Ittefaq Iron Industries Limited (PSX: ITTEFAQ) was incorporated in Pakistan as a private limited company in 2004 and was previously known as Ittefaq Sons Private Limited. The company was converted into a public limited company in 2017. That is when it also changed its name. The company is engaged in the manufacturing of Iron bars and Girders.

Pattern of Shareholding

As of June 30, 2022, ITTEFAQ has a total of 144.34 million shares outstanding which are held by 5187 shareholders. Local general public with a stake of 85.53 percent forms the largest shareholding category of ITTEFAQ. This is followed by Directors, CEO, their spouse and minor children holding 8.16 percent shares of ITTEFAQ. Around 2.9 percent of the company’s shares are held by joint stock companies while 2.26 percent shares are held by Banks, DFIs and NBFIs. Modarabas and Mutual Funds account for 1.09 percent of the outstanding shares of ITTEFAQ. The remaining shares are held by other categories of shareholders.

Historical Performance (2018-22)

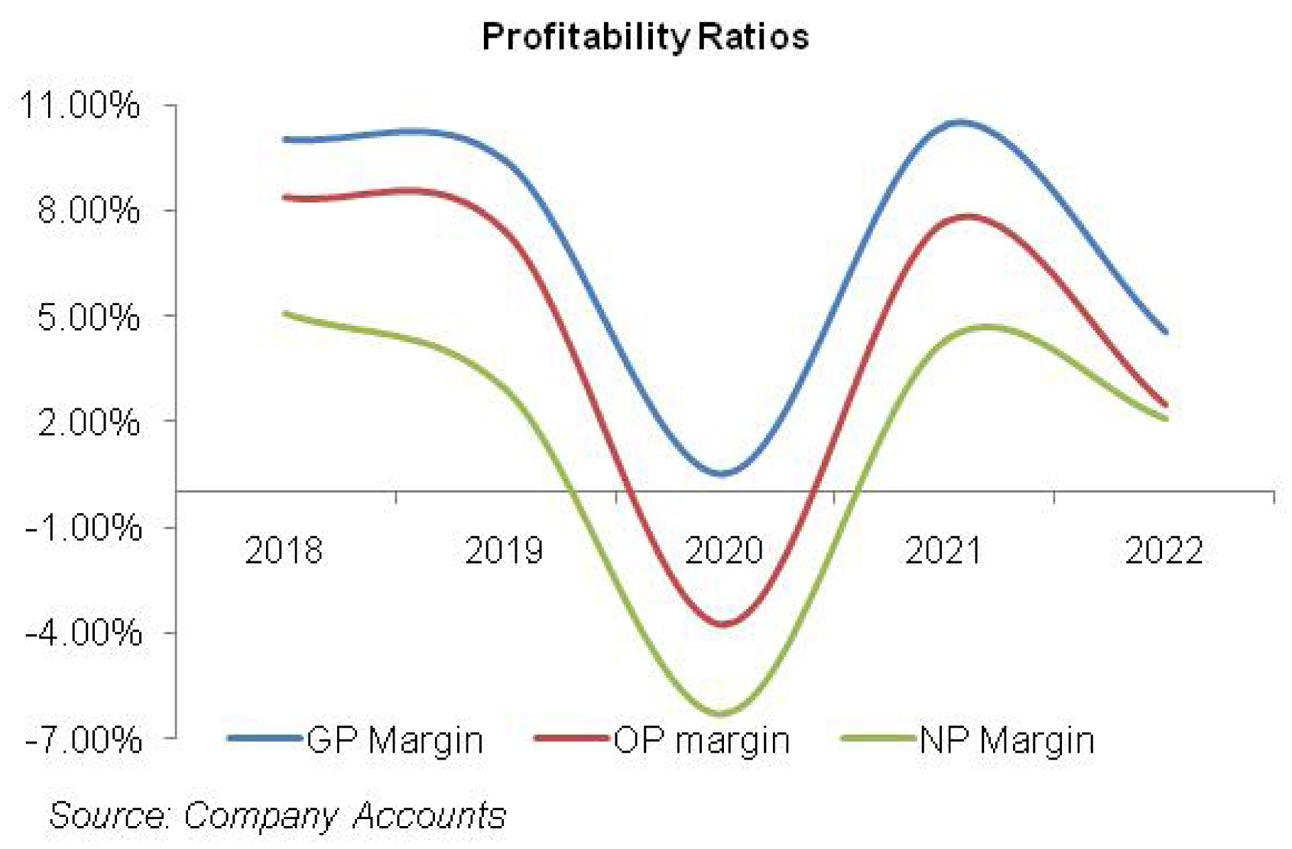

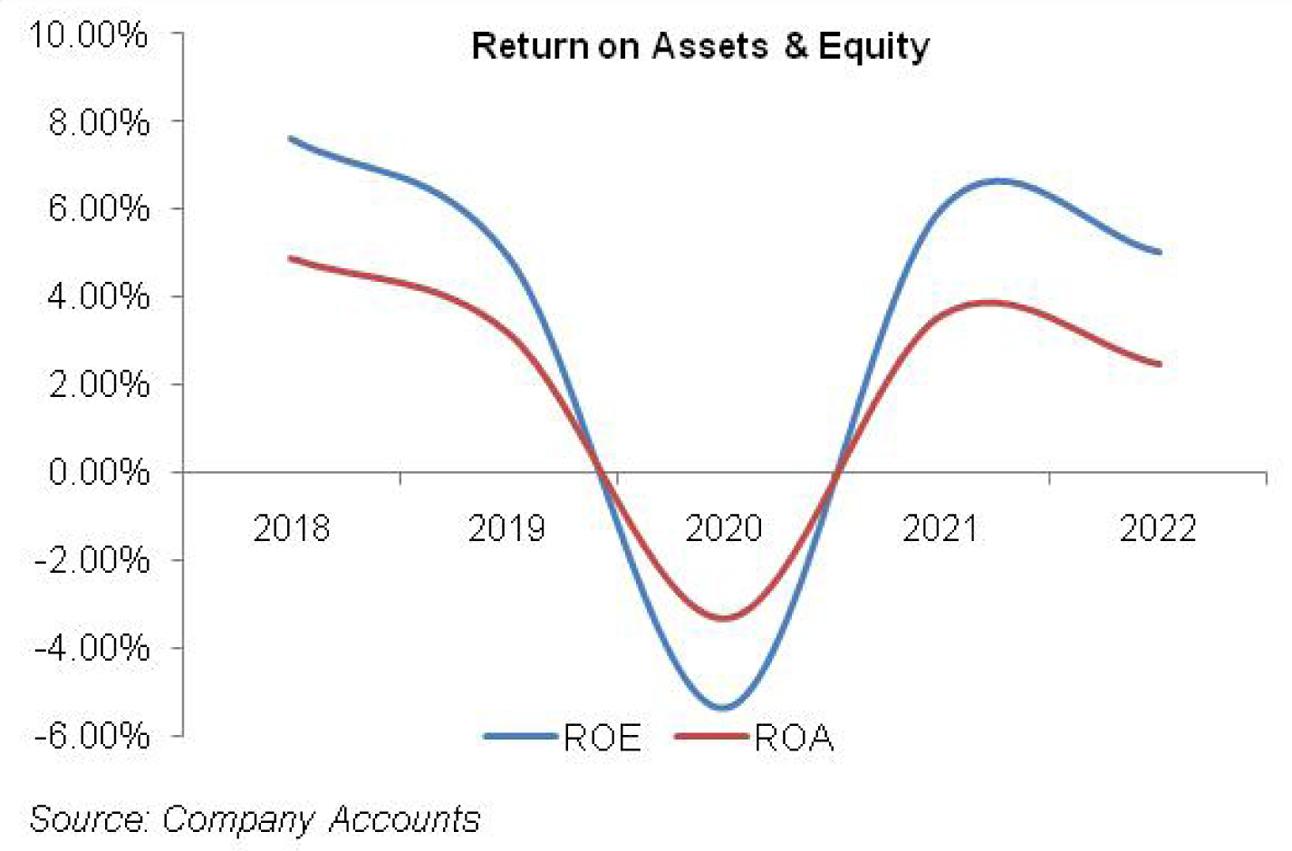

Since 2018, ITTEFAQ’s topline is making great strides except for a decline in 2020 where unlike the rest of the years, the company also posted a net loss. ITTEFAQ’s bottomline and margins which were tumbling until 2020, significantly rebounded in 2021 only to get hit hard again in 2022. The detailed performance review of each of the years under consideration is given below.

In 2019, ITTEFAQ’s topline posted a 10 percent year-on-year rise. The company had an installed capacity of 120,000 M T for the rolling mill and 160,000 for the structural mill. During 2019, ITTEFAQ achieved 62 percent of its rolling mill capacity and 23 percent of its structural mill capacity versus 67 percent and 0 percent capacity utilization achieved in the previous year. This was in line with the market demand during the year which was greatly suppressed on account of political instability, steep hike in policy rate, Pak Rupee depreciation and rising inflationary trend. This had put the industrial and infrastructure development activity in the country on a standstill, resulting in tamed demand of steel. Due to the similar reasons quoted above, the cost of ITTEFAQ’s sales grew by 11 percent year-on-year. This , although, resulted in a 3 percent year-on-year growth in gross profit, however, GP margin fell from 10 percent in 2018 to 9.4 percent in 2019. Distribution expense massively grew to the tune of 51 percent in 2019 which was the result of extensive advertising undertaken during the year. Higher rebates and commission as well as payroll expense also contributed to an overall growth in distribution expense in 2019. 54 percent spike in administrative expense came on account of increased human resource headcount during 2019 as new furnace and re-modification rolling was plant installed during the year. Lower provisioning for WWF and WPPF culminated into a 21 percent year-on-year plunge in other expense in 2019. Other income also slipped by 25 percent year-on-year in 2019 on account of lower return on deposit accounts/. Operating profit declined by 3 percent year-on-year in 2019 with OP margin nose-diving to 7.4 percent from 8.4 percent in 2018. Finance cost grew by 77 percent year-on-year in 2019 on account of high discount rate coupled with increased borrowings. However, increase in the company’s equity due to 13.12 million bonus shares issued at the end of the year resulted in a dip in debt-to-equity ratio from 51 percent in 2018 to 38 percent in 2019. ITTEFAQ’s bottomline posted a 37 percent year-on-year slash in 2019 to clock in at Rs.198.19 million with an NP margin of 2.9 percent versus 5.1 percent in 2018. EPS also dropped from Rs.2.17 in 2018 to Rs.1.37 in 2019.

In 2020, ITTEFAQ’s net sales crashed by 50 percent year-on-year as the local as well as global economies were jolted by COVID-19. A massive cut in government spending on PSDP coupled with lackluster LSM activity contributed to subdued steel turnover in 2020. Widespread lockdowns imposed during the year coupled with tamed demand translated into a fall in ITTEFAQ’s capacity utilization of rolling mill as well as structure and melting mill to 28 percent and 18 percent respectively. Cost of sales dropped by 45 percent, translating into a 97 percent lower gross profit recorded by the company in 2020. GP margin drastically fell to 0.5 percent in 2020. Excessive advertisement didn’t let the distribution expense show any respite in 2020 which grew by 62 percent year-on-year in 2020. Conversely, administrative expense slumped by 11 percent year-on-year in 2020 due to lesser payroll expense incurred during the year. Zero provisioning for WWF and WPPF resulted in a 1 percent dip in other expense. Other expense would have been even lower has the company not booked the provision worth Rs.23.98 million in 2020 against doubtful debts owing to deteriorating business fundamentals amid COVID-19. Other income slid by 29 percent year-on-year in 2020 due to high based effect owing to the gain earned on the disposal of property, plant and equipment in 2019. The company posted an operating loss of Rs.128.03 million in 2020. Finance cost dwindled by 80 percent year-on-year in 2020 due to lower long-term borrowings and also because the discount rate started sliding down in the last quarter of FY20. ITTEFAQ posted a net loss of Rs.212.81 million in 2020 with a loss per share of Rs.1.47.

ITTEFAQ closed 2021 with a staggering 83 percent year-on-year growth in its topline. The company’s rolling mill plant operated at 46 percent capacity in 2021 to produce 64,708 MT while melting and structure mill operated at 58.8 percent capacity to produce 65,102 MT. The demand recovery was the result of the comprehensive project for the construction industry announced by the government coupled with higher PSDP spending. Furthermore, the initiation of Diamer Bhasha dam during the year also buttressed the demand of steel products during the year. Despite 65 percent cost hike on account of increase in the prices of scrap in the international market, higher demand as well as upward revision in steel prices resulted in 36 times bigger gross profit recorded in 2021 with GP margin jumping up at 10.4 percent. Increased sales volume meant higher packing as well as handling and carriage charges, culminating into a 29 percent year-on-year hike in distribution expense in 2021. Administrative expense inched up by 6 percent year-on-year mainly due to higher payroll expense incurred during the year. While the company booked considerably lower provision against doubtful debt in 2021 due to improved economic backdrop, higher provisioning against WWF and WPPF pushed other expense up by 46 percent year-on-year in 2021. Other income also posted a significant 151 percent rise in 2021, however still stays at 0.15 percent of ITTEFAQ’s net sales. Unlike last year, ITTEFAQ was able to post an operating profit in 2021 with OP margin of 7.7 percent. Finance cost slid by 4 percent year-on-year due to monetary easing. The company recorded a net profit of Rs.266.76 million in 2021 with an NP margin of 4.3 percent and an EPS of Rs. 1.85.

ITTEFAQ’s net sales posted 81 percent year-on-year growth in 2022 on the back of improved steel prices coupled with higher sales volume. The company operated its rolling mill plant at 50.5 percent capacity and melting plant at 58 percent resulting in the production volume of 70,735 MT and 75,545 MT respectively in 2022. However, 93 percent higher cost of sales on account of inflated prices of scrap in the international market, significant reduction in the value of Pak Rupee, steep hike in energy and fuel prices pushed the gross profit down by 21 percent year-on-year in 2022. GP margin slumped to 4.5 percent in 2022. Higher advertisement and packing material charges resulted in a 28 percent spike in distribution charges in 2022. Administrative expense inched up by 16 percent year-on-year in 2022 which was in line with inflation despite reduced man power. Service cost worth Rs.45.672 million incurred during the year pushed the other expense up by 82 percent year-on-year in 2022 despite a drop in provisioning against WWF and WPPF during the year. Higher return on bank deposits also translated into an 11 percent year-on-year rise in other income in 2022. High cost of sales and operating expense drove the operating profit down by 42 percent year-on-year in 2022 with OP margin slithering to 2.5 percent. Finance cost grew by 50 percent year-on-year due to excessive monetary tightening during the year. This pushed the net profit down by 12 percent year-on-year to clock in at Rs.234.05 million in 2022 with an EPS of Rs.1.62 and an NP margin of 2.1 percent.

Recent Performance (9MFY23)

Lackluster LSM growth as well as overall economic activity kept steel demand under extreme pressure during FY23. This resulted in a 19 percent year-on-year decline in ITTEFAQ’s net sales during 9MFY23. Cost of sales also slid, however, with a lower magnitude of 14 percent year-on-year. This resulted in a 94 percent slippage in gross profit during 9MFY23 with GP margin falling from 6.1 percent in 9MFY22 to just 0.4 percent in 9MFY23. Lower sales volume resulted in a 5 percent lesser distribution charges incurred during 9MFY23 versus the same period last year. Conversely, administrative expense succumbed to inflationary pressure and grew by19 percent year-on-year in 9MFY23. Other expense registered a 34 percent year-on-year plunge which might be due to lower provisioning done against WWF and WPPF in 9MFY23. Other income also tumbled by 3 percent year-on-year in 9MFY23. ITTEFAQ made an operating loss of Rs. 141.74 million in 9MFY23 as against an operating profit of Rs.356 million during the similar period last year. Despite high discount rate, the company was able to cut back on its finance cost by 51 percent which could be the result of reduced borrowings during the period. However, drop in finance cost was offset by hefty increase in taxation expense. ITTEFAQ registered a net loss of Rs.245.45 million during 9MFY23 as against a net profit of Rs.226.17 million during the same period last year. Loss per share stood at Rs. 1.70 during 9MFY23.

Future Outlook

The coming years appear to be rough for the steel industry due to negative impact of flash floods of 2022 on the GDP growth, acute political instability, high cost of doing business due to unprecedented levels of inflation and discount rate and Pak Rupee depreciation, not to forget the steel hike in energy fuel prices and government taxes. While there are many projects of CPEC in the pipeline coupled with Ravi Riverfront urban development project, however, no progress will be achieved unless the political dust settles.

Comments

Comments are closed for this article.