Pakistan Reinsurance Company Limited (PSX: PAKRI) was incorporated in Pakistan as public limited company in 2000. The principal activity of the company is providing reinsurance and other insurance services.

Pattern of Shareholding

As of December 31, 2023, PAKRI has a total of 900 million shares outstanding which are held by 3936 shareholders. The secretary ministry of commerce is the major shareholder of PAKRI with 51 percent shares followed by State Life Insurance Corporation of Pakistan holding 24.41 percent shares. Local general public has 15.76 percent stake in PAKRI while banks, DFIs and NBFIs hold 5.08 percent shares. Around 2.07 percent of PAKRI’s shares are held by insurance companies. The remaining shares are held by other categories of shareholders.

Financial Performance (2019-23)

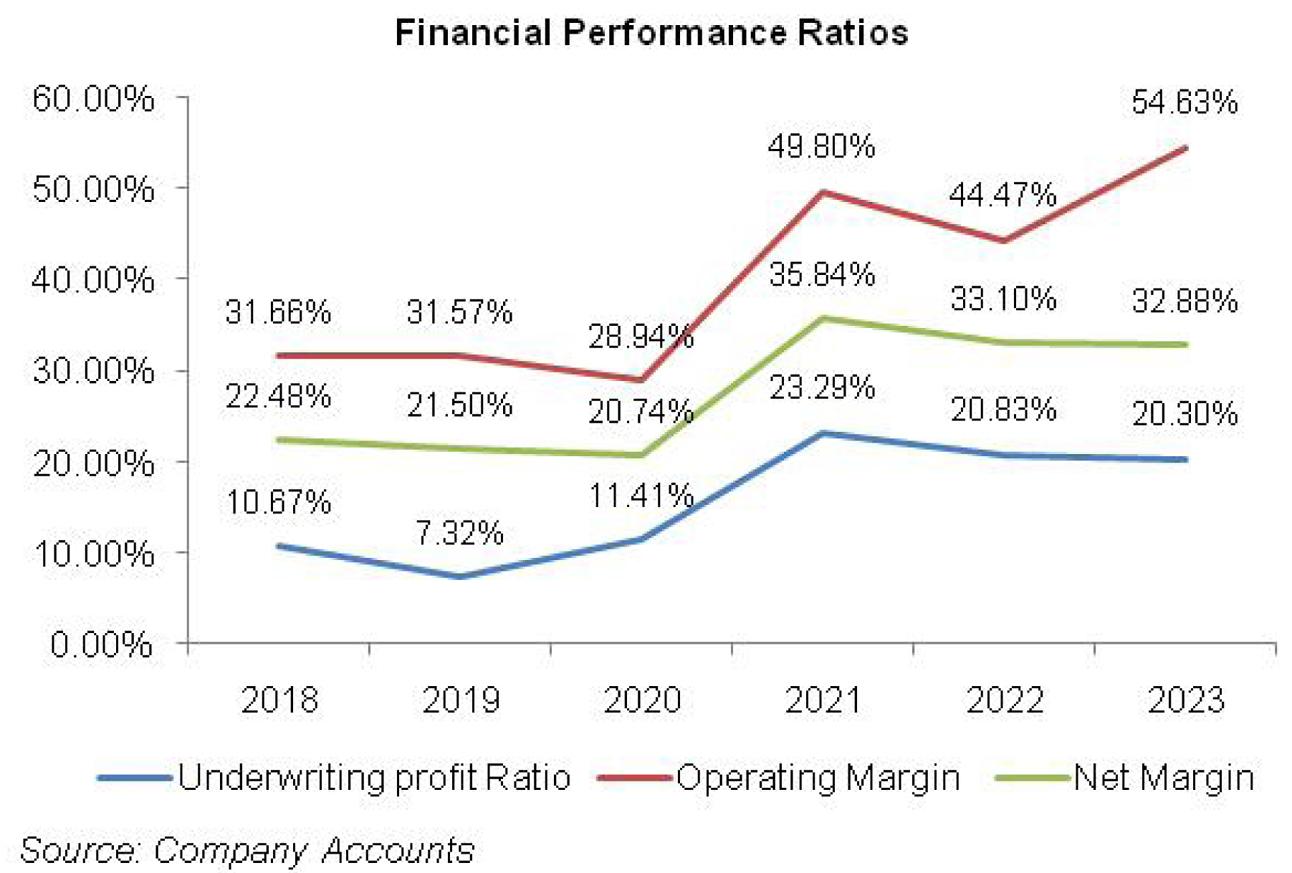

Except for a year-on-year decline in 2020, PAKRI’a topline i.e. net insurance premium has registered reasonable growth over the period under consideration. Its bottomline also followed the suit. The company’s underwriting profit ratio and net margin dipped in 2019 followed by a rebound for the next two years to attain their highest level in 2021 after which it began to shrink. Its operating margin also followed the similar trajectory until 2022, however, climbed at its optimal level in 2023 (see the graph of financial performance ratios). The detailed performance review of the period under consideration is given below.

In 2019, PAKRI’s net insurance premium posted 26.39 percent year-on-year rise. In accordance with the increased business, insurance claims and acquisition expenses also grew by 36.31 percent in 2019. PAKRI’s claim ratio grew from 54.72 percent in 2019 to 61.68 percent in 2020. The company was able to cut down its management expense by 8.24 percent by right-sizing its workforce from 194 employees in 2018 to 149 employees in 2019. This resulted in management expense ratio of 11.22 percent in 2019 versus management expense ratio of 15.46 percent recorded by the company in 2018. During the year, PAKRI booked provision worth Rs.122.924 million on doubtful debts. Higher insurance claims and acquisition expenses as well as provision for doubtful debt resulted in 13.26 percent year-on-year plunge in underwriting results in 2019 with underwriting ratio falling down from 10.67 percent in 2018 to 7.32 percent in 2019. This was majorly recompensed by 25.68 percent higher investment income recorded by PAKRI in 2019. This was primarily the effect of higher dividend income and income from investment in government securities. Rental income also grew by 12.16 percent in 2019. This represented income from letting out of PRC tower. Other income also improved by 85.82 percent in 2019 due to hefty exchange gain as well as net return on loans to employees. Other expense grew by 26.93 percent in 2019 which was mainly due to higher fee & subscription charges, provision for WWF as well as provision against lease rental payable to Karachi Port Trust (KPT). PAKRI also registered finance cost of Rs.1.74 million in 2019 as against no finance cost incurred in the previous year. This was due to the fact that the company entered into an agreement with KPT for lease of land. Operating profit grew by 26 percent in 2019 yet OP margin slightly tumbled from 31.66 percent in 2018 to 31.57 percent in 2019. PAKRI’s profit from window Retakaful operations grew by 8379 percent in 2019 to clock in at Rs.9.24 million. The company’s net profit grew by 20.87 percent year-on-year in 2019 to clock in at Rs.1484.282 million with EPS of Rs.4.95 versus EPS of Rs.4.09 recorded in 2018. However, NP margin fell from 22.48 percent in 2018 to 21.5 percent in 2019.

In 2020, PAKRI’s topline dropped by 2.84 percent year-on-year on account of economic slowdown due to COVID-19. Net claims, commission and acquisition expenses tumbled by 11.85 percent during the year. As a consequence, claim ratio nosedived to 58.5 percent in 2020. PAKRI kept a check on its management expenses which slumped by 13.96 percent in 2020 due to lower payroll expense as the company further streamlined its workforce. Management expense ratio slid to 9.94 percent in 2020. PAKRI also booked provision worth Rs.426.553 million on doubtful debts, up 247 percent year-on-year. Higher provision for doubtful debt drove up the company’s underwriting result by 51.47 percent in 2020, resulting in higher underwriting ratio of 11.41 percent. Investment income and rental income grew by 20.15 percent and 19.34 percent respectively in 2020. This was on account of robust dividend income and return on government securities earned during the year and rental income received from letting out of PRC tower. Conversely, other income shrank by 90.12 percent in 2020 due to lower return on bank deposits and no exchange gain made during the year. Other expense escalated by 56.7 percent in 2020 due to exchange loss. Finance cost also increased by 58.09 percent in 2020 to clock in at Rs.2.75 million due to slight uptick in lease liability. PAKRI registered 10.94 percent lower operating profit in 2020 which culminated into OP margin of 28.94 percent. Profit from window Retakaful operations posted tremendous growth of 229.52 percent in 2020. This was the second year of Retakaful window operations. Net profit dropped by 6.25 percent year-on-year to clock in at Rs.1391.441 million with EPS of Rs.4.64 and NP margin of 20.74 percent.

In 2021, PAKRI’s net insurance premium posted 7.7 percent year-on-year rise. Conversely, its net insurance claims tumbled by 3.74 percent in 2021, resulting in a lower claim ratio of 52.28 percent. Net commission and other acquisition cost grew by 4.67 percent in 2021. After two successive years of decline in management expense, PAKRI recorded 9.33 percent higher management expense in 2021. This was on account of higher payroll expense incurred during the year. This was despite the fact that the number of employees continued to taper to clock in at 159 in 2021. Provision against doubtful debt slid by 97.94 percent in 2021 to clock in at Rs.8.782 million. This resulted in a staggering 119.77 percent higher underwriting result posted by PAKRI in 2021 with underwriting ratio of 23.29 percent – the highest during the period under consideration. Investment income failed to impress in 2021 and contracted by 5.91 percent due to lower return on debt securities on account of monetary easing. Rental income improved by 25.13 percent in 2021. Other income also posted 91.31 percent due to hefty exchange gain. PAKRI was able to cut down its operating expense by 63.72 percent in 2021 as the company didn’t book exchange loss during the year. Finance cost also dropped by 7.31 percent in 2021 due to monetary easing. Furthermore, fair value gain on investment property worth Rs.698.055 million recorded in 2021 further buttressed the operating results. PAKRI’s operating profit grew by 85.34 percent in 2021 with OP margin of 49.8 percent. Profit from window Retakaful operations slumped by 47.58 percent in 2021, yet PAKRI was able to post a tremendous 86.11 percent rise in its bottomline which clocked in at Rs.2589.587 million in 2021 with EPS of Rs.2.88 and NP margin of 35.84 percent – the highest NP margin achieved during the period under consideration.

PAKRI recorded 9.74 percent uptick in its net insurance premium in 2022. However, with 14.14 percent higher net insurance claims recorded during the year, claim ratio increased to 54.38 percent in 2022. Overall, insurance claim and acquisition expense registered 10.12 percent surge in 2022. Drastic 109.66 percent escalation in management expense in 2022 was due to hefty payroll expense as PAKRI enhanced its workforce to incorporate 181 employees. This resulted in management expense ratio of 19.28 percent in 2022 versus 10 percent in 2021. After three successive years of booking provision on doubtful debt, the company booked reversal worth Rs.542.510 million in 2022. Underwriting results declined by 1.83 percent in 2022 with underwriting ratio falling down to 20.83 percent. Investment income, rental income and other income performed quite well during the year, registering growth of 36.33 percent, 21.33 percent and 194.7 percent respectively in 2022. Monetary tightening buttressed the profit on debt securities, resulting in higher investment income in 2022. Higher discount rate also drove up return on bank deposits which coupled with higher exchange gain strengthened PAKRI’s other income in 2022. Finance cost grew by 8.32 percent in 2022 due to upward cycle of discount rate while other expense declined by 13 percent due to lower fee & subscription charges incurred during the year. PAKRI’s operating profit lowered by 2 percent in 2022 with OP margin clocking in at 44.47 percent. Profit from window Retakaful operations which dropped in 2021, registered 90.27 percent rise in 2022. PAKRI’s net profit inched up by 1.36 percent in 2022 to clock in at Rs.2626.828 million with EPS of Rs.2.92 and NP margin of 33.10 percent.

2023 proved to be a seamless year for PAKRI with 17.58 percent higher net insurance premium recorded during the year. Net insurance claims grew by 9.17 percent during the year, culminating into claim ratio of 50.49 percent – the lowest during the period under consideration. Overall, insurance claims, commission and acquisition expense ticked up by 6.67 percent in 2023. PAKRI registered the lowest commission expense ratio of 10.18 percent in 2023. Commission expense ratio stood at 19.16 percent in 2019 and since then it has dropping unabatedly. Management expense ratio grew by 2.7 percent in 2023. While payroll expense was in check during the year, depreciation expense, repair & maintenance and computer related expenses contributed towards higher management expense during the year. PAKRI booked provision worth Rs.216.799 million against doubtful debts in 2023 as against reversal recorded in the previous year. Underwriting results improved by 14.58 percent in 2023, resulting in an underwriting ratio on 20.3 percent – slightly lower than last year. Investment income grew by 78.54 percent in 2023 primarily due to a hefty rise in profit from debt securities due to the unprecedented level of discount rate. The company recorded 17.29 percent higher rental income in 2023 from letting out of the PRC tower. Other income also improved by 185.56 percent in 2023 on account of tremendous exchange gain due to depreciation in the value of local currency as well as higher return on deposits due to elevated discount rate. Other expenses surged by 8517.76 percent in 2023 due to a write-off of the amount due from other insurers during the year. PAKRI’s operating profit strengthened by 44.45 percent in 2023 of 54.63 percent – the highest during the period under consideration. Profit from window Retakaful operations performed quite well during the year and posted a 214.34 percent year-on-year rise in 2023 to clock in at Rs.95.469 million. Net profit grew by 16.78 percent to clock in at Rs.3065.248 million in 2023 with EPS of Rs.3.410 and NP margin of 32.88 percent.

Recent Performance (1QCY24)

With a 10 percent rise in net insurance premiums and a 14.55 percent decline in net insurance claims, its claim ratio dropped to 51.82 percent in 1QCY24 versus 66.73 percent during the same period last year. Net commission and other acquisition cost registered a negligible 0.37 percent year-on-year rise in 1QCY24. Management expenses soared by 57.25 percent in 1QCY24 due to elevated payroll expenses and depreciation expenses. This resulted in management expense ratio of 13.09 percent in 1QCY24 versus 9.16 percent in 1QCY23. PAKRI’s underwriting results improved by 108.34 percent in 1QCY24 with a staggering underwriting profit ratio of 25.27 percent versus 13.35 percent during the same period last year. Investment income and rental income built up by 72.87 percent and 10.89 percent respectively during the period. A high discount rate was the main contributor to higher profit on debt securities which buttressed investment income in 1QCY24. Other income couldn’t sustain its growth trajectory and dropped by 45 percent during 1QCY24. Other expenses also shrank by 66.16 percent during the period under consideration. PAKRI recorded 59.19 percent higher operating profit in 1QCY24 with an OP margin of 56.83 percent versus 39.28 percent in 1QCY23. Profit from window Retakaful operation continued to attain new heights and recorded 220.37 percent growth in 1QCY24. Net profit improved by 45.84 percent year-on-year to clock in at Rs.947.604 million in 1QCY24 with EPS of Rs.1.05 versus EPS of Rs.0.72 during a similar period last year. NP margin also strengthened from 26.5 percent in 1QCY23 to 35.12 percent in 1QCY24.

Future Outlook

PAKRI’s market penetration and credibility are evident from the fact that its top line is attaining new heights after a downtick last seen in 2020. The shrinking claim ratio over the years also shows that the company is getting more and more efficient in assessing risk and has stricter underwriting criteria. Its window Retakaful operation has also gained traction in a very short span of time and its contribution to the overall bottomline is expanding by the time. The company is proficiently managing its assets as evidenced by robust investment income and other income. With vigorous financial fundamentals, PAKRI is all embraced to navigate the evolving macroeconomic landscape.

Comments

Comments are closed for this article.