International Steels Limited (PSX: ISL) was incorporated in Pakistan as a public unlisted company in 2007. The company is a subsidiary of International Industries Limited. ISL is engaged in the manufacturing of cold-rolled, galvanized, and color-coated steel coils and sheets.

Pattern of Shareholding

As of June 30, 2024, ISL has a total of 435 million shares outstanding which are held by 5623 shareholders. International Industries Limited has the majority stake of 56.33 percent in the company followed by the local general public holding 10.89 percent shares. Sumitomo Corporation, an associated company of ISL holds 9.075 percent shares of ISL. Strategic investor accounts for 4.74 percent of the company’s shares while insurance companies hold 4.2 percent of shares. Directors, their spouses, and minor children hold 3.578 percent of ISL’s shares. Around 3.18 percent of shares of ISL are held by the public and other companies and 2.086 percent by NIT, NBP & funds. 1.88 percent of shares of ISL are held by Banks, DFIs, and NBFIs, and 1.449 percent by mutual funds. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-23)

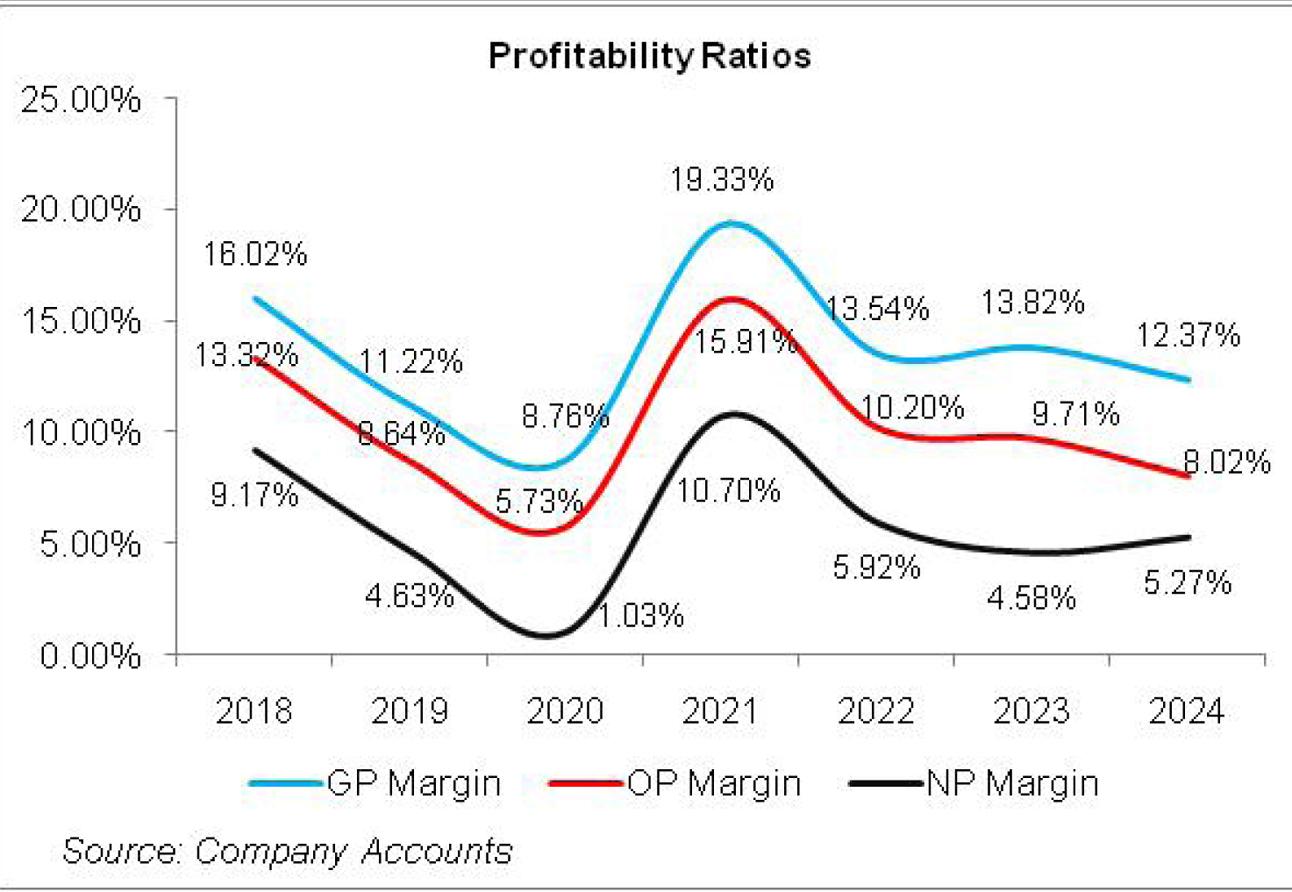

During the period under consideration, ISL’s topline slid thrice i.e. in 2020, 2023, and 2024. Conversely, its bottom line followed a downward trajectory in all the years under consideration except 2021 and 2024. The company’s margins rode a steep downhill journey until 2020 followed by a sound recovery in 2021 where the margins attained their optimum level. ISL’s margins drastically fell in 2022. In the subsequent year, gross margins slightly ticked up while operating and net margins continued to erode. In 2024, gross and operating margins tapered while net margins picked up. The detailed performance review of each of the years under consideration is given below.

In 2019, ISL’s topline grew by 20.71 percent year-on-year. During the year, the company increased its production capacity by 24 percent year-on-year to 584,400 tons. Due to the slowdown of economic activity and import of low-priced steel from Russia and China, ISL’s galvanized sales volume dipped by 11 percent to clock in at 307,500 MT while sales volume of cold rolled products increased by 11.8 percent to clock in at 217,500 MT. Gross profit tumbled by 15.49 percent in 2019 on account of the Pak Rupee depreciation and fluctuation in international steel prices. GP margin fell from 16 percent in 2018 to 11.22 percent in 2019. Distribution expenses mounted by 61.6 percent year-on-year in 2019 on account of exorbitant freight & forwarding charges due to hike in petroleum prices. Sales and promotion expenses also multiplied during the year to drive up the overall distribution expenses. While ISL greatly reduced its payroll expenses during the year, escalated legal and professional expenses resulted in only a 0.3 percent dip in administrative charges in 2019. 19.32 percent year-on-year slump in other expenses in 2019 was the effect of lower profit-related provisioning done for the year. Other income also slid by 57.4 percent in 2019 due to lower income from power generation as well as loss on the sale of property, plant & equipment. As a consequence, operating profit declined by 21.66 percent year-on-year in 2019 with OP margin moving down from 13.32 percent in 2018 to 8.64 percent in 2019. 139.15 percent year-on-year spike in finance cost in 2019 was the impact of high discount rate and increased short-term borrowings due to higher working capital requirements. Net profit tumbled by 38.96 percent year-on-year in 2019 to clock in at Rs.2664.37 million with EPS of Rs.6.12 versus EPS of Rs.10.03 recorded in 2018. NP margin also marched down from 9.17 percent in 2018 to 4.63 percent in 2019.

ISL’s net sales registered a year-on-year decline of 16.36 percent in 2020. The first half of the year was plagued by high inflation, reduced consumer spending, development spending cuts, and heightened discount rates, while the second half of the year was marred by COVID-19-related restrictions which resulted in an overall economic slowdown. Since, the beginning of the year, the company was targeting new geographical destinations to counterbalance the subdued demand in the home market. As a result, its export sales multiplied by 1.3 times in 2020. However, robust export sales couldn’t drive up the overall sales of ISL. During the year, the company’s production volume declined by 26 percent year-on-year to clock in at 412,000 tons. The sales volume of its galvanized products decreased by 23 percent year-on-year to clock in at 237,500 MT while the sales volume of cold rolled products dropped by 17 percent to clock in at 180,500 MT. Gross profit shrank by 34.67 percent year-on-year in 2020 with GP margin slipping to 8.76 percent. This was on account of depreciation in the Pak Rupee and wavering global steel prices. Distribution expenses magnified by 27.43 percent in 2020 due to high freight & forwarding charges incurred by ISL. The company streamlined its workforce from 724 employees in 2019 to 692 employees in 2020, resulting in lower payroll expenses. This coupled with reduced legal & professional charges pushed down administrative expenses by 7.6 percent in 2020. Lower profit-related provisioning pushed down other expenses by 37.38 percent in 2020 while lower income from non-financial assets resulted in a 9.9 percent slump in other income in 2020. As a result, operating profit dropped by 44.51 percent in 2020 with OP margin lessening to 5.7 percent – the lowest during the period under consideration. Finance costs hiked by 79.5 percent in 2020 due to higher discount rates for the most part of the year as well as increased working capital-related borrowings. This translated into an 81.43 percent year-on-year decline in net profit which clocked in at Rs.494.85 million in 2020 with EPS of Rs.1.14 and NP margin of 1 percent.

2021 brought about a 45.16 percent expansion in ISL’s net sales which was on account of sound recovery in all the sectors of the economy as the signs of COVID-19 began to subside. The automobile industry rebounded by 23.4 percent in 2021 providing great impetus to the steel industry. Overall, LSM registered a 14.9 percent rise in 2021 compared to a 10.2 percent decline in the previous year. ISL’s overall production increased by 19.42 percent year-on-year in 2021 to clock in at 492,000 MT. The company’s galvanized sales increased by 23 percent in 2021 to clock in at 293,000 MT while cold rolled sales went up by 10 percent to clock in at 199,000 MT. Local sales were mainly propelled by automobile, construction, appliances, and general fabrication sectors. The company was also able to grow its export sales by 11 percent in 2021 by setting its footprint in new markets. Vigorous volumes coupled with upward revision in prices resulted in 220.25 percent growth in ISL’s gross profit in 2021 with GP margin reaching its optimum level of 19.3 percent. 18.86 percent higher distribution expenses incurred by ISL in 2021 was the effect of increased freight & forwarding, sales promotion, rent, rates & taxes as well as salaries. Administrative expenses posted a 37.56 percent spike in 2021 on account of higher payroll as well as legal & professional charges incurred during the year. Increased profit-related provisioning, donations, and impairment loss on property, plant & equipment culminated in 281.9 percent taller other expenses incurred by ISL in 2021. Other income also magnified by 789.1 percent in 2021 primarily on the back of gain on re-measurement of GIDC. Income from bank deposits, government grants, and gains on the sale of fixed assets also contributed to driving up other income in 2021. All these factors translated into 302.85 percent bigger operating profit posted by ISL in 2021 with OP margin reaching its highest value of 15.91 percent. Lower discount rate as well as reduced borrowing due to the better liquidity position of the company resulted in a 64.2 percent plunge in finance cost in 2021. ISL posted a 1408.8 percent rise in its net profit which clocked in at Rs.7466.33 million in 2021 with EPS of Rs.17.16 and NP margin of 10.7 percent.

In 2022, ISL witnessed 31 percent year-on-year growth in its net sales. Production volume, however, tells a different tale as it slid by 16.5 percent year-on-year in 2022 to clock in at 411,000 MT. Sales volume was also in line with reduced demand and production. Galvanized sales dropped by 18.088 percent in 2022 to clock in at 240,000 MT while cold rolled products sales dropped by 7.54 percent to clock in at 184,000 MT in 2022. The commodity super cycle in the international market coupled with Pak Rupee depreciation, high inflation, and lackluster demand didn’t allow ISL to pass on the high cost of sales to its consumers. This resulted in an 8.23 percent year-on-year decline in gross profit in 2022 with GP margin marching down to 13.54 percent. 47 percent hike in distribution expenses in 2022 was the outcome of exorbitant freight & forwarding charges due to a spike in the prices of POL products. ISL enlarged its workforce from 693 employees in 2021 to 705 employees in 2022. This drove up the payroll expenses, however, lower legal & professional charges resulted in 6 percent lower administrative expenses in 2022. ISL incurred a hefty exchange loss of Rs. 617.018 million in 2022. This was, to a great extent, offset by lower profit-related provisioning, fewer donations, and no impairment loss incurred during the year, resulting in a 6.2 percent escalation in other expenses in 2022. Other income also eroded by 36.37 percent in 2022 due to loss from power generation and lesser gain on the re-measurement of GIDC. This resulted in 16.1 percent thinner operating profit recorded by ISL in 2022 with OP margin moving down to 10.2 percent. Finance costs magnified by 62.89 percent in 2022 on account of monetary tightening as well as enormous working capital-related borrowings. ISL’s bottom line diminished by 27.51 percent year-on-year in 2022 to clock in at Rs.5412.19 million with EPS of Rs.12.44 and NP margin of 5.92 percent.

In 2023, ISL witnessed a 16 percent year-on-year plunge in its topline. Besides economic slowdown, high inflation, floods, depreciation of Pak Rupee as well as import restrictions, the sales of ISL were greatly impacted by tax exemptions provided to the companies in the FATA/PATA region. Sales volume plummeted by 27.36 percent to clock in at 308,000 MT. In line with sluggish economic activity and the resultant low demand, production also shrank by 26 percent to clock in at 304,000 MT. The company’s ability to reduce its energy cost through strategic planning as well as higher margins on export sales due to the Pak Rupee depreciation translated into a slight uptick in GP margin which clocked in at 13.82 percent in 2023. This was despite a 14.33 percent smaller gross profit recognized by ISL in 2023. Distribution expenses tumbled by 36.2 percent in 2023 on account of lower freight & forwarding and a lesser sales & promotion budget for the year. Despite the rationalization of the workforce from 705 employees in 2022 to 688 employees in 2023, an adjustment in minimum wages as well as higher legal & professional charges translated into 14.5 percent higher administrative expenses incurred by ISL in 2023. Hefty exchange loss resulted in a 41.71 percent spike in other expenses in 2023. Other income, on the other hand, shrank by 22.48 percent in 2023 due to greater loss from power generation, reduced government grant & re-measurement gain on GIDC as well as lesser gain on sale of fixed assets. Operating profit nosedived by 20 percent year-on-year in 2022 with OP margin contracting to 9.71 percent. Finance cost posted a 71.19 percent spike in 2023 on account of monetary tightening. This pushed net profit down by 34.98 percent in 2023 to clock in at Rs.3518.79 million with EPS of Rs.8.09 and NP margin of 4.6 percent.

In 2024, ISL’s net sales dipped by 9.71 percent year-on-year. This was on account of reduced demand due to macroeconomic and political instability prevailing in the home market. Moreover, the tax exemptions given to the FATA/PATA region was further extended until June 2025. During the year, local sales proceeds slid by 18.15 percent while export sales proceeds registered a 33.87 percent improvement due to 42 percent higher export sales volume. In terms of product lines, galvanized products contributed the most to ISL’s sales mix followed by cold-rolled products and by-products. In 2024, the revenue from galvanized products improved while the other two categories registered a decline in their revenues. Cost of sales dipped by 8.19 percent in 2024 resulting in a 19.18 percent slump in gross profit in 2024. GP margin also fell to 12.37 percent in 2024. To counter the exorbitant spike in energy cost, ISL has announced the installation of a 6.4 MW solar plant, which after commissioning will significantly reduce the cost of sales. Distribution expenses multiplied by 109.63 percent in 2024 due to higher freight & forwarding charges incurred during the year on the back of improved export sales. Administrative expenses mounted by 21.51 percent in 2024 due to higher payroll expenses as well as an escalation in vehicle, traveling, and conveyance charges. ISL streamlined its workforce from 688 employees in 2023 to 682 employees in 2024. Other expenses thinned down by 69.35 percent in 2024 on account of a considerable decline in exchange loss. Other income dipped by 14.39 percent in 2024 due to higher losses incurred from power generation. ISL recorded a 25.5 percent dip in its operating profit in 2024 with OP margin sliding down to 8 percent. Finance costs shrank by 62.19 percent in 2024 due to lower outstanding long-term borrowings. Moreover, the company obtained external borrowings under the Temporary Economic Refinance Facility and Renewable Energy financing facility at below-market rates. Net profit ticked up by 3.87 percent in 2024 to clock in at Rs.3654.81 million with EPS of Rs.8.4 and NP margin of 5.27 percent.

Recent Performance (1HFY25)

During the first half of FY25, ISL registered a 19.97 percent year-on-year decline in its net sales. While local macroeconomic indicators began to improve during the period, a sustained period of high inflation has considerably squeezed the purchasing power of consumers which will take time to recover. Moreover, due to the slowdown of the Chinese economy, there was a significant decline in steel demand in the international market. This led to falling prices of steel from USD 640 per MT to USD 500 per MT which gave the most benefit to the tax-exempted players of the FATA/PATA region while the legitimate players recorded inventory losses. ISL’s export sales were also affected during the period due to increased production levels worldwide as the global demand was inadequate. Besides, the appreciation in the value of local currency also rendered the company uncompetitive by compressing its margins. Cost of sales dropped by 14.53 percent in 1HFY25 resulting in 55.21 percent shrinkage recorded in ISL’s gross profit in 1HFY25. This was the result of heightened energy tariffs. GP margin clocked in at 7.48 percent in 1HFY25 versus GP margin of 13.37 percent recorded in 1HFY24. Distribution expenses dipped by 12.57 percent in 1HFY25 due to lower sales volume recorded during the period. Administrative expenses also tumbled by 2.6 percent in 1HFY25 probably due to lower payroll expenses. Other expenses dwindled by 78.49 percent in 1HFY25 maybe on account of lower profit-related provisioning done during the period. Other income also ticked down by 0.67 percent in 1HFY25 perhaps because of higher loss incurred on power generation. ISL recorded a 64.31 percent decline in its operating profit in 1HFY25 with OP margin recorded at 4.36 percent versus OP margin of 9.77 percent registered during the same period last year. Finance cost mounted by 50.6 percent in 1HFY25 due to higher working capital-related borrowings made during the year, ISL posted a 77.30 percent decline in its net profit which stood at Rs.534.09 million in 1HFY25. This translated into EPS of Rs.1.23 in 1HFY25 versus EPS of Rs.5.41 recorded in 1HFY24. NP margin contracted from 5.92 percent in 1HFY24 to 1.68 percent in 1HFY25.

Future Outlook

While monetary easing, declining inflation, and strengthening Pak Rupee provide great impetus for the resumption of construction activities in the country, sales volumes of the steel industry may gradually recover during the ongoing fiscal year due to lower PSDP allocation and petite GDP growth.

Comments

Comments are closed for this article.