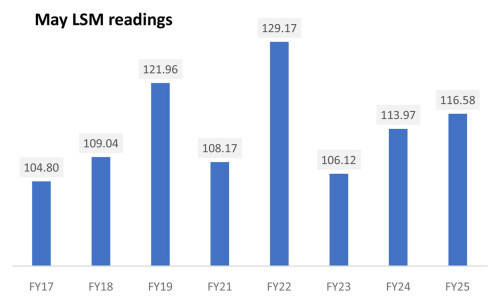

Pakistan’s large-scale manufacturing (LSM) sector continues to flirt with the idea of recovery, but the data tells a different story. May 2025 posted a modest 2.29 percent year-on-year increase — the second monthly rise this calendar year — but the bigger picture remains unflattering.

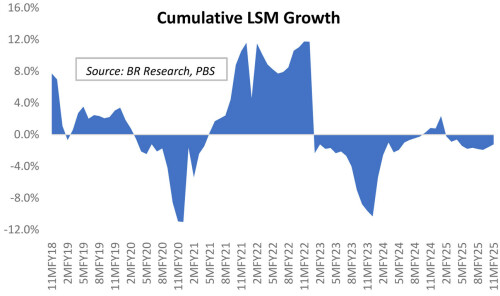

Cumulative LSM growth for 11MFY25 stands at negative 1.21 percent, marking the tenth consecutive month of contraction. That’s not a recovery; its stagnation dressed up as progress.

The rot runs deep. Half of the 22 tracked LSM sub-sectors are still clocking an index value below 100 — meaning their current output is lower than it was nine years ago when the base period began in July 2016. For an economy chasing growth, that’s a damning indictment.

In fact, the overall LSM index for May 2025, while marginally better than the past two years, is still 5.5 percentage points lower than May 2019, effectively placing industrial activity in a time warp.

Let that sink in: Pakistan’s industrial engine is idling where it was seven to eight years ago.

The diffusion index shows just enough to keep hopes alive — 12 out of 22 sectors have shown year-on-year growth during 11MFY25. But only one of them — automobiles (along with cycles and motorcycles) — managed double digits. The rest are crawling in low single digits, hardly the stuff of revival narratives.

The sugar industry has been a major drag, with output down 14 percent year-on-year, producing 5.8 million tons this season, a full 1 million tons short of last year’s mark. It’s not just sugar either. Juice production — perhaps the most literal measure of industrial vitality — is now at its lowest in 108 months, the worst since the current index base was established.

The textile sector remains stuck in a deep freeze. The LSM index for textiles has now stayed below 100 for 36 straight months — that’s three years of going nowhere. And the one sub-sector that has kept the LSM numbers from falling off a cliff — readymade garments — is starting to lose steam. While it still contributes positively on a cumulative basis, export quantities have declined year-on-year for several consecutive months, pulling overall momentum down to a modest 5 percent growth.

In fact, readymade garments may now be staring down a new test — one shaped by geopolitics. With Trump-era tariffs likely to reshape global trade dynamics again, Pakistan’s textile exporters are entering a more competitive world where cost, compliance, and scale will matter more than ever. The sector’s trajectory — long the LSM’s only bright spot — could now determine whether this entire industrial slide gets arrested or accelerates.

Meanwhile, the industrial heavyweights are still in intensive care. Cement, steel, chemicals, and white goods — sectors that traditionally signal broader economic activity — remain deeply negative. And without a rebound in construction-linked industries, any talk of broad-based LSM revival remains wishful thinking.

Yes, there are flickers of hope — electric fans, for instance, are seeing some momentum, driven by renewed government focus on energy conservation. But with a sectoral share of just 0.08 in the LSM basket, fans alone are not going to blow wind into the sails of a stalled industrial ship.

Policy optimism remains high. Lower industrial electricity tariffs and cheaper credit are being hailed as potential game-changers. But these may only slow the slide, not reverse it. The highs of FY22 are not on the horizon — they are over the hills and far away.

The LSM is not dying. But it is certainly not growing up either. It is stuck in industrial adolescence, trapped in a loop of false starts and shallow rebounds.

Until the economy confronts its structural bottlenecks — from energy unpredictability to policy inconsistency and export concentration — Pakistan’s LSM will continue to do what it does best: take one step forward and two steps back — and call it progress.

Comments

Comments are closed for this article.