It didn’t take much for car buyers to return to showrooms. As soon as the policy rate dropped to 12 percent, auto financing rebounded. Net borrowing turned positive after months of staying in the red where it stayed for exactly 26 consecutive months! During this dry spell, rates had climbed from 12.5 to a peak of 22 percent and stayed there for a full year.

The rate cut worked. FY25 closed with a 42 percent jump in auto sales compared to last year, up 44,000 units, and roughly 20,000 higher than FY23. However, volumes continue to pale in comparison to the highest sales achieved in FY22, down 47 percent from that year.

The fact is, there has been ample latent demand for cars over the past two years but buying power was curbed by inflationary pressures and high tax burden coupled with an acute lack of viable financing options given sky-high rates, as well as SBP’s tightened regulations on consumer financing.

The tougher prudential regulations meant consumers not only faced steep interest rates on car loans, but also higher equity conditions, reduced loan tenors, and a cap on financing. In addition, imported cars were no longer eligible for car financing. The prudential regulations served a singular purpose of shrinking demand in the automobile industry which in turn would keep imports subdued.

With interest rates now lower than before, demand is more visibly active. But this is far from a boom anyone should expect. For one, rates remain in double digits and relatively high. Whether they fall further, enough to trigger a real surge in auto financing, depends on several moving parts, chief among them is the direction of the economy and whether it enters a growth phase over the next six months.Auto financing reached its highest numbers in history when rates dropped to 7 percent, but the moment rates hiked up from 12.5 percent, consumers’ ability to afford financing, and banks’ own risk appetite plummeted.

Secondly, while the SBP has not shown any signs of reversing the regulatory changes, other policy issues may do no favors for latent demand either. For one, the recent hike in prices by several assemblers, that have materialized in response to theEnergy Vehicle Adoption Levy, might price some potential consumers out of the market. This is especially true for vehicles in the mid-range segments of passenger cars, and less true for the luxury segment.

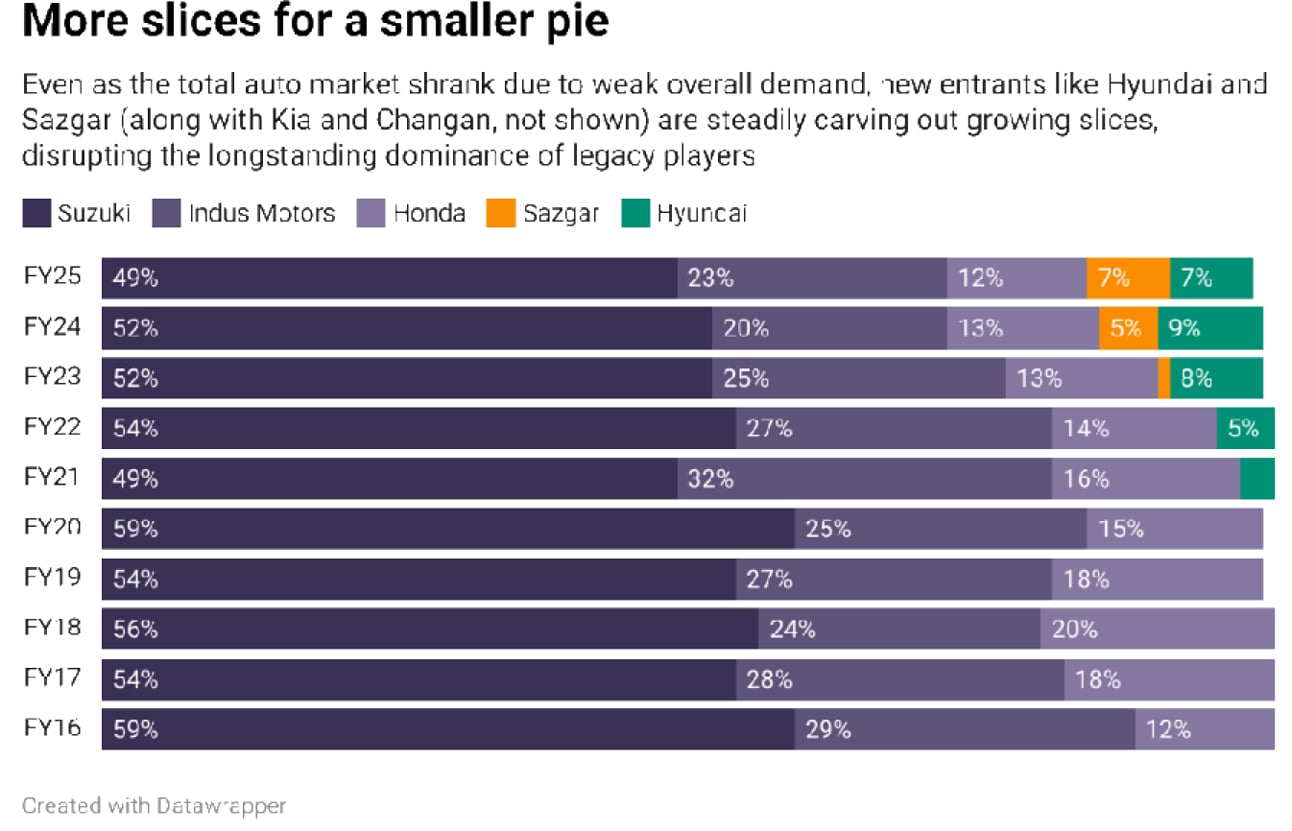

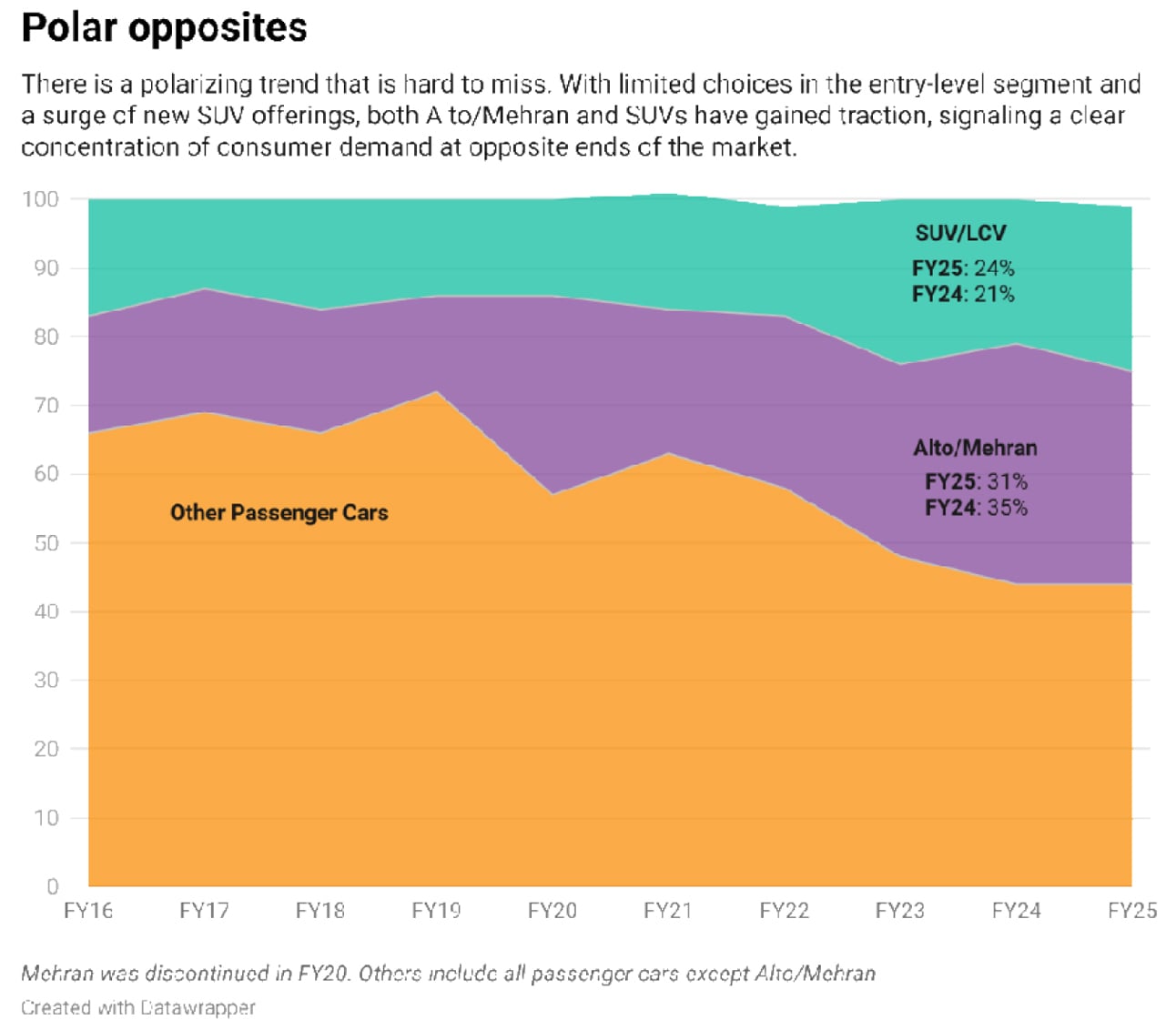

Though the levy is higher on larger engines, particularly SUVs and crossovers,demand for SUVs has been fairly robustand growing. In fact, larger macroeconomic conditions including inflation did not affect demand for this segment, that has increasingly expanded over the past 3-4 years with the entry of new players and new models. Companies like Kia, Hyundai and Sazgar have done exceptionally well in various SUV segments since FY21.

As a result, the share of SUV/LCV in total volumes has grown to 24 percent in FY25 where the last 3-year average stands at 23 percent.

On the other end of the market is the entry-level engine—the unrivalled Alto that has taken the market by a storm. Even at a steep price tag of Rs31-33 lakh, Alto remains the most affordable locally assembled vehicle in the country. In its competition are 3-year-old used imported cars from Japan that are brought in by dealers under the guise of the gift scheme.

But high tariffs and higher commissions kept by importers and dealers ensures these cars are not price competitive with the local favourite. On top of that, they are not eligible for bank financing.

There aren’t many other options. Suzuki is not taking fresh bookings for Cultus, Wagon-R or Swift and the only other assembler offering a small car is Kia with Picanto, priced a good Rs10 lakh above Alto.

One may argue that the second-hand car market is available for middle-income car buyers when small car options dwindle, but the market is extremely fragmented, unorganized and unreliable with no formal trading mechanisms available. With the exit of startups like CarFirst and Vavacars that were attempting to facilitate car trading, the secondary market remains precarious. For most, buying second hand cars is a shot in the dark.

The risk-averse car buyers that are still price sensitive therefore,are likely to opt for a short-tenor and high equity loan to cover the gap in financing and still be able to afford an Alto. For many, it remains their only real available option. As it stands, the 3-year average share of Alto in total volumes is an impressive 31 percent (41% in passenger cars alone).

If rate cuts keep coming, consumers may find it easier to absorb the higher prices for most segments. The elasticity of vehicle demand to prices and income is still a subject ofmuch debate. What’s less up for debate is the government’s move to liberalize the import policy and the potential plans to commercialize the import of used cars, both of which spells more trouble, not less, for legacy OEMs. What’s even less up for debate is that none of these conflictingpolicies place consumers at the centre of them (read: “How to make anti-poor policies 101”), which is typical, but a shame nevertheless.

Comments

Comments are closed for this article.