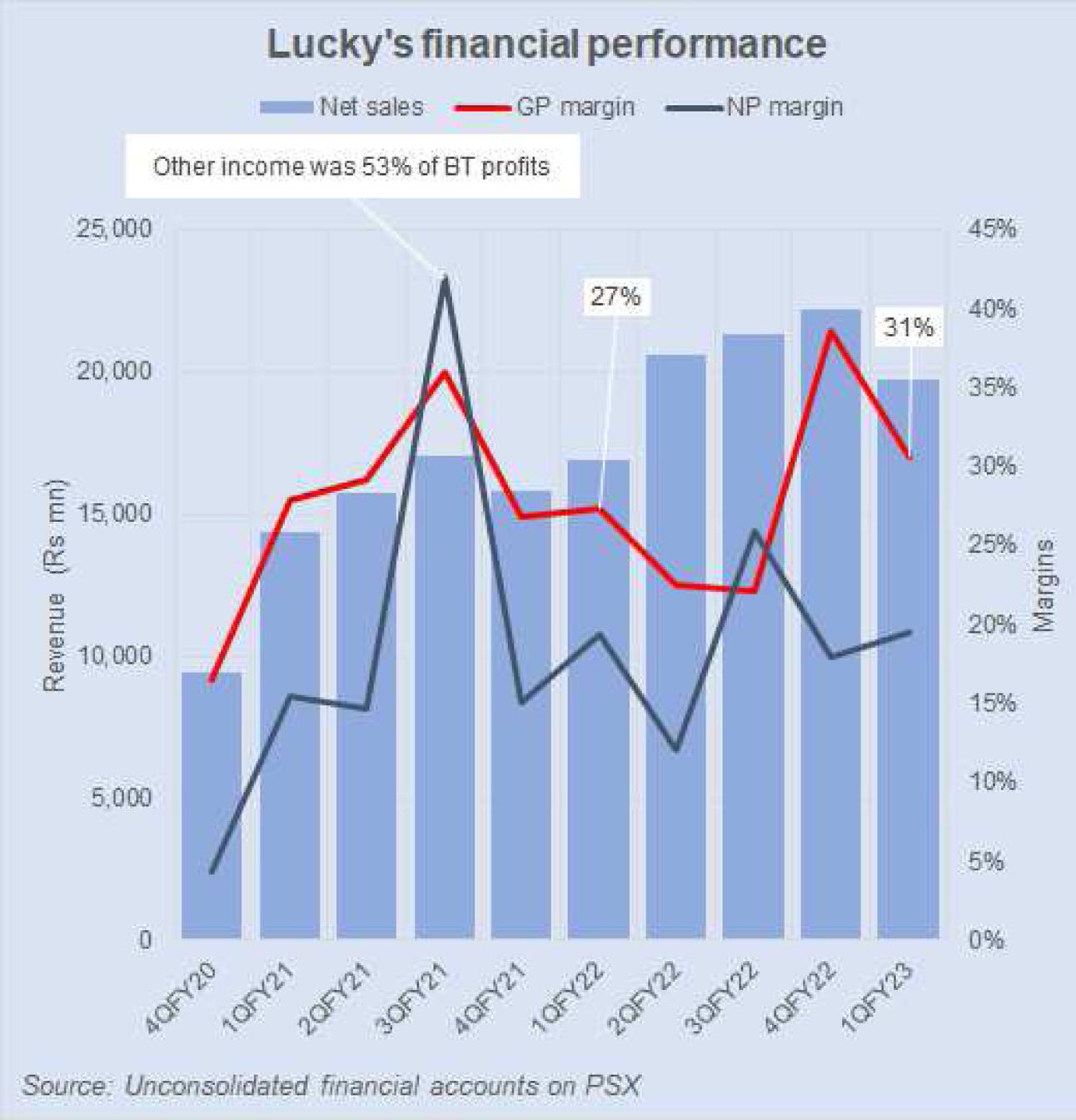

Typically, a 30 percent decline in off take would be troubling for any company looking to make a decent earning but that company is not Lucky Cement (PSX: LUCK). In 1QFY23 in fact, Lucky not only saw volumes shrink by 30 percent, higher than the industry wide decline in sales of 25 percent but also experienced a slight shift in market share—down from 17.6 percent to 16.4 percent. Despite that, both the top-line and the bottom-line delivered a positive performance where revenue and post-tax profits grew 17 percent year on year.

Strong retention prices helped. Estimated revenue per ton sold for the company surged 67 percent which is significant. Though costs of production have been growing as fossil fuel and coal markets internationally have been witnessed prices shooting up. Amid that, cement manufacturers have been using a combination of international coal with Afghan and local coal in the mix (most companies located in the North zone have replaced 70-90% of their coal usage with Afghan or domestically sourced coal). This has cushioned the blow to the margins bypassing much of the coal frenzy being experienced world over. Lucky has been using Afghan and local coal at its northern plants and South African or Indonesian coal at the southern plant.

The coal mix together with prudent inventory management helped margins improve compared to the same period last year standing at 31 percent in 1QFY23 compared to 27 percent previously. Costs per ton sold for the company during period has grown 60 percent; lower than the increase in revenue per ton sold.

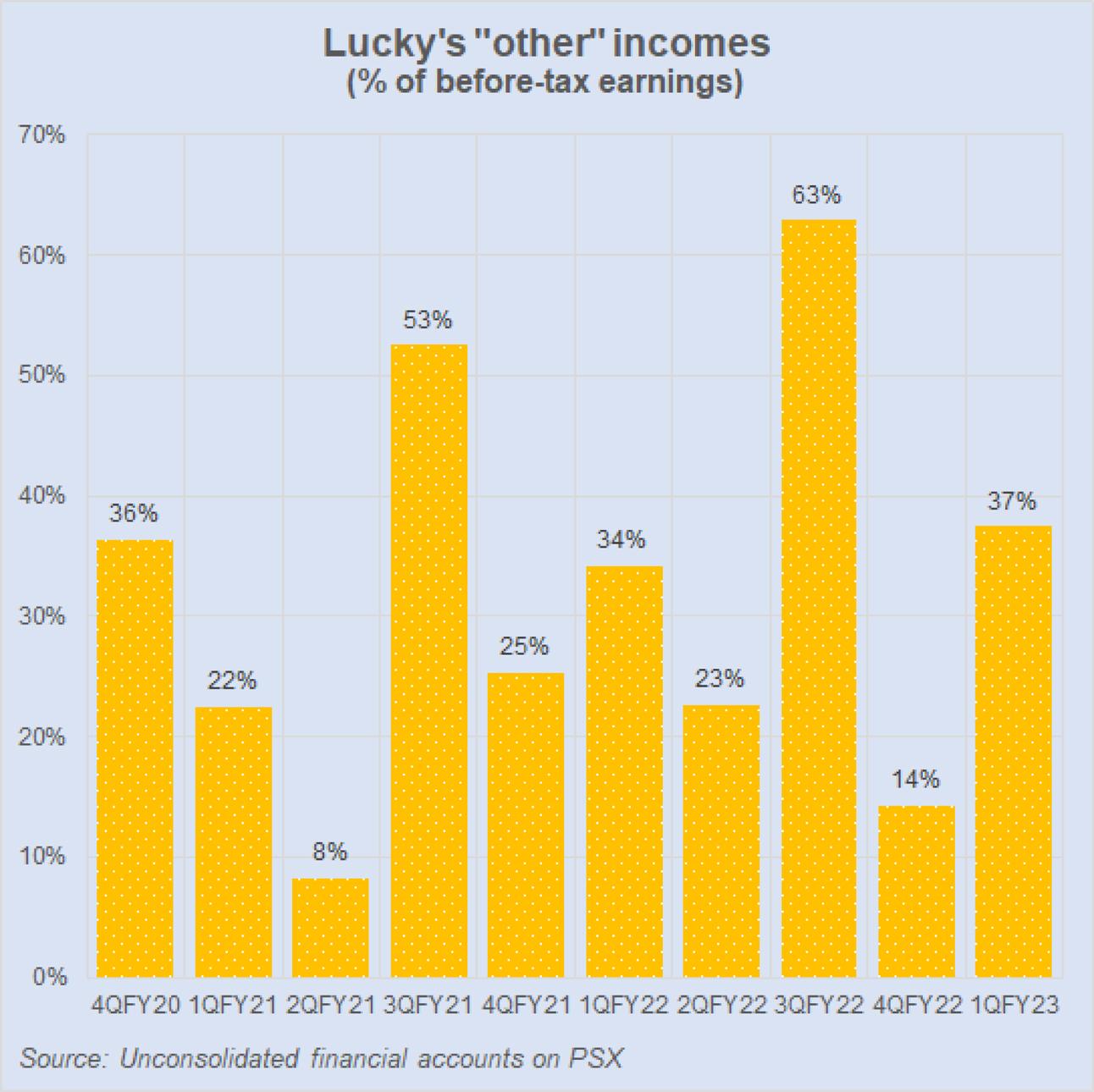

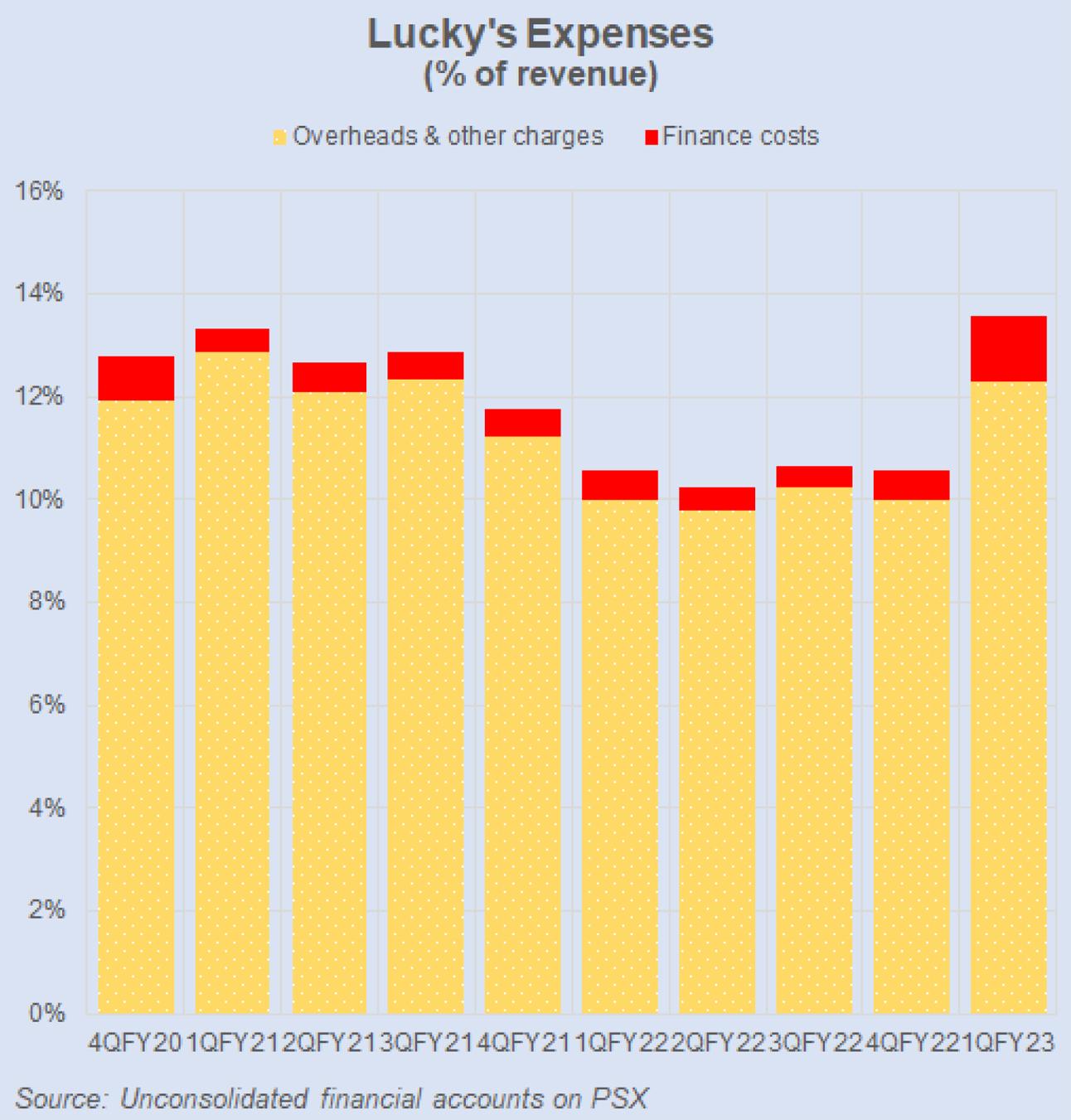

Though overheads and other charges grew to 12 percent (1QFY22: 10%) of revenue, finance costs have not budged much staying at only 1 percent of revenue. These factors together led to an earnings growth of 17 percent year on year. Even though the effective tax this quarter was higher than last year, net margins improved to 20 percent versus 19 percent in 1QFY22. A big portion of the before-tax earnings—about 37 percent—came from the “other income” component.

The company is expected demand to remain low, expected to decline by 10 percent during this year though management believes some incremental demand could be fetched due to flood-related rehabilitation. Expected rebuilding and reconstruction associated to floods to begin quite so soon would be unwise.

Even as demand lull will likely continue, Lucky expansion plans will come through by the end of the calendar year which will be joined with other expansions. By the end of the fiscal year—if there are no delays—cement industry capacity will grow by another 10-15 million tons. This is a large capacity coming online in an economy that is turning off the steam engines. Nevertheless, the company seems positive that there won’t be any price wars as demand post-floods will improve, pushing the market to absorb the growing capacity. Given the precarious macroeconomic climate—with inflation still running amok—demand recovery will be crucial for continually glowing financial performance for cement manufacturers.

Comments

Comments are closed for this article.