Hinopak Motors (PSX: HINO) is in gross losses. At its financial year-end in Mar-20, HINO—which was a market leader in the commercial vehicle segment until recently when Isuzu took the top spot—recorded a gross loss of Rs170 million and a loss per share of Rs166.7. To blame this annual performance on Covid-19 would be unfair since, for all intents and purposes, the company saw a downtrend in sales long before the pandemic hit.

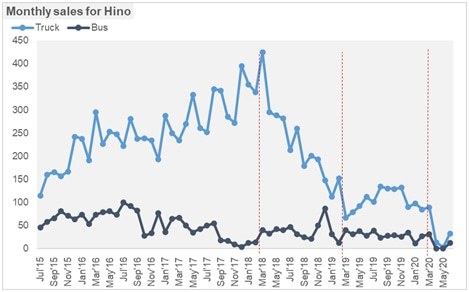

After surviving a grueling last year registering a net loss margin of 5 percent, this year has been far worse. Volumetrically, sales (for chassis, bus, bodies, and Hilux frames) fell 44 percent as demand for both light and heavy commercial vehicles dwindled—down to single-digit in monthly sales in the case of trucks beginning Dec-19. Evidently, the commercial vehicle segment has followed a sharp decline since 2018 when the economy had already started to burn out. The trajectory of sales since 2016 when the economy was fast-growing—and CPEC-related excitement was setting in—was upward, peaking in Mar-18. It was all downhill from there.

Commercial vehicles sales are a barometer for economic activity in the country –denoting boom or bust in trade, retail, commercial and construction sectors—which is why the slowdown in the segment came faster than other segments such as passenger cars and motorcycles which are based on individual incomes and slow to react to macroeconomic changes. Due to worsening economic conditions, any expansions the company was planning due to CPEC are on halt.

This year, better price points allowed the top-line to not trudge along the volumes route, as revenue per unit sold—on average—improved by 23 percent year on year. However, higher input costs did not help. In fact, costs per unit sold expanded by 32 percent. Being an importer of parts and kits, the company associates much of this increase on the depreciating rupee and poor rupee and yen parity against the dollar.

Higher overheads deepened the cut. The company saw increased administration and distribution expenses as a share of revenue (5% against 3.8% last year) while higher borrowing costs brought financial expenses to nearly 8 percent of revenues (last year: 5%). Naturally, with nearly 13 percent of revenues moving out on overheads and finance costs, the company’s net losses ballooned further. The loss in the outgoing year nearly doubled from the preceding year.

The coming year will be another whirlwind. The first three months so far have recorded minimal to no sales due to COVID-related lockdowns but volumes may start to improve as construction-related activity across the country will soon start to pick up. However, until the economy and trade really revive, demand may remain subdued which will keep chipping away at the topline.

Comments

Comments are closed for this article.