Karam Ceramics Limited (PSX: KCL) was set up as a public limited company in 1979. Before 1982, its name was “International Standard Ceramics Limited”. The company manufactures and sell tiles. It has tiles for indoor and outdoor as well as for bathroom flooring. Some of its clients are Saima Mall, Kidney Centre, Dolmen Mall, Bahria Town, Karachi and Model Town, Lahore.

Shareholding pattern

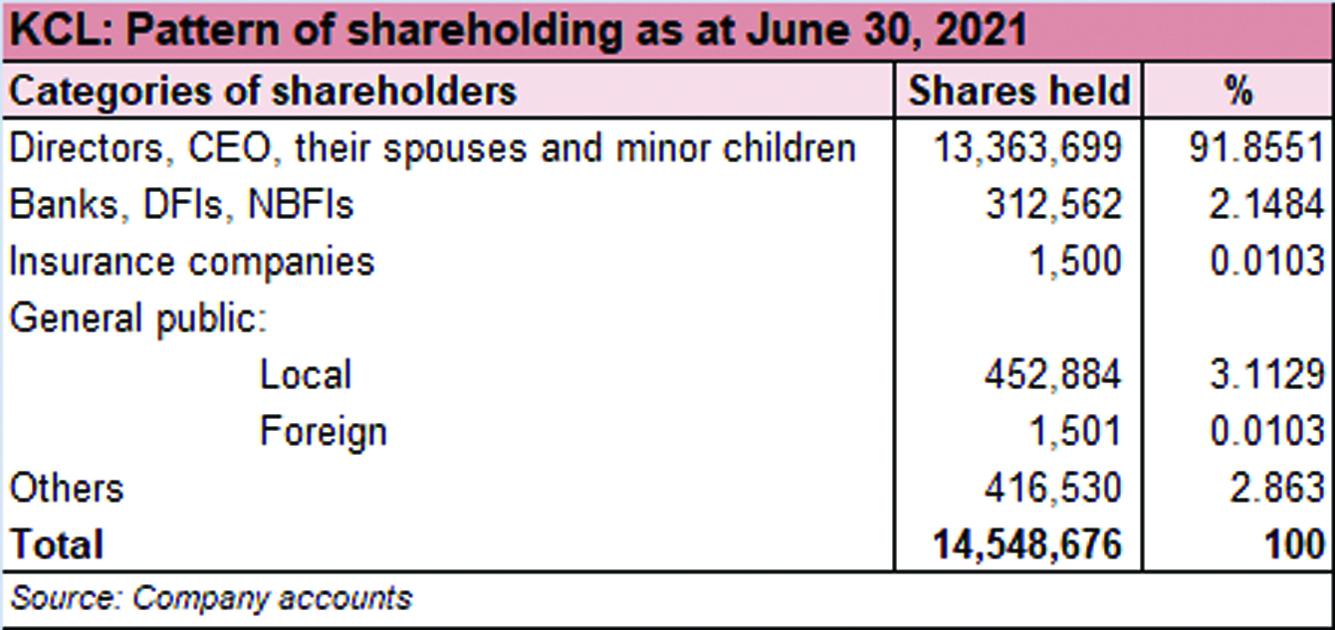

As at June 30, 2021, a major chunk of shares, about 92 percent, is held by the directors, CEO, their spouses and minor children. Within the category, over 13 percent shares are held by each of the following: Mr. Irshad Ali S. Kassim, the Vice Chairman and Mr. Munawar Ali S. Kassim, the CEO of the company. The local general public holds 3 percent shares followed by 2 percent held in banks, DFIs, and NBFIs. The remaining close to 3 percent shares is with the rest of the shareholder categories.

Historical operational performance

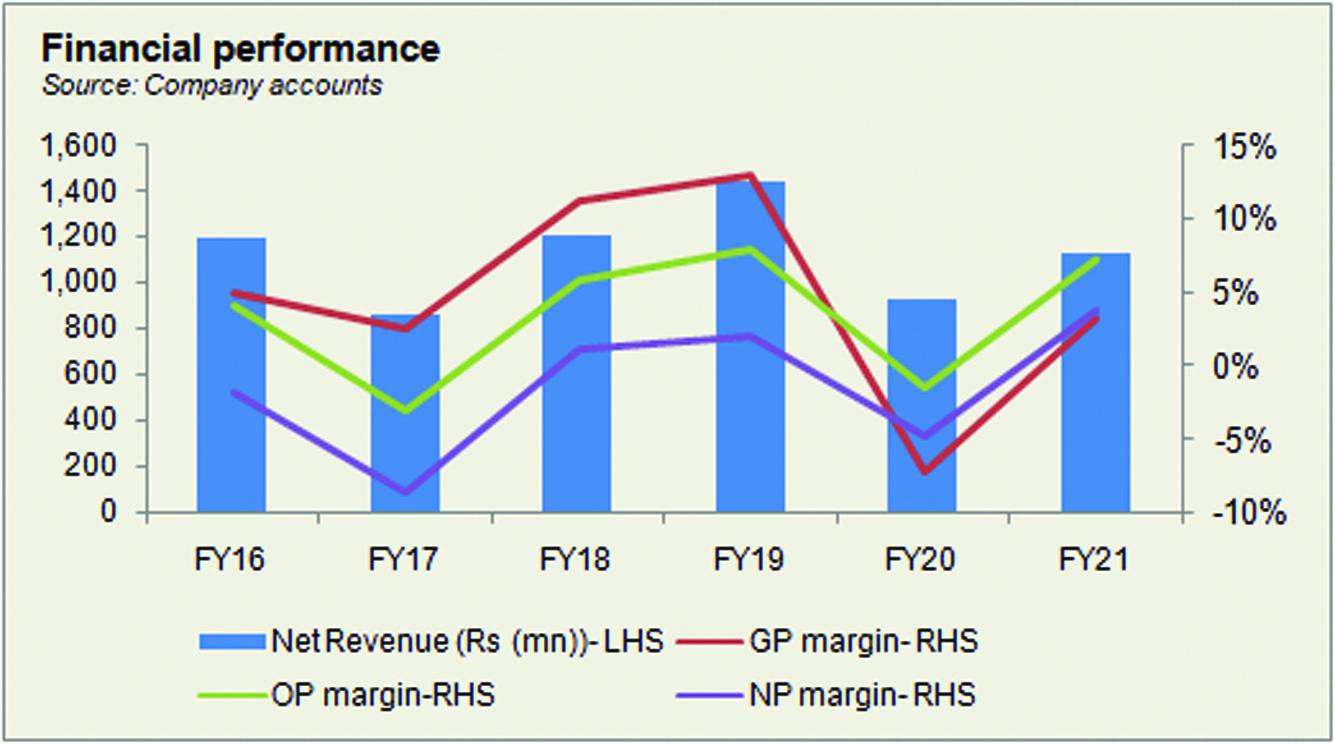

Karam Ceramics has witnessed a fluctuating topline over the years, while profit margins in the last six years increased between FY17 and FY19, declined in FY20, before improving again in FY21.

After declining for two consecutive years, revenue in FY18 grew by over 40 percent, to cross Rs 1 billion. This was attributed to an increase in volumes as well as price. Moreover, cost of production plunged to a below 90 percent mark, at nearly 89 percent, after six years. Therefore, gross margin increased to over 11 percent. With other costs also reducing as a share in revenue, operating and net margin also improved compared to previous two years specifically. After incurring losses for two consecutive periods, the company managed to post a profit of Rs 14 million for the year.

In FY19, revenue growth stood at almost 19 percent, again, attributed to an improvement in selling price and volumes. Cost of production fell further to 87 percent of revenue, thereby raising gross margin to 13 percent. With slight decreases in other elements too, the improvement in gross margin also trickled down to the bottomline that was recorded at Rs 29 million at a net margin of 2 percent. It is one of the highest net margins seen since FY10.

In FY20 the company faced the biggest contraction in revenue at over 35 percent, with topline falling below Rs 1 billion. This was attributed to the outbreak of the Covid-19 pandemic that resulted in a lock down. Karam Ceramics was able to resume operations by end of May 2020. However, since fixed costs are unavoidable, with the lost in revenue, the company was unable to cover its costs, therefore it incurred a gross loss for the first time of Rs 67 million. Some support was brought in by other income at Rs 90 million that was abnormally high. This came from “present value adjustment on modification of interest free loan from directors. However, with finance expense continuing to escalate due to higher interest rates, the company incurred the largest loss in a decade at Rs 44 million.

Revenue bounced back in FY21 as it grew by over 21 percent, with topline crossing Rs 1 billion. Although cost of production consumed almost 97 percent of revenue, it was lower in comparison to that seen last year. Thus, the company posted a gross margin of 3.2 percent. There was also some marginal reduction in other operating expenses as a share in revenue, while other income continued to post a higher-than-normal number, at Rs 80 million. This primarily came from a combination of “present value adjustment on modification of interest free loan from directors” and liabilities no longer payable. Coupled with this was a positive tax figure that allowed net margin to peak at 3.7 percent for the year.

Quarterly results and future outlook

Revenue in the first quarter of FY22 was higher by 33 percent as it was recorded at Rs 268 million compared to Rs 201 million in the same period last year. This was due to an improvement in prices and volumes. Production cost was also significantly lower as a share in revenue at 90 percent, versus 98 percent in 1QFY21. The resultant higher gross margin also trickled to the bottomline that was recorded at Rs 13 million compared to a net loss of Rs 26 million in 1QFY22.

With the announcement of construction package, construction activity in the country has increased substantially. Presently, this has created a demand for cement and steel but the company expects that eventually there will also be an inevitable demand for bathroom and tiles. Additionally, new players have also entered the industry that are operating in free trade zones and are thus entitled to tax benefits. On the other hand, for last decade or so, the industry has also faced competition from the presence of smuggled goods from Iran and dumped goods from China.

Comments

Comments are closed for this article.