International Knitwear Limited (PSX: INKL) was incorporated in Pakistan as a public limited company in 1990. The principal activity of the company is manufacturing knitted and woven apparel products besides exporting garments.

Pattern of Shareholding

As of June 30, 2024, INKL has a total of 9.675 million shares outstanding which are held by 1238 shareholders. The local general public has a majority stake of 42.15 percent in the company followed by directors, CEOs, their spouses, and minor children holding around 35.37 percent shares. Associated companies, undertakings & related parties hold 9.67 percent shares of INKL. Around 2.16 percent of shares of the company are held by Modarabas & Mutual Funds and 1.64 percent by insurance companies. The remaining shares are held by other categories of shareholders.

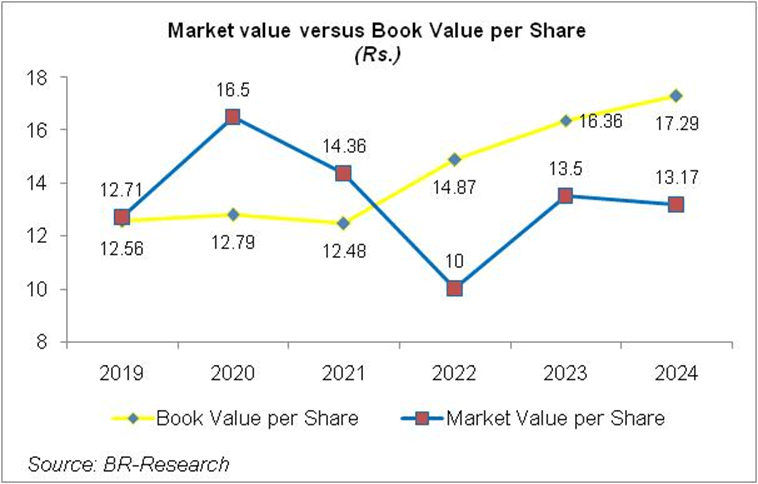

Financial Performance (2019-24)

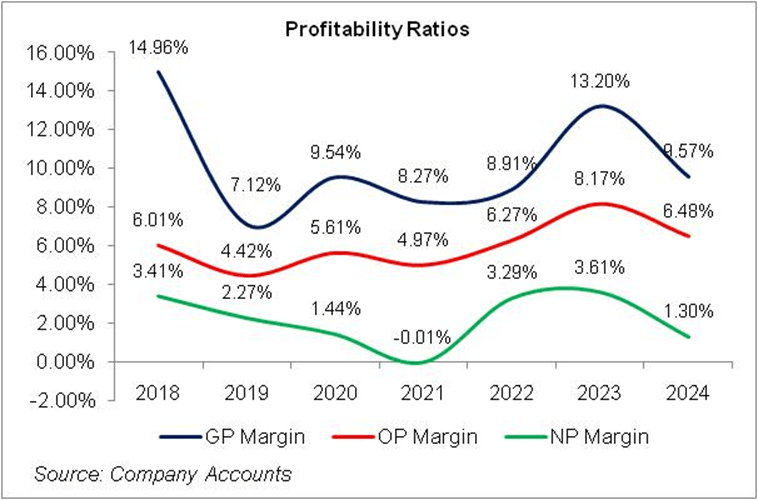

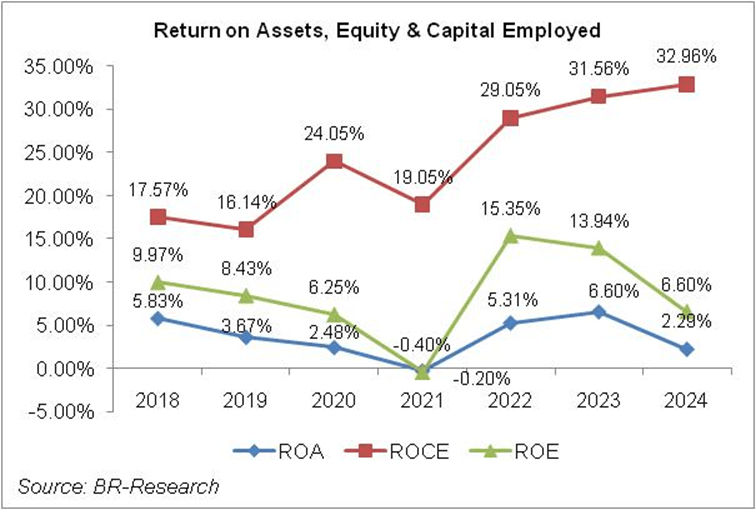

Except for a plunge in 2021 and 2023, INKL’s topline rode an upward trajectory over the period under consideration. Conversely, its bottom line shrank until 2021 when the company recorded net loss. INKL’s bottom line recovered from a net loss in 2022 and remained constant in 2023. This was followed by a drastic fall in the company’s bottom line in 2024 despite tremendous topline growth. The company’s margins considerably eroded in 2019. In 2020, gross and operating margins rebounded while net margins continued to slide down. All the margins depicted a fall in 2021 followed by recovery in the subsequent two years. In 2024, INKL’s margins eroded (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

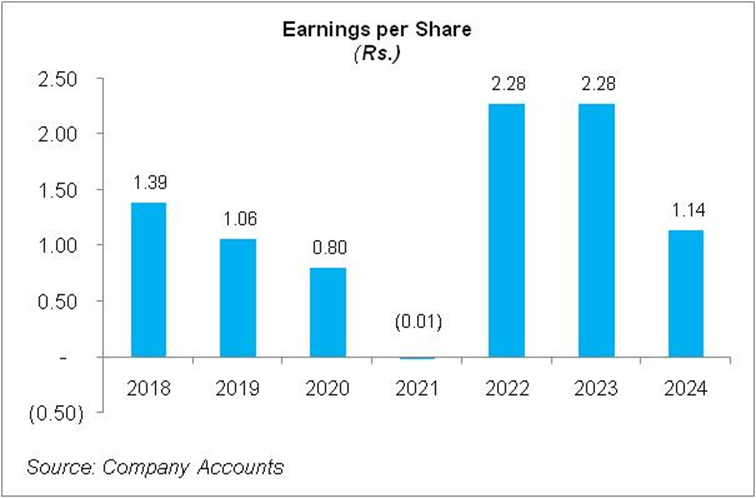

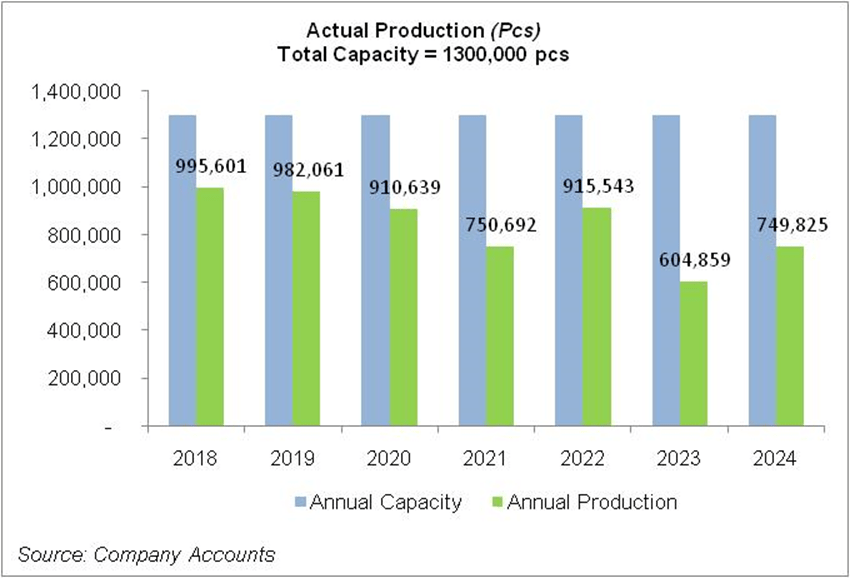

In 2019, INKL’s topline grew by 14.72 percent year-on-year to clock in at Rs. 451.10 million. This was on the back of an increase in volume, prices, and depreciation of the Pak Rupee. The company achieved capacity utilization of 75.54 percent in 2019 as both local and export orders increased. Cost of sales grew on the back of inflation, hikes in commodity prices, elevated fuel and energy prices as well as Pak Rupee depreciation. This resulted in a 45.41 percent decline in gross profit with GP margin falling 14.96 percent in 2018 to 7.12 percent in 2019. Operating expenses surged by 28 percent year-on-year in 2019 on account of higher payroll expenses, conveyance charges as well as depreciation. The company hired additional resources which took its workforce from 127 employees in 2018 to 191 employees in 2019. INKL recorded other income of Rs.11.13 million in 2019 due to exchange gain; gain on translation of foreign currency debtors as well as hefty dividend income earned during the year. Other expenses slid by 14.94 percent in 2019 due to lower profit-related provisioning made during the year. Operating profit plummeted by 15.63 percent in 2019 with OP margin slipping from 6 percent in 2018 to 4.42 percent in 2019. INKL was able to cut down its finance cost by 17.54 percent in 2019 despite a higher discount rate. Net profit declined by 23.63 percent year-on-year in 2019 to clock in at Rs.10.24 million with EPS of Rs.1.06 versus EPS of Rs.1.39 recorded in the previous year. NP margin slumped from 3.41 percent in 2018 to 2.27 percent in 2019.

In 2020, INKL registered a 19.14 percent year-on-year rise in its net sales which stood at Rs.537.46 million. This was due to robust performance in the first three quarters of 2020 before the outbreak of COVID-19. However, the lockdown imposed during the 4th quarter of the year resulted in idle capacities, supply chain impediments, and cancellation of orders across the industry. As a result, INKL achieved capacity utilization of 70.05 percent in 2020. Due to improved volume and prices during the most part of the year, as well as cost control measures put in place by the management, INKL registered a 59.74 percent year-on-year rise in its gross profit with GP margin picking up to 9.54 percent in 2020. Operating expenses fell by 1.46 percent in 2020 as the workforce was streamlined to 152 employees which resulted in lower payroll expenses. Due to restrictions on traveling, conveyance charges also dropped during the year. Other income declined by 80.41 percent in 2020 due to no exchange gain and gain on translation of foreign currency debtors recorded during the year. Dividend income also ticked down in 2020. Conversely, other expenses mounted by 14.36 percent in 2020 due to higher profit-related provisioning made during the year. The company was able to strengthen its operating profit by 51.29 percent over last year with OP margin scaling up to 5.61 percent in 2020. Finance costs magnified by 156.24 percent in 2020 due to a higher discount rate for the most part of the year, elevated exchange loss as well as increased borrowings. This coupled with a higher effective tax rate due to prior year taxation drove INKL’s net profit down by 24.45 percent in 2020 to clock in at Rs.7.73 million with EPS of Rs.0.8 and NP margin of 1.4 percent.

INKL recorded a 9.2 percent year-on-year plunge in its net sales which clocked in at Rs.488.09 million in 2021. The slowdown of the global economy due to COVID-19 as well as the imposition of lockdowns time and again during the year dented its sales volume. The company’s capacity utilization fell to 57.75 percent in 2021. A hike in global cotton and yarn prices as well as a revision of gas tariff and non-availability of gas during winter months drove up INKL’s cost of sales. This resulted in a 21.30 percent year-on-year fall in gross profit with GP margin sinking to 8.27 percent. Operating expenses inched up by 3.44 percent in 2021 due to slightly increased salaries although workforce size remained almost intact during the year. Other income surged by 181.24 percent in 2021 on account of higher dividend income, grant income, and gain on the sale of investments. INKL also recorded an exchange gain of Rs.0.488 million during the year. Other expenses tumbled by 68.76 percent in 2021 due to lower profit-related provisioning done in 2021. Operating profit contracted by 19.53 percent in 2021 with OP margin dropping to 4.97 percent. Finance cost increased by 32.72 percent in 2021 despite monetary easing due to higher mark-up on MTF salaries & wages (COVID-19) and other mark-up incurred during the year. INKL recorded a net loss of Rs.0.05 million in 2021 with a loss per share of Rs.0.01.

INKL posted a staggering 37.32 percent year-on-year escalation in its net sales which clocked in at Rs.670.26 million in 2022. This was on the back of a revival in both local and export orders coupled with improved prices and Pak Rupee depreciation which made export sales more worthwhile. Due to increased demand, the company was able to employ its capacity efficiently with capacity utilization clocking in at 70.43 percent in 2022. Gross profit spiraled by 48 percent in 2022 due to better absorption of fixed overheads, upward price revision, elevated volumes, and currency depreciation. 11.18 percent increase in operating expenses in 2022 was primarily the effect of higher payroll expenses as the number of employees increased to 181 in 2022. Other income multiplied by 56.83 percent in 2022 due to higher exchange gain, dividend income, gain on disposal of property, plant, and equipment as well as reversal of provision on ECL. Higher profit-related provisioning drove up other expenses by 423.47 percent in 2022. Operating profit strengthened by 73 percent year-on-year in 2022 with OP margin climbing up to 6.27 percent. Finance cost dropped by 18.38 percent in 2022 due to lower other markup and markup incurred on export refinance facilities. INKL was able to pull its bottom line out of a net loss and recorded a net profit of Rs.22.08 million in 2022. This translated into EPS of Rs.2.28 and NP margin of 3.29 percent.

The political and economic instability prevailing in the country, and the high cost of doing business coupled with global recession took its toll on the net sales of the company which dwindled by 8.77 percent to clock in at Rs.611.49 million in 2023. INKL’s capacity utilization drastically dropped to 46.53 percent in 2023 in line with reduced demand. Nevertheless, gross profit spiraled by 35 percent year-on-year in 2023 with GP margin flying up to 13.2 percent. This was due to higher margins on exports, cost control measures, and the company’s ability to pass on the impact of high costs to its consumers. High cost was the result of sky-rocketed inflation, a shift to expensive imported cotton due to damage of local cotton produce owing to devastating floods, Pak Rupee depreciation as well as upward revision in gas and power tariffs. 36 percent high operating expense incurred in 2023 was the consequence of higher payroll expense although the number of employees was streamlined to 121 in 2023. Higher fee and subscription charges, depreciation as well as motor vehicle & conveyance charges also played their role in inflating the operating expense in 2023. Other income thinned down by 27.9 percent in 2023 mainly on account of exchange loss and loss and loss on disposal of investment. Higher provisioning for WWF and WPPF drove other expenses up by 34.49 percent in 2023. INKL was able to record an 18.96 percent enhancement in its operating profit with OP margin reaching its optimum level of 8.19 percent in 2023. Finance charges continued to slide during the year due to significantly lower outstanding loans in 2023. Higher taxation due to the effect of the prior year pushed down net profit by 0.06 percent in 2023 to clock in at Rs.22.072 million in 2023. However, EPS remained intact at Rs.2.28 in 2023. NP margin boasted its highest level of 3.61 percent in 2023.

In 2024, INKL’s topline dipped by 39 percent to clock in at Rs.850.51 million. This came on the back of the well-timed execution of BMR initiatives and the company’s ability to grab export opportunities besides focusing on local niche markets. The company achieved capacity utilization of 57.68 percent in 2024 and produced 749,825 pieces. The high cost of raw materials as well as elevated energy tariffs resulted in a 44.90 percent hike in the cost of sales in 2024. This resulted in a 0.86 percent uptick in gross profit with the GP margin falling down to 9.57 percent in 2024. Operating expenses ticked up by 2.72 percent in 2024 mainly on account of higher payroll expense due to inflationary pressure and an increase in the number of employees. INKL’s factory workforce stood at 168 employees in 2024. Other income slid by 28.69 percent in 2024 due to lower gains recorded on the disposal of property, plant & equipment. Other expenses also dropped by 27.79 percent in 2024 due to lower profit-related provisioning done during the year. Operating profit ticked up by 10.37 percent in 2024, however, OP margin plunged to 6.48 percent. Finance charges escalated by 121 percent in 2024 due to higher discount rates and increased utilization of short-term working capital lines. INKL’s bottom line eroded by 49.97 percent to clock in at Rs.11.043 million with EPS of Rs.1.14 and NP margin of 1.30 percent.

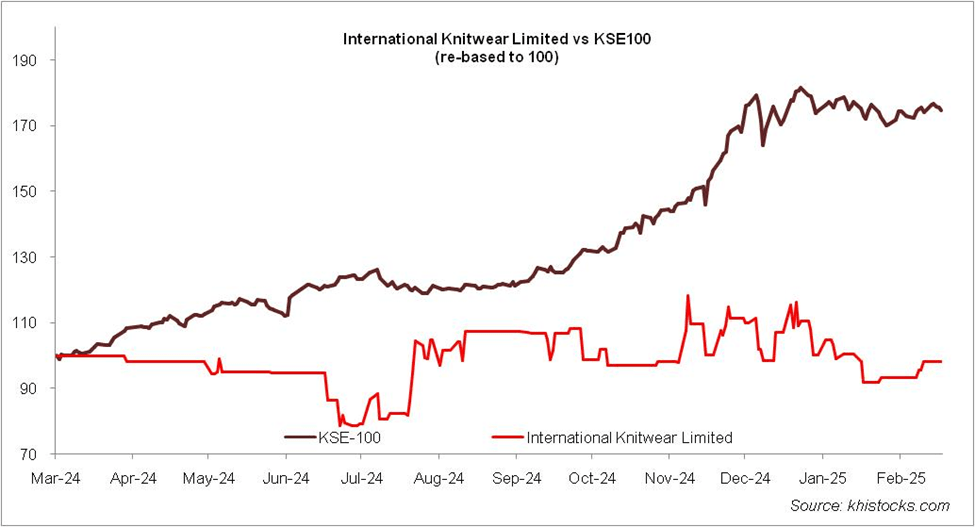

Recent Performance (1HFY25)

During the first half of the ongoing fiscal year, INKL’s topline jumped up by 41.28 percent to clock in at Rs.572.38 million. This came on the back of increased volume and higher product prices in both local and export markets. In anticipation of higher demand, the company also enhanced its capacity in the value-added segment. 58.29 percent escalation in cost of sales during 1HFY25 was the result of elevated energy tariffs and higher prices of raw materials. This resulted in a 43.36 percent diminution recorded in INKL’s gross profit with the GP margin drastically falling down from 16.73 percent in 1HFY23 to 6.71 percent in 1HFY25. One of the company’s export clients demanded delivery via air which resulted in a spike in freight charges during the period. Overall operating expenses recorded an 8.22 percent rise in 1HFY25. Considerably lesser exchange loss recorded during the period resulted in other income of Rs.4.26 million in 1HFY25. This mainly comprised of dividend income. Other expenses slumped by 60.25 percent in 1HFY25 due to lower profit-related provisioning done during the period. INKL recorded 40.33 percent thinner operating profit in 1HFY25 with OP margin clocking in at 5.16 percent versus OP margin of 12.21 percent recorded during the same period last year. Finance costs tumbled by 14.58 percent in 1HFY25 due to a lower discount rate and a considerable settlement of outstanding liabilities during the period. INKL’s net profit tapered off by 53.59 percent to clock in at Rs.10.92 million in 1HFY25. This translated into EPS of Rs.1.13 in 1HFY25 versus EPS of Rs.2.43 recorded during the same period last year. NP margin also dipped from 5.81 percent in 1HFY24 to 1.91 percent in 1HFY25.

Future Outlook

While INKL has been able to strengthen in sales in both local and export markets by grabbing the upcoming opportunities, focusing on niche markets, and enhancing its capacity by deploying timely BMR initiatives, it is unable to improve its margins and profitability owing to the high cost of sales. The main culprit that erodes INKL’s profitability is the high energy tariff. The company has recently launched a 100 KW solar power project with another 150 KW solar power project in the pipeline. This will lessen INKL’s reliance on the national grid and keep a check on its cost of sales. Besides, improved liquidity and a declining discount rate will also squeeze the company’s finance cost and result in better profitability and margins in the coming quarters of FY25.

Comments

Comments are closed for this article.