**Atlas Battery Limited (PSX: ATBA) was incorporated in Pakistan as a public limited company in 1966. The company manufactures and sells automotive, motorcycle batteries energy storage batteries, and allied products. Shirazi Investments (Private) Limited is the holding company of ATBA holding 58.86 percent of its shares. The company has signed a technical collaboration with Japan Storage Battery Co. Limited for the production and sale of Japanese batteries in Pakistan. ATBA also boasts itself to be the first battery manufacturer to launch branded distilled water and hybrid batteries. **

Pattern of Shareholding

As of June 30, 2024, ATBA has 35.017 million shares outstanding which are held by 2687 shareholders. Associated companies, undertakings, and related parties form the largest shareholder category holding 77.44 percent of ATBA’s shares. This is followed by the local general public having a 16.51 percent stake in the company. Public sector companies and corporations hold 2.81 percent shares of ATBA while joint stock companies account for 2.31 percent shares. The remaining shares are held by other categories of shareholders.

Historical Performance (2019-24)

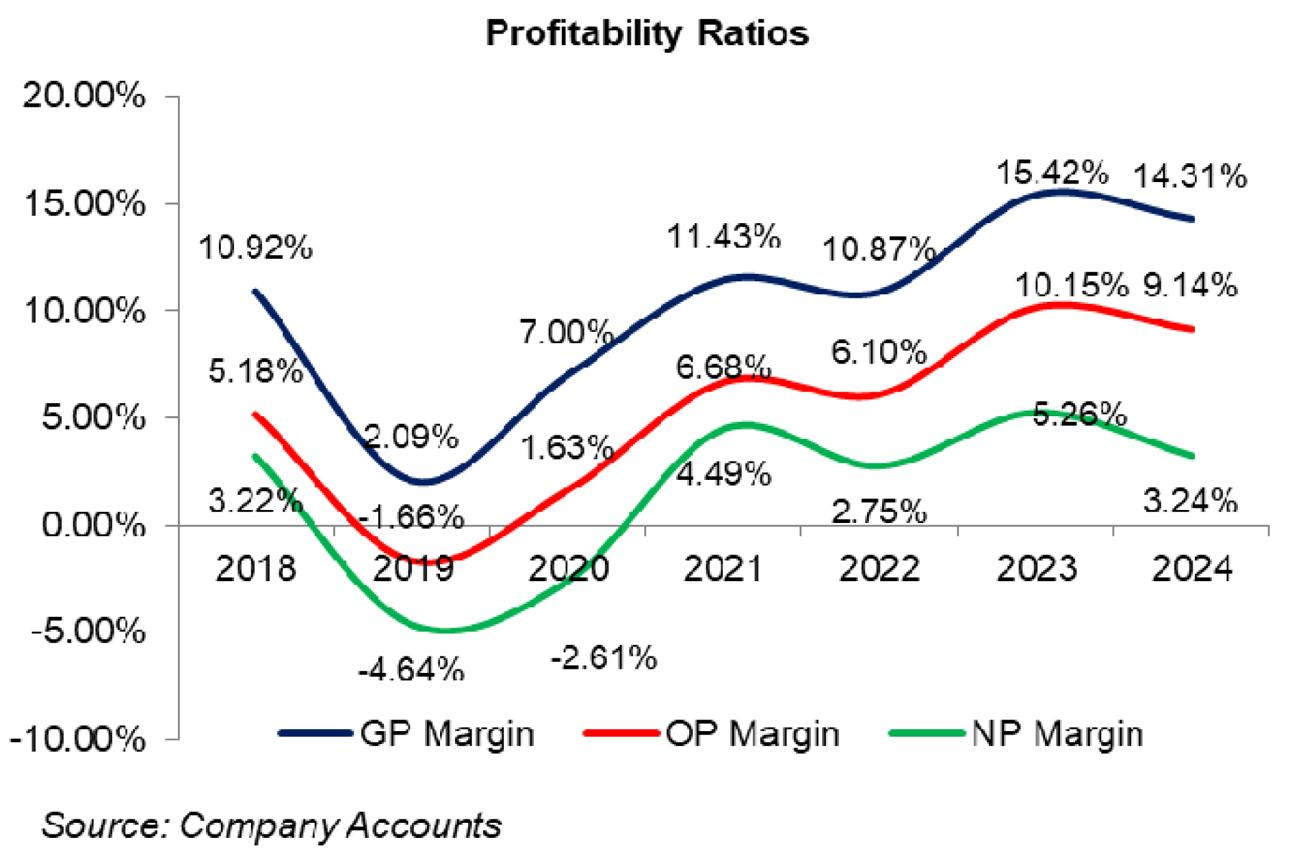

ATBA’s topline took a dip in 2019 and 2020 followed by a rebound until 2023. In 2024, ATBA’s net sales took a dip again. Its bottom line stayed in the negative zone in 2019 and 2020 followed by a staggering turnaround in 2021. In 2022, ATBA’s bottom line took a plunge only to come back stronger in the next year. In 2024, the bottom line considerably shrank. ATBA’s margins also followed a comparable route as its bottom line (see the graph of profitability ratios). The detailed performance review of the period under consideration is given below.

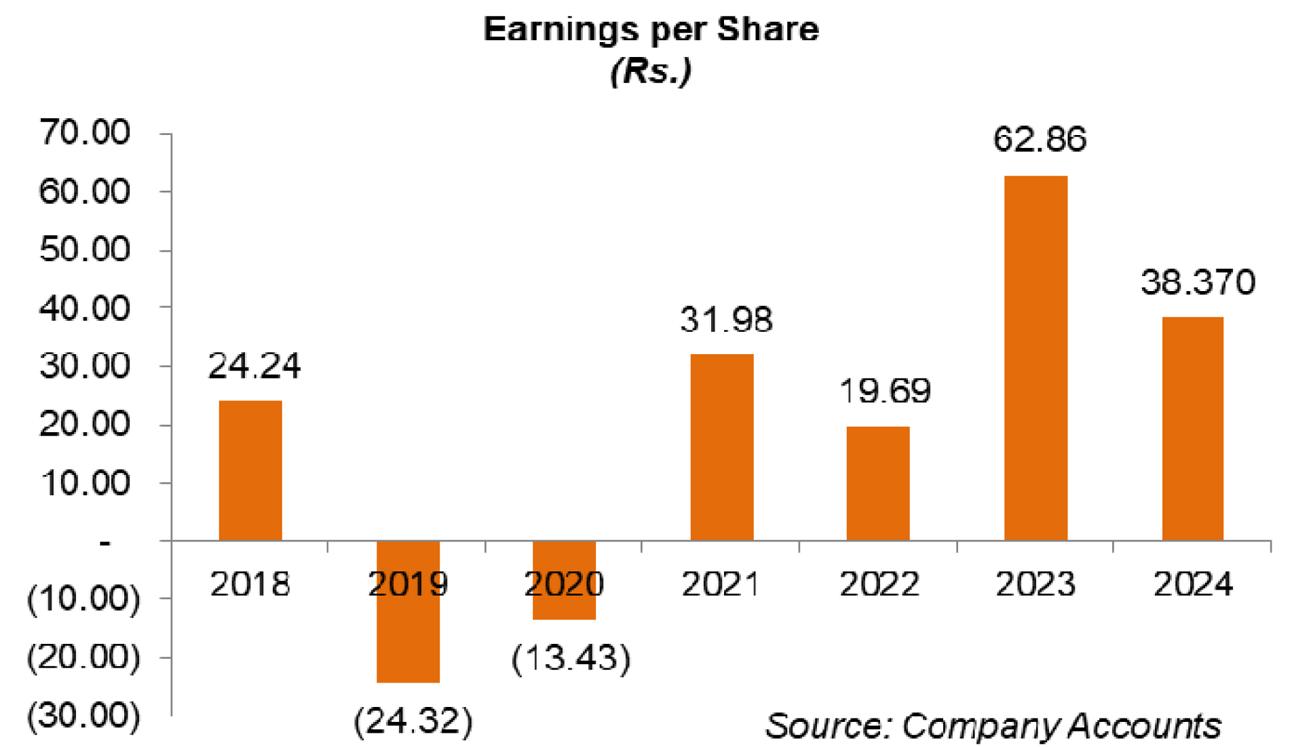

A sneak into the financial statements reveal that 2019 was a challenging year for ATBA. The bottom line showed an uglier picture with tighter margins and operating losses. The reason for the desolate performance in 2019 was a slowdown in the automobile industry due to the high cost of production, depreciation of the Pak Rupee, and higher interest rates during the year. The sale of locally manufactured cars, tractors, trucks, and buses as well as motorcycles and three-wheelers, all registered a decline in 2019, the shocks of which were felt in the sale of automotive parts and accessories including batteries. Another reason for the sluggish demand for batteries in 2019 was the increased power generation which reduced the load shedding and the demand for medium and heavy batteries used in UPS. The result was a 30.33 percent year-on-year drop in ATBA’s topline with the GP margin standing at 2.1 percent in 2019 versus the GP margin of 10.9 percent recorded in 2018. Gross profit in absolute terms also dwindled by 86.69 percent year-on-year in 2019. During the year, a gain on the disposal of operating fixed assets resulted in a massive rise of 421 percent in ATBA’s other income. Distribution expenses slid by 17 percent year-on-year in 2019 due to lesser advertisement & promotional activities as well as lower freight & forwarding charges incurred during the year on account of thinner sales volume. Administrative costs shrank by 9.67 percent in 2019 primarily due to lesser rent & rates as well as smaller charitable contributions. Other expenses also registered a massive 72.79 percent decline in 2019 on account of no fair value loss incurred on investments, no loss incurred on disposal of fixed assets as well as lower profit-related provisioning booked during the year. All these factors couldn’t prevent the company from making an operating loss worth Rs.211.57 million in 2019 versus an operating profit of Rs.949.94 million registered in 2018. Finance cost magnified by 80.93 percent in 2019 owing to enhanced running finance utilization along with rising interest rates. ATBA posted a net loss of Rs.592.46 million with a loss per share of Rs.24.32 as against a net profit of Rs.590.594 million and EPS of Rs.24.24 recorded in 2018.

In 2020, ATBA’s topline further shrank by 1.78 percent year-on-year. This was due to subdued growth in the automobile industry on account of COVID-19. Moreover, the lockdown of industries and businesses had created excess unutilized power capacity which reduced the demand for UPS batteries. The company worked on the cost-cutting measures which resulted in a rise of 229.74 percent rise gross profit with GP margin climbing up to 7 percent in 2020. The operating expenses were also kept in check during the year. This resulted in ATBA making an operating profit worth Rs. 204.48 million in 2020 with an OP margin of 1.63 percent. High finance costs due to increased working capital didn’t let operating profit translate into a positive bottom line. However, the net loss of Rs.327.10 million along with loss per share of Rs.13.43 was 44.79 percent less when compared to that of 2019.

2021 was characterized by a stable macroeconomic environment the effects of COVID-19 began to subside. The automobile industry also rebounded owing to low interest rates which augmented the purchasing power of customers; consequently, the demand for automobiles recoiled, generating demand for automotive batteries. As businesses and industries started operating in full swing after the lockdown period, there was a widespread power deficiency, resulting in improved demand for UPS batteries. Moreover, a significant boost in the sales of solar panels in the off-grid areas further buttressed the demand for medium and small batteries. Improved sales volume and prices drove up ATBA’s topline by 59 percent year-on-year in 2021. This coupled with cost control measures resulted in gross profit multiplying by 159.58 percent in 2021 with GP margin mounting 11.43 percent. Distribution expenses enlarged by 33.77 percent year-on-year in 2021 as the company undertook widespread advertisement and sales promotion drives during the year. Furthermore, improved sales volume resulted in greater freight & forwarding charges incurred during the year. ATBA’s workforce grew from 296 employees in 2020 to 337 employees in 2021, resulting in higher payroll expenses. This pushed up the administrative expenses by 41.32 percent in 2021. However, operating expenses as a proportion of sales remained intact. Other income rose by 55.58 percent in 2021 as a result of dividend income, interest income, scrap sales as well as exchange gain. However, this was nullified by a 135.81 percent rise in other expenses as the company increased profit-related provisioning. All these factors culminated in a 552.12 percent bugger operating profit posted by the company in 2021 with OP margin reaching 6.7 percent. Finance costs which had been on the rise since 2018 gave some respite in 2021 owing to the low discount rate. ATBA registered a net profit of Rs. 895.97 million in 2021 with EPS of Rs. 31.98. The company’s NP margin of 4.5 percent in 2021 was the highest since 2018.

2022 was another encouraging year in a row where the topline took a 25.43 percent year-on-year flight on the back of improved volumes, better sales mix, and prices. Demand for heavy and medium-sized batteries for UPS, solar, and generators remained vigorous during the year. However, the increase in the cost of sales mainly due to elevated prices of raw materials in the global market, declining value of the Pak Rupee, high Indigenous inflation, and energy cost didn’t allow ATBA the healthy topline to trickle down into an encouraging GP margin. ATBA’s GP margin dipped to 10.87 percent in 2022 despite a 19.28 percent rise in gross profit. Distribution expenses hiked by 23.72 percent year-on-year in 2022 on account of increased freight & forwarding due to higher sales volume and escalated prices of POL products. Increased advertising and promotion budget also contributed towards higher distribution expenses incurred by ATBA in 2022. Administrative expenses also swelled by 18.32 percent in 2022 due to an enhancement in the workforce to 346 employees along with an adjustment of the minimum wage rate in line with soaring inflation. Higher exchange loss drove other expenses up by 31.75 percent in 2022. Other income declined by 31.50 percent year-on-year in 2022 on account of negligible dividend and interest income made during the year. ATBA’s operating profit expanded by 14.52 percent in 2022, however, OP margin fell to 6.1 percent. 181.35 percent higher finance cost incurred by the company in 2022 was the consequence of a higher discount rate. Net profit declined by 23 percent year-on-year in 2022 to clock in at Rs.689.44 million with EPS of Rs.19.69 and NP margin of 2.75 percent.

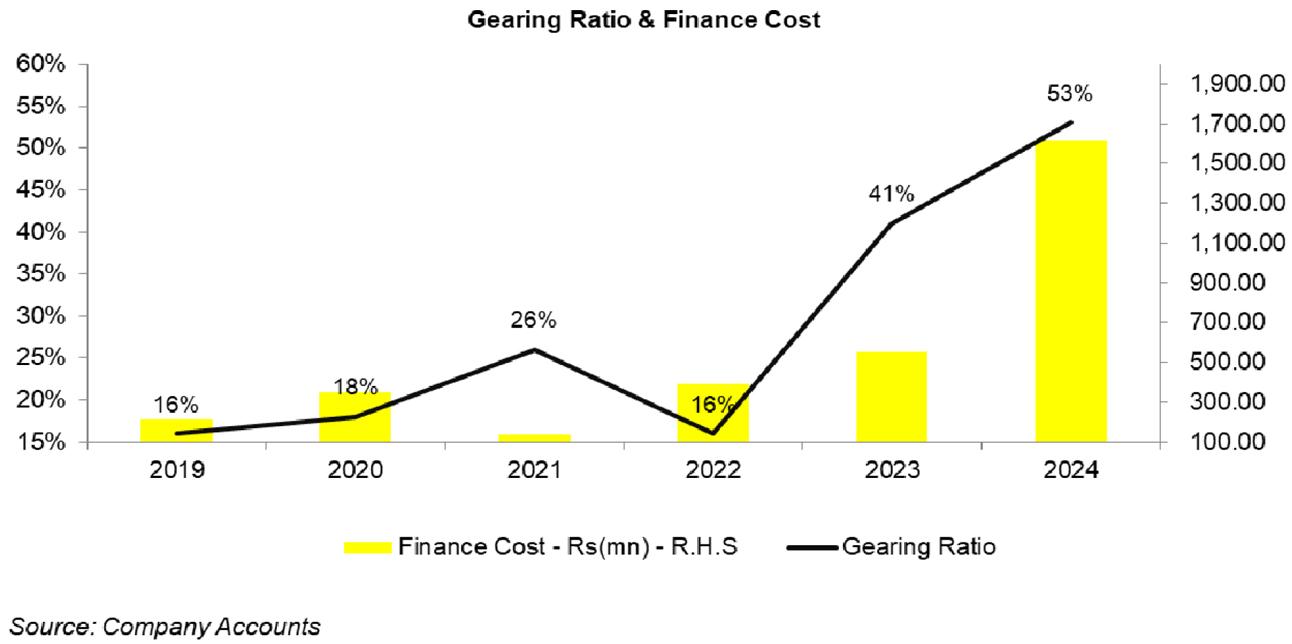

With a 67.23 percent year-on-year escalation in its topline, ATBA closed 2023 on an upbeat note. With load shedding and power outrages rampant in both rural and urban areas, the demand for batteries grew manifold which to a great extent nullified the lower demand from the automobile industry. Encouraging demand in the replacement market coupled with better prices resulted in 137.14 percent year-on-year growth in ATBA’s gross profit in 2023 with its GP margin reaching its optimum level of 15.42 percent. Distribution cost surged by 73.24 percent year-on-year in 2023 on account of rigorous advertising and sales promotion drives conducted by the company coupled with higher freight & forwarding charges on the back of improved sales volume. Higher petroleum prices also drove up distribution expenses in 2023. Administrative expenses also surged by 64.17 percent in 2023 mainly on account of higher payroll expenses. ATBA’s workforce stood at 352 employees in 2023 versus 346 employees in the previous year. Increased profit-related provisioning and exchange loss drove up other expenses by 219.34 percent in 2023. Other income also magnified by 108.21 percent in 2023 due to higher dividend income and scrap sales made during the year. Operating profit increased by 178.32 percent in 2023 with OP margin climbing up to 10.15 percent. Finance cost soared by 41.76 percent year-on-year in 2023 with the gearing ratio reaching its highest level of 41 percent versus 16 percent in the previous year (see the graph of gearing ratio & finance cost). During the year, the company made significant borrowings to meet its working capital requirements. Besides, ATBA also borrowed Rs.750 million under the diminishing Musharaka arrangement to finance BMR. The bottom line also took a hit from the super tax imposed during the year but still managed to build up by 219.28 percent in 2023 to clock in at Rs.2201.24 million with EPS of Rs.62.86 and NP margin of 5.26 percent.

During 2024, ATBA’s topline shrank by 0.92 percent. Weaker demand, high borrowing rates, and import restrictions resulted in the meager performance of the automobile industry in 2024 which produced a profound negative effect on the demand for batteries. Although demand for tall batteries increased during the year due to the rising demand for solar panels, it couldn’t produce any impetus to ATBA’s net sales in 2024. Cost of sales grew by 0.37 percent in 2024 mainly on account of elevated energy tariffs and other input costs. This resulted in an 8 percent contraction in ATBA’s gross profit in 2024 with the GP margin falling down to 14.31 percent. Distribution expenses inched up by only 0.47 percent in 2024 due to reduced sales volume and fewer advertisement & sales promotion drives conducted during the year. Administrative expenses escalated by 31.34 percent in 2024 due to higher payroll expenses due to inflationary pressure. The number of employees was reduced to 346 in 2024. Other income strengthened by 38 percent in 2024 mainly driven by exchange gain and dividend income. Lesser profit-related provisioning and no exchange loss incurred during the year squeezed other expenses by 50.7 percent in 2024. ATBA recorded a 10.83 percent plunge in its operating profit in 2024 with OP margin falling down to 9.14 percent. Finance costs surged by 193.33 percent in 2024 due to higher discount rates and increased short-term borrowings obtained during the year. This resulted in ATBA’s gearing ratio jumping up to 53 percent in 2024. Net profit slid by 38.96 percent to clock in at Rs.1343.649 million in 2024 with EPS of Rs.38.37 and NP margin of 3.24 percent.

Recent Performance (1QFY25)

ATBA’s net sales which started eroding in 2024 continued the same trajectory in the ongoing fiscal year with a year-on-year decline of 2.84 percent recorded in 1QFY25. This was due to a decline in the demand for batteries in the replacement market due to consumers’ shrunken pockets. In line with reduced sales volume, the cost of sales dropped by 2.88 percent in 1QFY25. This resulted in a 2.57 percent thinner gross profit recorded in 1QFY25. However, the GP margin remained intact at 13 percent. Distribution and administrative expenses surged by 16.37 percent and 13.68 percent respectively during 1QFY25 due to inflationary pressure. Robust dividend income and exchange gain translated into a 24.7 percent rise in other income in 1QFY25. Conversely, lower provisioning for WWF and WPPF drove other expenses down by 0.43 percent during 1QFY25. Operating profit tapered off by 13 percent in 1QFY25 with OP margin clocking in at 7.13 percent versus OP margin of 7.96 percent recorded in 1QFY24. Finance costs slumped by 17.9 percent in 1QFY25 due to monetary easing and reduced working capital-related borrowings obtained during the period. ATBA recorded a 14.57 percent decline in its net profit which stood at Rs.224.59 million in 1QFY25 with EPS of Rs.6.41 and NP margin of 2.27 percent. This was against the EPS of Rs.7.51 and NP margin of 2.58 percent recorded in 1QFY24.

Future Prospects

With the onset of monetary easing, lifted import restrictions, and lowered inflation, the automobile industry is showing improved performance. This will directly impact the demand for batteries. This coupled with increased consumer inclination towards solar panel installation will keep the demand for batteries buoyant in the coming quarter. In order to improve its margins and profitability, the company must also focus on attaining operational efficiency as well as diversification of product lines and geographical markets.

Comments

Comments are closed for this article.