The country’s digital financial services segment seems to have endured the pandemic year rather well. The latest quarterly statistics on branchless banking (BB) released by the central bank provide numbers that are a cause for optimism for this channel to make further inroads during 2021 as normalcy gradually improves.

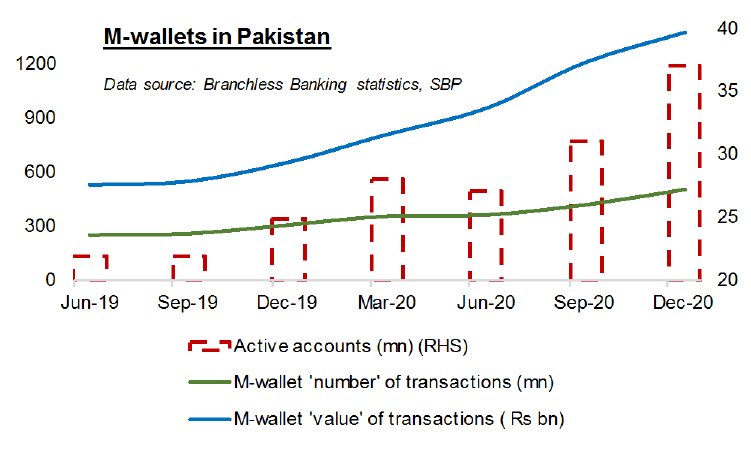

The SBP’s latest data show that the total number of BB accounts (also known as mobile wallets, or m-wallets, for short) stood at 62.7 million as of December 2020 end, up from 46.1 million accounts at 2019 close. This 36 percent annual growth in wallet uptake is impressive, considering the difficulties in on-boarding new users in a year marked by sporadic mobility restrictions as well as economic weakness.

However, the fact that 16 million+ new wallets were registered during the year only becomes a meaningful insight when there is an associated increase in “usage” of BB channels. In that regard, the concentration of “active accounts” among total accounts is a useful proxy, as are the trend in customer transaction performed via m-wallets compared to over-the-counter (OTC) channel.

The number of active accounts (which have been defined in the past by SBP as accounts that were either registered in the previous 180 days or accounts that performed at least one transaction in the previous 180 days) reached 37 million by December 2020 end, up from nearly 25 million active accounts as of 2019 end.

Despite the fact that the definition of active accounts seems rather lax (a 90-day period is perhaps more suited), the annual growth of 51 percent is significant. This expansion is also higher than annual growth in total accounts (36%), reflecting better activity levels in the system. Looked another way, at the end of 2020, 59 percent of m-wallets could be classified as “active”, up from 53 percent at the end of 2019.

In terms of payments, customers made 548 million transactions worth Rs1,476 billion in the Oct-Dec 2020 period, resulting in annual growth of 53 percent and 79 percent, respectively, over same period previous year. In other words, 6 million BB transactions were taking place per day day worth Rs2,693 towards 2020 end, higher than 4 million daily transactions with average ticket size of Rs2,300 around 2019 end.

The data also show that towards the end of 2020, most of the transaction flow was making its way via m-wallet channel compared to the OTC stream. In 4QCY20, for instance, 93 percent of customer transaction volume originated from m-wallets and accounted of 93 percent of the value pie. This is up from 86 percent of volume and 79 percent of value being generated from customer wallets back in 4QCY19.

The m-wallet dominance over OTC is deemed positive by stakeholders in Pakistan in the context of digitizing cash payments. Great, but it needs to be pointed out that the ability of folks to make virtual payments, especially at the bottom of pyramid, is enabled, in part, by the OTC channel. Thousands of BB agents, especially in remote places, play a crucial role in educating first-time or reluctant users to try this method to pay their bills or send/receive money.

To be sure, there is growth in number of BB agents, reaching ~0.5 million total agents and ~0.2 million active agents by 2020 end. But the OTC channel’s transaction volumes are slowly disappearing. Will this cast doubt on financial viability of these value-chain participants? This concern needs to be investigated, for without OTC, millions of financially-excluded people may be unable to find entry into formal financial system. And this could eventual hurt the uptake of m-wallet accounts after a certain point of saturation.

Comments

Comments are closed for this article.