Maple Leaf Cement Factory Limited (PSX: MLCF) was established as a public limited company in 1960. It is part of the Kohinoor Maple Leaf Group. Kohinoor Textile Mills Limited is its holding company that holds over 55 percent stakes.

Shareholding pattern

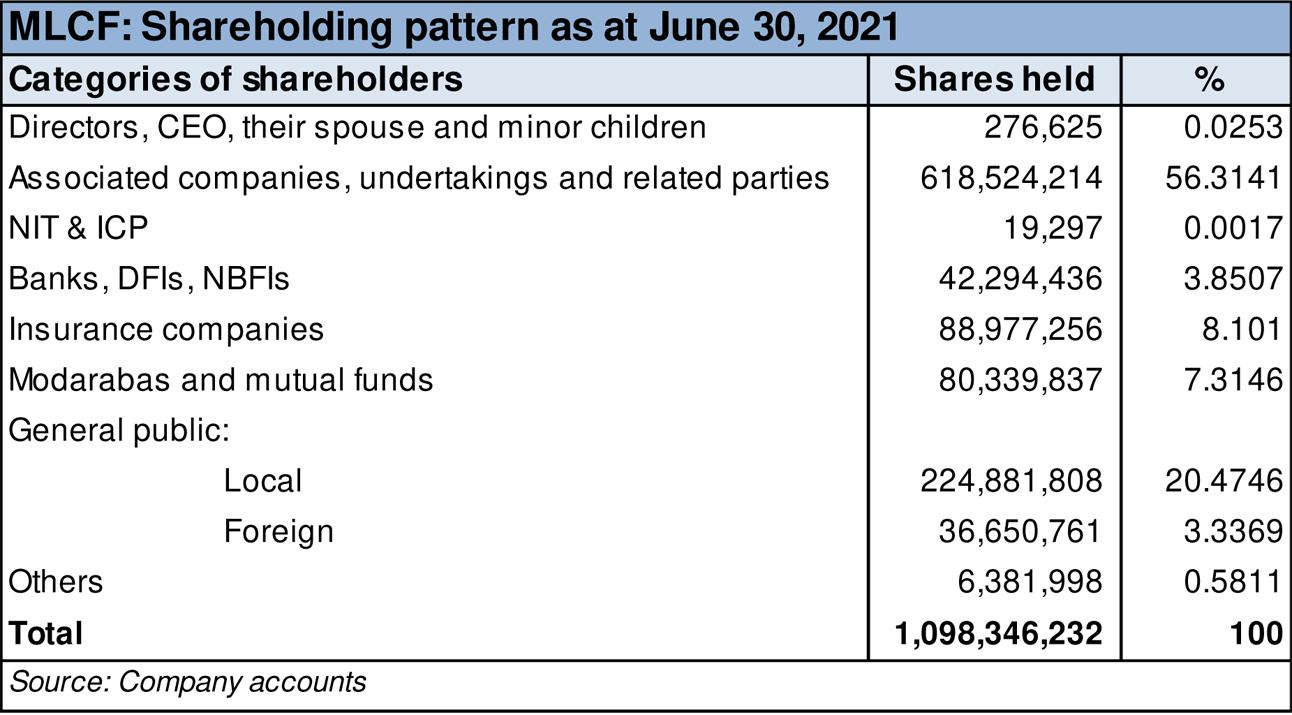

As at June 30, 2021, over 56 percent shares are held under the associated companies, undertakings and related parties. Of this, 55 percent are owned by Kohinoor Textile Mills Limited. The local general public owns close to 20.5 percent shares, followed by 8 percent in insurance companies. Over 7 percent shares are held in modarabas and mutual funds, while the directors, CEO, their spouses and minor children own less than 1 percent share. The remaining close to 8 percent shares is with the rest of the shareholder categories.

Historical operational performance

The company has consistently seen a growing topline over the years where as profit margins have followed a declining trend until FY20, after reaching a peak in FY16. In FY21, profitability witnessed a sharp incline.

In FY18, revenue grew by 7 percent to cross Rs 25 billion. Local dispatches grew by almost 19 percent to 3,487,492 metric tons, while export sales continued to decline. In addition to facing low margins on export sales, the latter was also discouraged by barriers by other countries such as anti-dumping duties by South Africa and non-tariff barriers in India. However, the higher topline did not translate into a higher gross margin as cost of production consumed nearly 73 percent of revenue, compared to 60.5 percent in FY17. The increase was attributed to packing materials, fuel expense and power and associated costs. The effect also reflected in the net margin that was lower at 14 percent compared to nearly 20 percent in the previous year.

Revenue growth in FY19 was marginal at 1 percent to reach Rs 26 billion. Local dispatches fell by 4.3 percent due to lower private sector spending as well as political uncertainty as the year began with general elections. On the other hand, export sales volumes registered a growth of 21 percent to reach 334,671 tons. This was attributed to slower business activity in the local economy and currency devaluation that encouraged exports. Because margins are lower on export sales due to intense competition, this reflected in the gross margin that fell to 18.9 percent. In addition to an escalation in cost of production, finance expense also grew to consume 4.5 percent of revenue, thus reducing net margin to 5.6 percent.

At nearly 12 percent in FY20 the company witnessed the highest revenue growth seen since FY17. Topline crossed Rs 29 billion in value terms. Sales’ volumes increased by nearly 42 percent to 5,201,820 metric tons while local dispatches saw a more than 50 percent rise. This was a result of the start of a new production line. On the other hand, there was a downward pressure on prices as supply exceeded demand. In addition to this, rupee devaluation raised coal prices that increased production cost. Unable to cover costs, the company incurred a gross loss of Rs 699 million for the first time. With operating expenses incurred and finance expense escalating to consume over 10 percent of revenue, net loss was recorded at Rs 4.8 billion.

The company witnessed an all-time high revenue growth of over 22 percent in FY21 with topline crossing Rs 35 billion. This was attributed to an improvement in selling prices in the local market. Moreover, some export markets also opened up as reflected in increased export volumes to 327,404 metric tons. Thus, gross margin improved to 21 percent for the year. There was a marginal change in operating expenses, while other income increased sharply to Rs 3.7 billion, providing significant support to the bottomline that was recorded at an all-time high of over Rs 6 billion. Net margin was also higher year on year at 17.5 percent. The unusually higher other income was largely generated from dividend income from subsidiary company.

Quarterly results and future outlook

Revenue in the first quarter of FY22 was higher by nearly 32 percent year on year. This was again attributed to higher selling prices. However, volumes have been lower due to same level of demand in the local market, while the export sales were adversely impacted by the political situation on Afghanistan. Despite the inflationary pressure and currency devaluation, the company was able to curtail costs as it utilised cost-effective pet coke and earlier purchases of materials that were sourced at cheaper rates. Thus, net margin for 1QFY22 stood at 5.7 percent versus 4.1 percent in 1QFY21.

Revenue in the second quarter was again higher year on year, by almost 35 percent. This was again due to selling prices adjusted for inflation. Volumes on the other hand have been impacted by slow implementation of large scale projects, and high production cost in the country that render the product unfeasible in the international market. However, profitability was higher year on year as the company used high energy content pet coke, as well as the competition of the Waste Heat Recovery Project of 9MW that made one-third of the power mix. The third quarter also saw almost 27 percent higher topline year on year due to rising selling prices. However, net margin was lower in 3QFY22 as 3QFY21 saw unprecedented rise in other income that normalised in the current period. With the ongoing uncertainty on the local and global front, cement demand is expected to remain stagnant while costs are expected to rise, particularly with supply of oil impacted due to Ukraine-Russia war.

Comments

Comments are closed for this article.