Ghani Chemical Industries Limited (PSX: GCIL) was incorporated in Pakistan as a private limited company in 2015 and was converted into a public limited company in 2017. The principal activity of the company is the manufacturing, trading & sale of medical and industrial gases and chemicals.

Pattern of Shareholding

As of June 30, 2024, GCIL has a total of 500.188 million shares outstanding which are held by 6623 shareholders. Associated companies have the majority stake of 74.34 percent in the company followed by individuals holding 19.31 percent shares. Joint stock companies account for 3.89 percent shares of GCIL. The remaining shares are held by other categories of shareholders.

Historical Performance (2022-24)

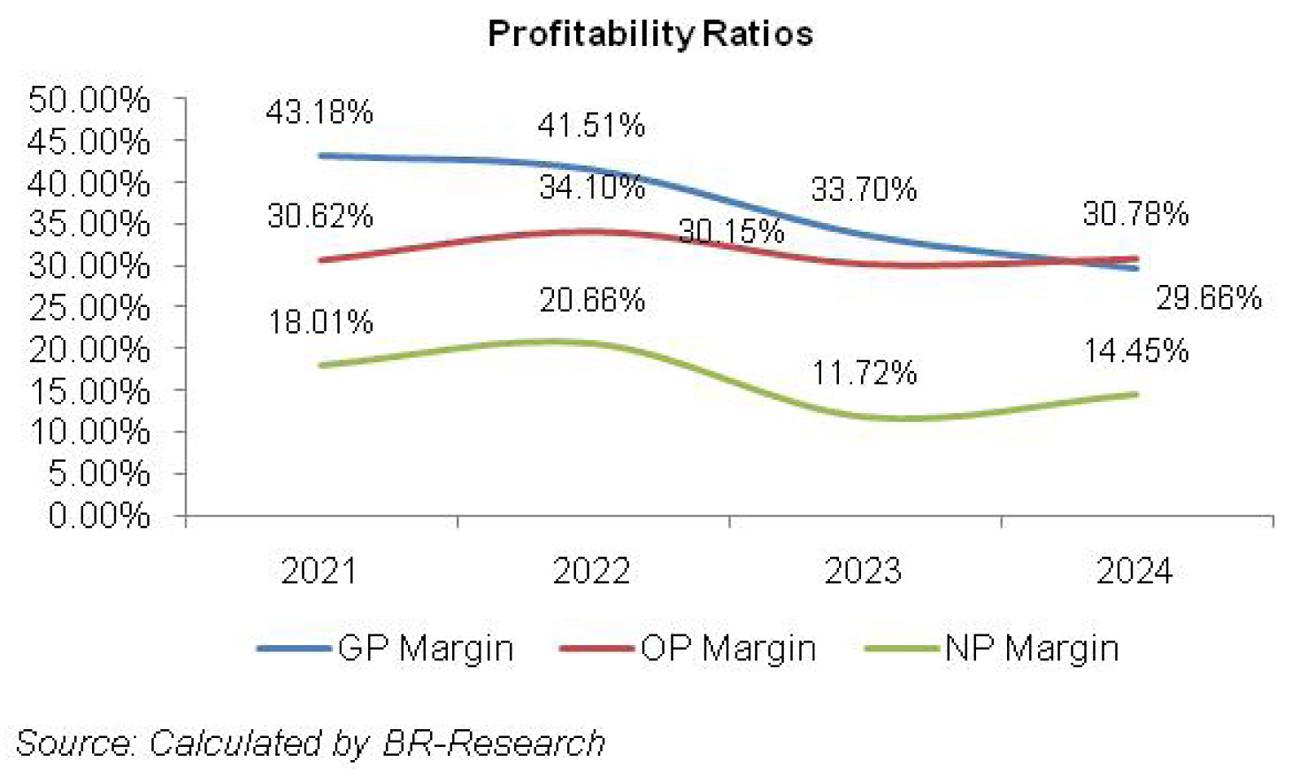

GCIL’s topline has posted year-on-year growth over the period under consideration. Conversely, its bottom line posted a plunge in 2023. In 2022, GCIL’s gross margin registered a decline while its operating and net margins posted growth. This was followed by a decline in all the margins in 2023. In 2024, gross margin continued to fall while operating and net margins posted recovery. The detailed performance review of the period under consideration is given below.

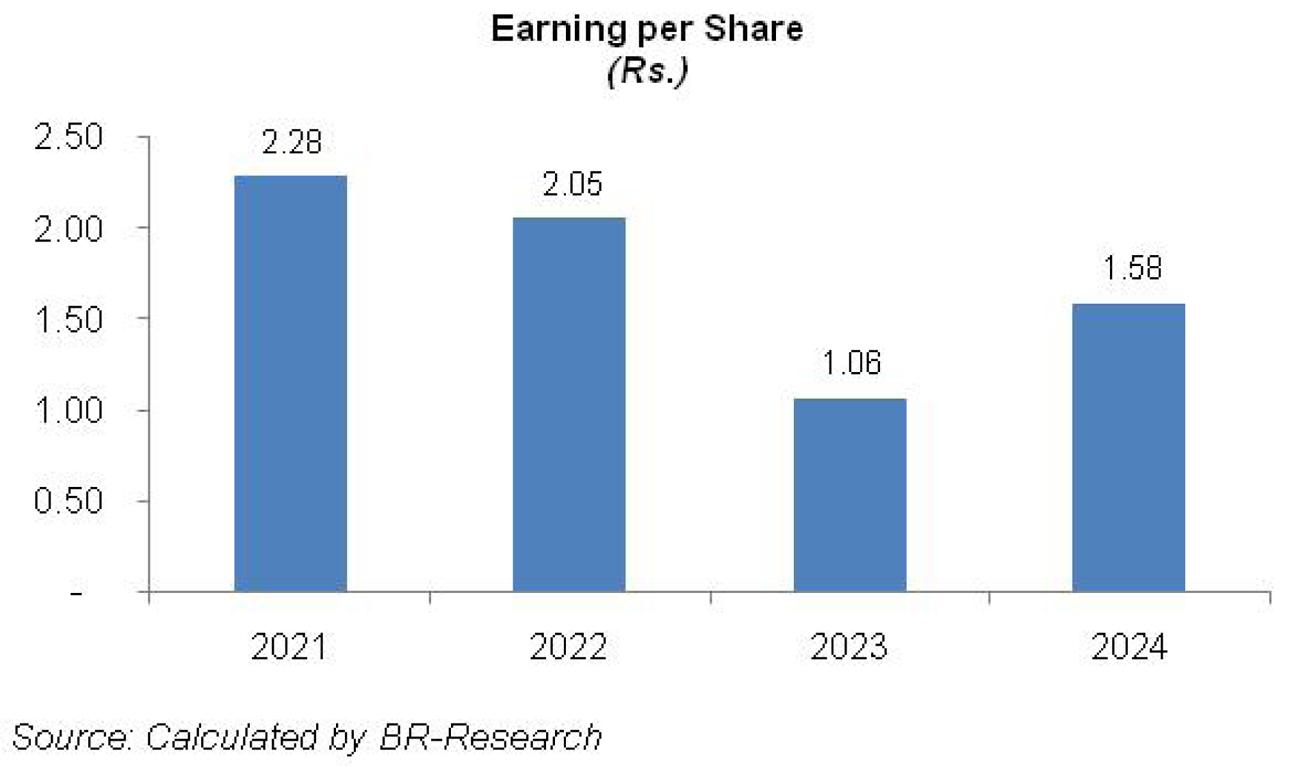

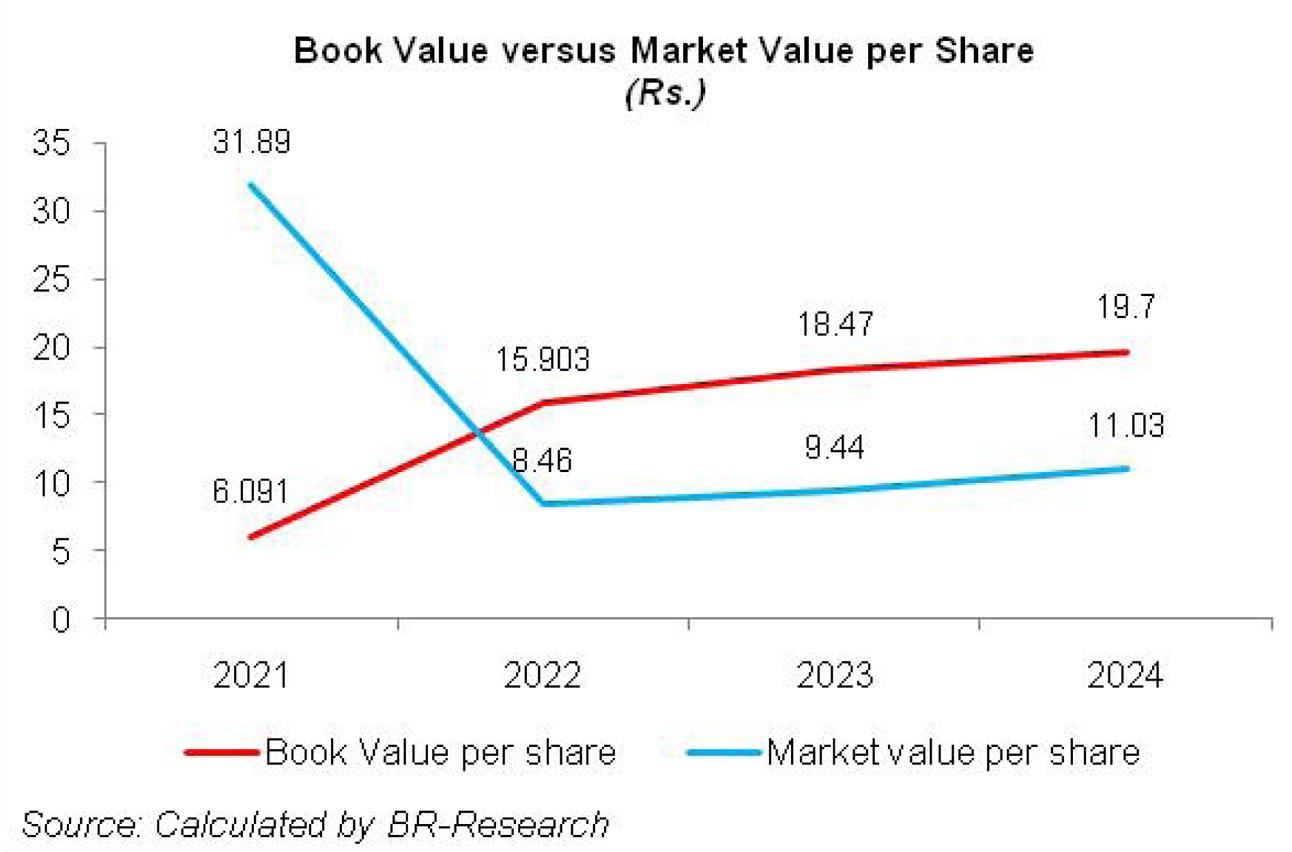

In 2022, GCIL’s topline posted year-on-year growth of 9.804 percent. Revenue proceeds from supplies and services, both posted year-on-year growth during the year; however, revenue from supplies forms the major chunk of GCIL’s sales. Cost of sales mounted by 13 percent in 2022 mainly on account of fuel & power charges which are the only raw materials for the manufacturing of industrial and medical gases. This translated into a 5.57 percent uptick recorded in GCIL’s gross profit in 2022, however, its GP margin nosedived from 43.18 percent in 2021 to 41.51 percent in 2022. Distribution expense ticked up by 0.615 percent in 2022 due to transportation charges. Administrative expenses surged by 28.67 percent in 2022 due to fee & subscription charges as well as adjustments arising upon the merger of GTECH. GTECH was merged into GCIL in w.e.f December 31, 2021; however, the court order for the same was received in October 2022. Other expenses mounted by 18.86 percent in 2022 on account of higher profit-related provisioning booked during the year. Other income posted a staggering 417.536 percent in 2022 due to gain recorded on the disposal of operating fixed assets, credit balances written back, advance received against leasehold land as well as mark-up income received from bank accounts and advances to an associated company. GCIL posted a 22.28 percent rise in its operating profit in 2022 with OP margin jumping up from 30.62 percent in 2021 to 34.1 percent in 2022. Finance cost ticked up by 10.26 percent in 2022 due to monetary tightening coupled with higher outstanding borrowings. Net profit picked up by 25.94 percent in 2022 to clock in at Rs.870.449 million. This translated into EPS of Rs.2.05 in 2022 versus EPS of Rs.2.28 posted in 2021. The drop in EPS was due to an increase in the working capital of GCIL as the company increased its authorized capital during the year. NP margin improved from 18 percent in 2021 to 20.66 percent in 2022.

In 2023, GCIL’s topline posted a paltry 2.8 percent year-on-year growth. Due to the slowdown of industrial activity on account of economic and political instability, the company produced 58.48 million cubic meters of gas, down 1.24 percent year-on-year. This resulted in a capacity utilization of 64 percent in 2023 versus a capacity utilization of 82 percent achieved in 2022. The cost of fuel and power wreaked havoc on the overall cost of sales which mounted by 16.54 percent in 2023. This squeezed the gross profit by 16.56 percent in 2023 with GP margin falling down to 33.70 percent. Lower sales volume resulted in a 36.67 percent drop in distribution expenses in 2023. Administrative expenses also surged by 15 percent in 2023 due to higher payroll expenses on account of inflationary pressure. Number of employees stood intact at 309 in both the years. Other expenses dipped by 28.82 percent in 2023 predominantly due to lesser profit-related provisioning booked during the year. Other income multiplied by 16 percent in 2023 due to massive return from bank deposits and advances to an associated company which was greatly offset by lower gain recorded on the sale of operating fixed assets. GCIL’s operating profit dipped by 9.1 percent in 2023 with OP margin dropping to 30.15 percent. Finance costs escalated by 63 percent in 2023 due to higher discount rates as well as increased borrowings to meet the CAPEX requirement of the company. GCIL recorded a 41.65 percent thinner bottom line to the tune of Rs.507.891 million in 2023. This translated into EPS of Rs.1.06 and NP margin of 11.72 percent. In 2023, the company increased its authorized capital from 550 million ordinary shares to 800 million ordinary shares and 50 million Class B shares.

In 2024, GCIL’s topline expanded by 25.51 percent. While the industrial activity remained muted, the company produced 55.470 million cubic meters of gas, down 5.15 percent year-on-year. This translated into capacity utilization of 61 percent in 2024. However, the company sold off the surplus finished goods inventory from the last year which resulted in increased sales volume. The company identified new avenues to improve its market penetration and volume during 2024. Cost of sales escalated by 33.16 percent in 2024 due to high electricity & gas prices. Gross profit, in absolute terms, enhanced by 10.46 percent in 2024, however, the GP margin plunged to 29.66 percent. Distribution expense slid by 25.20 percent in 2024 due to lower transportation charges incurred during the year. This is because the company set up a new plant for the manufacturing of Oxygen and Nitrogen gases at Port Qasim to deliver the long-term agreement signed with Engro Polymer & Chemicals Limited. The setup of the new production facility provided proximity to major customers, hence lower transportation costs. Administrative expenses spiked by 12.27 percent in 2024 due to higher electricity & utility charges, vehicle running & maintenance charges as well as depreciation expenses incurred during the year. GCIL expanded its workforce to 357 employees in 2024 to fulfill the rising demand. Other expenses multiplied by 36 percent in 2024 due to higher profit-related provisioning booked during the year. Other expense was conveniently offset by 66.53 percent higher other income recognized during the year. This was mainly the result of compensation charges recovered from a customer due to short lifting of chemical supplies, return on advances to associated companies, gain on disposal of operating fixed assets and commission income earned due to services work at a hospital. GCIL recorded a 28.16 percent improvement in its operating profit in 2024 with OP margin ticking up to 30.78 percent. Finance costs ticked up by 4 percent in 2024 due to increased borrowings and discount rates. GCIL recorded a gearing ratio of 28.96 percent in 2024. Net profit improved by 54.72 percent to clock in at Rs.785.807 million with EPS of Rs.1.58 in 2024.

Recent Performance (1QFY25)

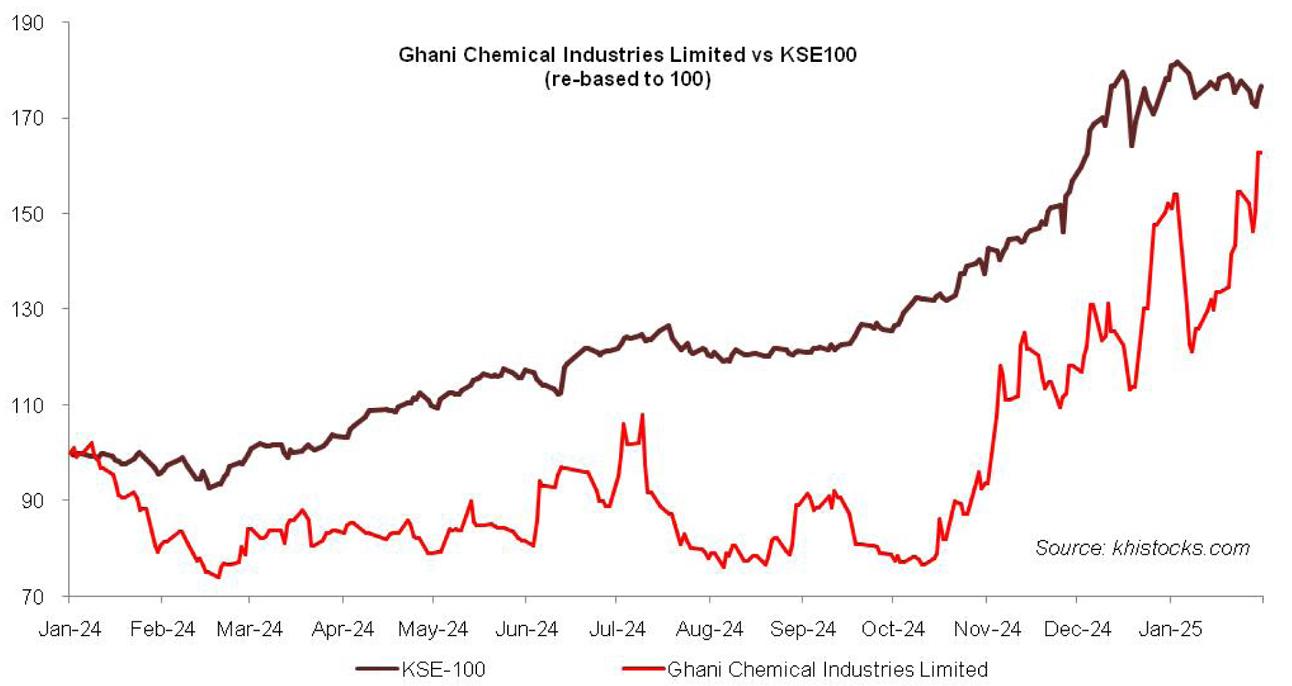

GCIL posted a staggering year-on-year topline growth of 42.81 percent in 1QFY25. This was the result of a phenomenal rise in sales volume. However, elevated electricity tariff resulted in a 42.15 percent spike in the cost of sales in 1QFY25. Gross profit grew by 43.96 percent in absolute terms; however, GP margin posted a marginal growth from 36.42 percent in 1QFY24 to 36.72 percent in 1QFY25. Distribution expense ticked down by 8.61 percent in 1QFY25 due to proximity to customers which reduced the transportation charges. Conversely, administrative expenses surged by 28.98 percent in 1QFY25 due to higher payroll expenses on the back of workforce expansion and inflationary pressure. Higher electricity & utility charges might also have driven up the administrative expenses in 1QFY25. A 74.26 percent spike in other expenses in 1QFY25 appears to be the consequence of higher profit-related provisioning. Other income picked up by 25.27 percent in 1QFY25. This might be due to the return of long-term investments made in the subsidiary companies – Ghani Gases (Private) Limited and Ghani Power (Private) Limited during 1QFY25. Operating profit grew by 44.61 percent in 1QFY25 with OP margin clocking in at 35.95 percent versus OP margin of 35.50 percent recorded in 1QFY24. Finance cost escalated by 10.83 percent in 1QFY25 due to increased external borrowings. GCIL recorded 34.14 percent growth in its topline which stood at Rs.303.145 million in 1QFY25. This translated into EPS of Rs.0.61 versus EPS of Rs.0.46 recorded in 1QFY24. NP margin inched down from 18.64 percent in 1QFY24 to 17.50 percent in 1QFY25.

Future Outlook

With the improvement in macroeconomic fundamentals, GCIL is anticipating improved demand from the industrial sector. The company is also exploring new avenues of growth in both private and public healthcare sectors across the country to enhance its revenue. Moreover, as the petroleum exploration and production market is set is grow, the demand of nitrogen will eventually increase in order to comply with the stricter environmental regulations.

The company has also made sizeable investment for building 275TPD ASU plant in the KPK for manufacturing liquid oxygen, nitrogen and argon to avoid the complexities associated with the transport of these gases. This coupled with import substitute Calcium carbide project being set up at Hattar, SEZ, KPK provide the company with immense growth potential.

Recently, the company has entered into a Gas Sales and Purchase Agreement (GSPA) with Mari Energies Limited and OGDC for the supply of 3 MMSCFD natural gas during an extended well testing period (EWT) from Maiwand-X1 discovery in Baluchistan. This will enable GCIL to achieve efficiency in its energy cost and market/sell gas to industrial units across the country. GCIL also plans to set up its own gas processing facility in the area which will greatly buttress its revenues.

Comments

Comments are closed for this article.