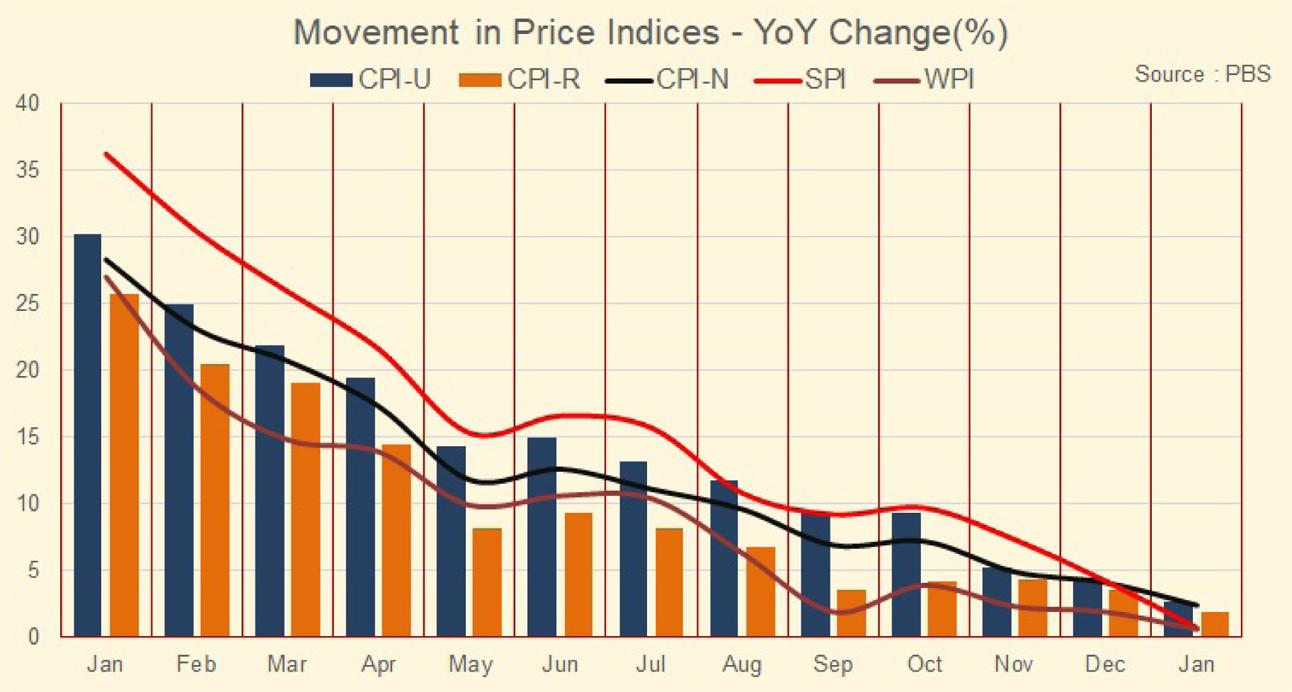

The headline inflation nosedived to 2.4 percent—the lowest level since October 2015—down from 28.3 percent last year. The decline is partly attributed to the high base effect and partly to a lower monthly increase, which averaged 0.3 percent over the last 12 months compared to 2.2 percent in the previous 12 months. Thus, inflation is surely and truly falling. However, prices on an aggregate basis are still rising from a higher base, offering little to no relief for the masses.

The decline is primarily attributed to falling food prices (just as they were a key driver during the sharp increase), which dropped by 3.1 percent year-on-year. On an aggregate basis, food prices have declined, with the impact most visible in perishable items, which are down by 10.3 percent year-on-year. Wheat products, such as roti, have seen prices drop by one-third, and a similar trend is observed in eggs.

Another notable area of lower inflation is energy—electricity and fuel prices have declined by 15.6 percent and 2.5 percent, respectively, over the past twelve months, thanks to falling global oil and hydrocarbon prices. These items saw sharp increases in 2022 and 2023, contributing significantly to rising food inflation during that period.

The skyrocketing inflation in 2022 and 2023 was driven by the global commodity supercycle and sharp currency depreciation. Now, with a reversal in global commodity prices and a stable currency, inflation has nosedived. Other contributing factors included unabated domestic demand in 2022 and 2023, fueled by loose fiscal and monetary policies. However, both policies were tightened in 2024, helping to curb inflation.

However, the decline in inflation is not uniform across all sectors. Apart from food and energy, some pressure points remain—such as clothing and footwear, health, education, and miscellaneous items—where inflation remains in double digits. These categories collectively account for 20 percent of the overall Consumer Price Index (CPI), which is two-fifths of the food index. For the middle class, particularly the salaried segment, the weight of non-food and non-energy expenses is much higher. They continue to bear the brunt of inflation in areas such as children’s school fees, healthcare expenses for the elderly, and the cost of durable goods and services.

Core inflation remains relatively sticky compared to headline inflation—it declined to 8.8 percent in January 2025, down from 20.5 percent in the same period last year. However, core inflation never surged to extreme levels, and its decline has been more gradual. The rural core inflation remains in double digits, further straining rural communities where farm income suppression is high.

The decline in wheat and other food prices, while easing the burden on urban dwellers, is making life more challenging for rural farmers. This, in turn, is negatively affecting the demand for various goods and services, keeping economic growth in check.

This is the brief story of highly volatile inflation—a sharp spike followed by a similarly steep decline. Inflation appears to be bottoming out, likely hovering around 2-5 percent over the next three months before starting to rise again. Food prices, in particular, may have already hit their lowest point, with an expected surge during the upcoming Ramadan and Eid season, as demand for food items—especially perishables—typically increases.

Another source of inflationary pressure could stem from a wage-price spiral. As the economy recovers, employees may demand higher wages, which could, in turn, drive overall demand and put upward pressure on prices. Additionally, the transmission of a 1,000 basis point decline in interest rates may stimulate demand, further contributing to inflation.

Currency depreciation could also play a role. As economic activity picks up, higher imports will eventually be reflected in exchange rate adjustments. Currently, the strengthening USD index, combined with a stable PKR, is causing the latter to appreciate against other currencies. However, the PKR may realign in the coming months.

Furthermore, in a few months, the base effect will reverse. Right now, a high base from last year is making inflation figures appear lower, but as this base effect fades, inflation figures may start to climb again.

At any given time, inflation is just a number—what truly matters is maintaining stable, single-digit inflation. FY26 will be a challenging year in that regard.

Comments

Comments are closed for this article.