Attock Petroleum Limited (PSX: APL) was Incorporated in 1998 an oil marketing company and is part of the Attock Oil Group of Companies. Its product portfolio consists of lubricants, commercial and industrial fuels; and it markets and supplies fuels to manufacturing industry, armed forces, power producers, government/semi-government entities, FMCG companies, developmental sector, and agricultural customers. APL has a strong retail network with over 700 retail outlets nationwide. Attock Oil Group of Companies is a fully vertically integrated oil and gas group including exploration, production, refining and marketing of a wide range of petroleum products. APL’s sponsor, Pharaon Investment Group Limited Holding s.a.l holds the largest shareholding at 34 percent, whereas other key shareholders include Attock Refinery, Pakistan Oilfields Limited, and Attock Oil Company as shown in the illustration.

Past performance

The oil marketing sector is a sector that is driven by the petroleum and oil demand in the country and that has largely been on an upward trajectory over the past decade despite the pandemic and sector up and down such a prices, liquidity challenges and the circular debt. Moreover, a lot has been going on in the sector in terms of changing consumption patterns; industrial and economic activity; petroleum product pricing mechanism in the country; government policies like furnace oil curtailment; power sector merit order etc.

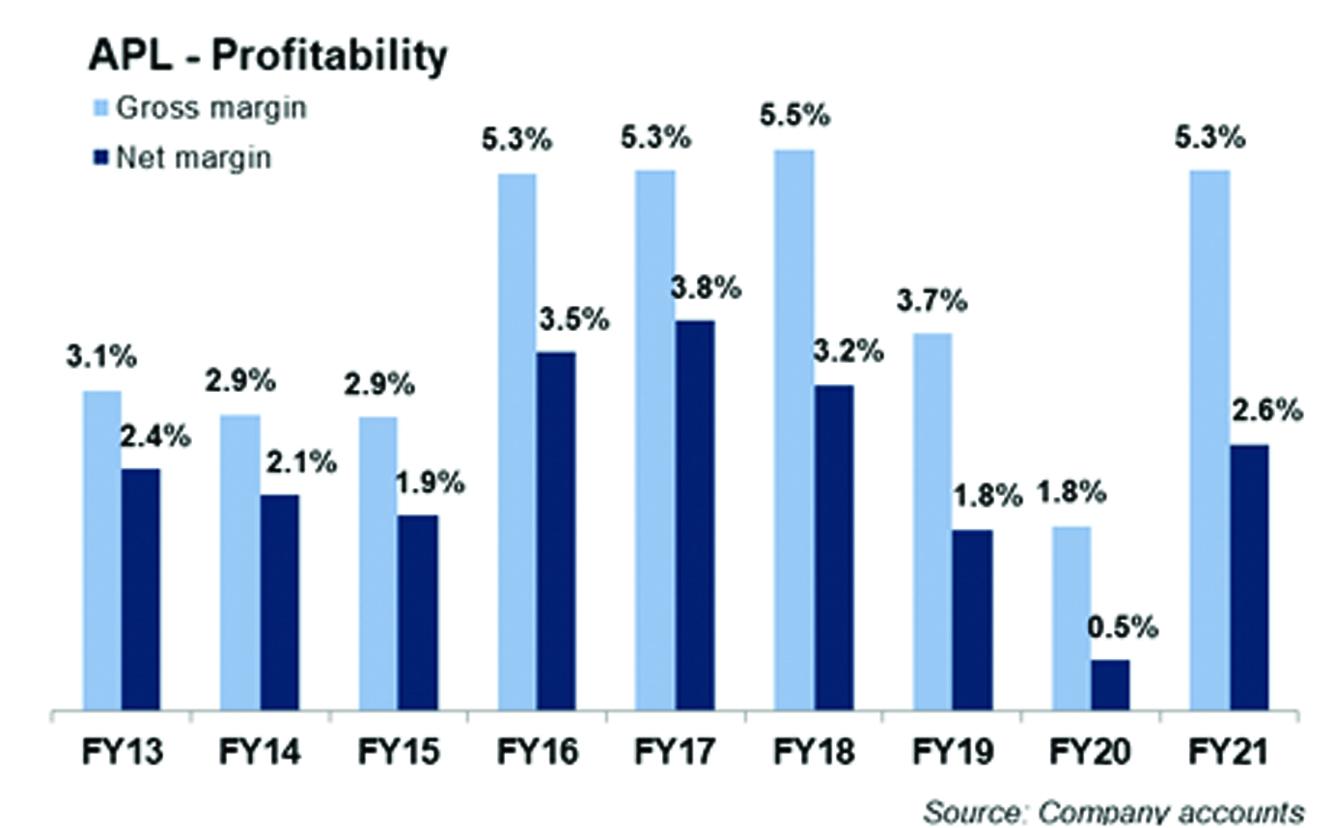

Continuing the volumetric growth, petroleum products and retail volumes sold by the OMCs resulted in higher sales revenues due to higher oil prices in FY16. However, Attock Petroleum Limited’s overall volumes were adversely affected by the phasing out of furnace oil. As a result, APL lost market share in attempt to reduce exposure in furnace oil due to unattractive margins.

On the other hand, revenue growth for APL was strong in FY17 due to growth in volumetric flows, diesel and petrol sales particularly which translated into a fat bottomline. Overall, APL’s earnings were up by 38 percent year-on-year.

APL continued its revenue growth in FY18 as petroleum prices remained high and volumes grew as well. Increase in sales volume and inventory gains due to rising price trend of petroleum products during the year resulted in higher gross margins. However, APL’s profits grew meagerly by seven percent year-on-year due to reversal of provision of other charges and higher exchange losses due significant currency depreciation during the year.

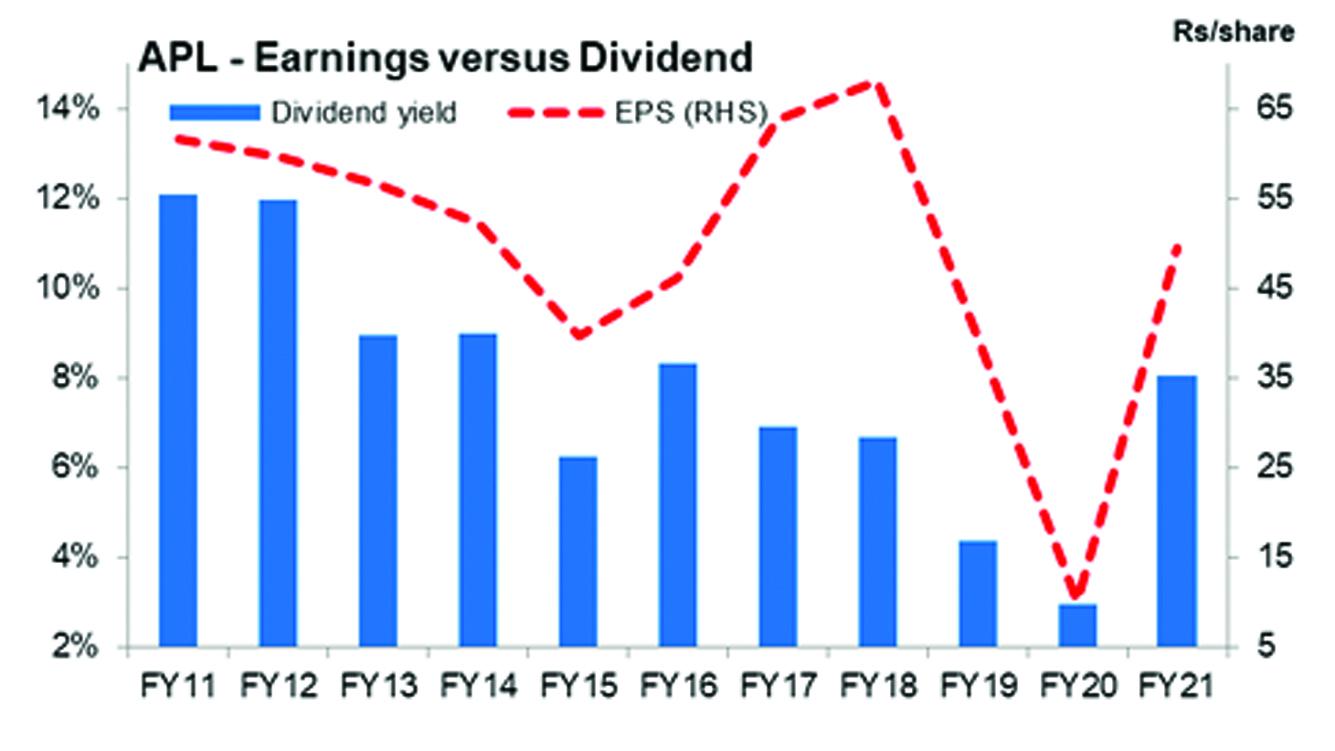

The pace slowed down in FY19 due to falling crude oil prices and domestic currency nosediving. Moreover, the effects of monetary and fiscal tightening adversely affected the OMC sector in FY19. Where the falling crude oil prices resulted in significant inventory losses for the OMCs, the depreciating rupee brought in large exchange losses. APL’s topline grew by around 26 percent year-on-year, which was entirely due to higher petroleum product prices, because voluemtric growth remained subdued in FY19. APL’s volumes declined by 11 percent year-on-year decline led by furnace oil and high speed diesel sales while earnings were down by 30 percent.

Things became further difficult in FY20 for many sectors including the OMCs largely due to demand destruction brought by the COVID pandemic. APL’s earnings too plummeted to only Rs1 billion. Weakness in earnings due to inventory losses from lower prices of petroleum products in the country versus international prices, along with decline in volumes were key inhibiting factors. During FY20, APL’s overall market share remained the same around 10.5 percent. However, its volumes sold registered a decline of around 11 percent year-on-year, which was highest for diesel followed by petrol and then furnace oil. Apart from the weakness in the topline and higher inventory losses, jump in finance cost amid high interest rates, relatively lower other income, decline in profits from associated further added to the bottomline decline.

FY21 saw a recovery fortunately after a shaky year FY20. The real deal in FY21 financial performance was the quarterly improvement in 4QFY21. After thrashing earnings to levels not seen in at least a decade, APL’s bottomline jumped by 4.9 times in FY21 where the 4QFY21 earnings surged by more than nine times. Though the overall topline growth remained subdued with a decline of 6 percent year-on-year, revenues for APL grew by 52 percent year-on-year in 4QFY21. The primary reason for growth in revenues was 20 percent increase in volumes in 4QFY21 led by furnace oil recovery in the fuel mix. At the same time, the oil price recovery after the international price crash in 2020 supported the revenue growth for the quarter.

APL’s gross margins grew staggeringly due to significant inventory gains against heavy inventory losses in the corresponding period. This was due to increase in oil prices as well as due to change in the domestic petroleum pricing format to fortnightly basis that reduced the volatility from the lag. The operating and net profits got a further boost from net impairment reversals on financial assets in FY21 as well as a decline in finance cost.

FY22 and beyond

The last quarter of FY21 as well as 1QFY22 have seen a revival in volumes for the OMC sector including APL with rebound in economic activity including car sales, industrial activity, and agriculture output. Along with continued restrictions on cross-border smuggling. APL volumes continued to churn growth as it entered FY22. Oil sales for Attock Petroleum Limited were up by 23 percent year-on-year during 1QFY22 led by the retail fuels, motor gasoline and high-speed diesel, as well as the furnace oil.

APL’s revenues during 1QFY22 were up by a massive 61 percent year-on-year due to higher petroleum product prices as well as higher volumetric sales. And while gross margins slipped slightly, the growth in gross profits of over 53 percent year-on-year also came from higher petroleum product prices in the shape of inventory gains - particularly of higher margin product, the furnace oil. Other operating expenses saw a jump in 1QFY22, which was offset by an increase in other income, decline in finance cost, and an impairment reversal on financial assets versus a loss during 1QFY22. Overall, APL’s bottomline grew by 61 percent year-on-year in 1QFY22.

APL is in a better position as the OMC was able to regain market share in all three key petroleum products.

Comments

Comments are closed for this article.