Askari Bank Limited (PSX: AKBL) was incorporated as a public limited company in Pakistan in 1991. The parent company of AKBL is Fauji Foundation. The bank offers conventional, corporate, Islamic, consumer, and agricultural banking services through its wide network of 560 branches and sub-branches across the country.

Pattern of Shareholding

As at December 2021, AKBL has an outstanding share capital of 1260 million shares which are held by 14,471 shareholders. Associated companies and related parties are the largest shareholders of AKBL with a representation of over 73 percent in its share capital. This is followed by the general public holding 18.85 percent shares of AKBL. Modarba and Mutual funds have a stake of 2.41 percent in AKBL followed by Insurance companies owning 1.96 percent shares. The remaining shares are held by other categories of shareholders.

Financial Performance (2018-2022)

The topline of AKBL has by and large been growing since 2018, however, in 2021; it showed a marginal growth of 0.3 percent. While gross advances and investments grew by 21 percent and 37 percent respectively during the year, we can safely assume that the subdued topline growth was the result of discount rate cuts during the year to help the economy recover from the shocks of COVID-19. Discount rate slash also justify the growth of gross spread ratio which stood at around 42 percent in 2021 as against 39 percent in 2020 despite a significant 28 percent year-on-year growth in deposits in 2021. It is to be noted that the CASA ratio of the bank dropped from 87 percent in 2020 to 79.69 percent in 2021. The contribution of non-fund-based income dropped from 24.5 percent of total income in 2020 to 22.74 percent mainly on the back of income on securities which dropped by 68 percent year-on-year in 2021. The massive plunge in income on securities shadowed the tremendous growth on fee and commission, dividend income and foreign exchange income and resulted in 3 percent year-on-year dip in the total non-markup income. Then the bank booked massive provisions during the year which grew by 152 percent year-on-year. While this was a prudent approach as its non-performing loan portfolio grew by 8 percent year-on-year on the back of widespread economic uncertainty post COVID-19. However, this didn’t bode well for the bottomline and resulted into a year-on-year drop of 11 percent in its net profit in 2021.

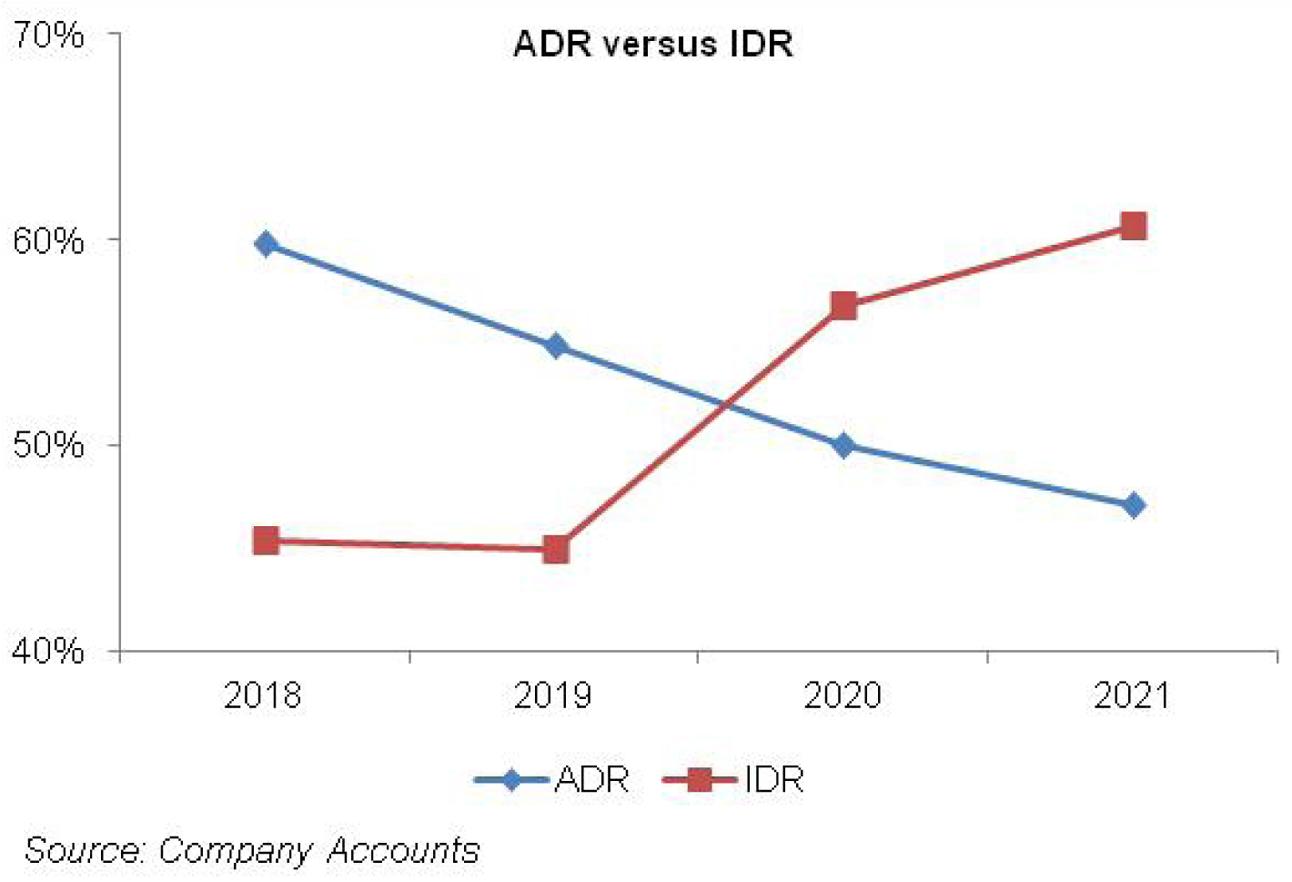

It is to be noted that the bank has been continuously slashing its Advances-to-Deposit Ratio (ADR) since 2018 which clocked in at 47 percent in 2021 as against 59.8 percent in 2018. In this way, the bank has been able to keep a check on its infection ratio which stood at 6.3 percent in 2021 as against 7.7 percent in 2018. AKBL has maintained a coverage ratio of above 90 percent in all the years which shows that the bank has done enough provisioning for its bad debt portfolio. The coverage ratio of AKBL stood at 97 percent in 2021.

The bank has been maintaining a healthy CASA ratio which is above the similar sized peers in the industry which is the reason of its net interest income riding an upward trajectory since 2019. Non-markup income also fairly contributes to the bottomline with non-markup income to total income ratio hovering above 22 percent in all the years under consideration. AKBL has significantly reduced its cost-to-income ratio from 66 percent in 2018 to 51 percent in 2021 despite branch network optimization and implementation of additional provincial levy during 2021.

With multiple hikes in discount rate during the year, the topline of AKBL presented a tremendous growth of 114 percent during 2022. However, with minimum deposit rate imposed on the saving deposits, the topline growth couldn’t translate into a healthy NII. Gross spread ratio of AKBL dropped to 24 percent in 2022 from 42 percent in 2021. While the detailed financial statements of 2022 have not been published by the bank, the historical evidence shows that while the bank enjoyed healthy CASA, the current accounts always remained under 30 percent of its total deposits. This is where the bank took the hit when MDR was imposed on the saving accounts. As of September 30, 2022, Current deposits account for 29 percent of AKBL’s total deposits. During 2022, the bank made tremendous foreign exchange income which grew by 76 percent year-on-year; however, a loss of Rs.251 million on the securities resulted in non-markup income to remain stagnant as a proportion of total income. The cost-to-income ratio of AKBL further improved to 45 percent in 2022. Moreover, there was a marked drop in provision during the year. The nine monthly statements of AKBL show that the infection ratio is further improved to 5.4 percent with coverage ratio clocking in at 98.7 percent. Despite higher effective tax rate due to the imposition of super tax coupled with higher taxation on government securities for having an ADR under 50 percent, the bank was able to post a 45 percent year-on-year growth in its bottomline during 2020.

Future Outlook

Banking sector is a key beneficiary in the prevailing monetary tightening scenario, however, in order to optimize the benefit of high discount rate, AKBL must focus on mustering low-cost current accounts which stood at a mere 29 percent as of September 30, 2022. Moreover, with inevitable excessive income tax levy imposed in the Finance Budget, AKBL can evade higher taxation on government securities by overhauling its asset portfolio and increase its ADR which stood at 49 percent as of September 30, 2022. However, with an ongoing economic downturn and low borrowing appetite from private sector, how AKBL will enhance its advances portfolio while keeping a check on its non-performing loans is yet to be seen.

Comments

Comments are closed for this article.