Mughal Iron and Steel Industries Limited (PSX: MUGHAL) was established in 2010 as a public limited company. It was formed after taking over a partnership concern by the name of “Mughal Steel”.

The company is present in the long-roll steel industry and engaged in other activities such as making billets, steel rebars, girders and t-iron. The company finds the utility of its products in the domestic housing market, both in urban and rural, alike, as well as large infrastructure projects market.

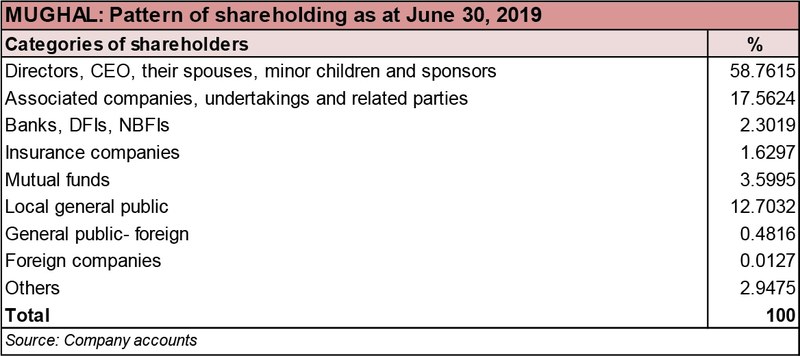

Shareholding pattern

The company is largely owned by the directors, the CEO, their spouses and minor children, with nearly 59 percent of the shares in their ownership. Of this, a little beyond 13 percent of the shares are held by Mr. Muhammad Mubeen Tariq Mughal, a director of the company. The next key shareholder are the associated companies, undertakings and related parties, holding 17.5 percent shares, followed by the local general public at almost 13 percent. The remaining about 10 percent shares are distributed with the rest of the categories.

Historical operational performance

Mughal Iron and Steel Industries has largely experienced positive growth in its timeline, except for FY17 when it saw marginal reduction. Profit margins have also been maintained, seeing two peaks; once in FY14 and once in FY18.

In FY15, the company’s topline doubled year on year, with a significant improvement in installed capacity as well as actual production for both melting and re-rolling. Most of this increase in revenue came from sales in the domestic market, driven by higher demand due to increase in construction activity in public and private sectors.

However, the higher revenue came at a higher cost; the latter consumed 89 percent of the revenue for the year. Distribution cost saw the most change, with salaries and freight and forwarding primarily driving this increase. Salaries expense increased from less than a million rupees to nearly Rs 4 million, whereas freight and forwarding grew to Rs 42 million, up from Rs 3 million in FY14. Thus, despite the rise in revenue, it could not be translated into better profit margins.

Revenue continued to increase during FY16 at 55 percent. Sales for steel bars, girders and t-iron increased in domestic market, while exports remained subdued. However, close to 90 percent of the revenue was consumed by cost of production. Apart from raw material expenses, fuel and power expense was the next major element that saw a rise. In addition to the problem of power shortage, the cost of electricity is also high. The company managed to control distribution and administrative costs, which allowed some improvement in operating profits; but they were offset by the higher taxation due to “first time recognition of deferred taxation”.

Mughal Iron and Steel industries saw a marginal decline in its revenue in FY17 by close to 1 percent. This was due to a completion of one-time sale order last year, which elevated previous years’ growth rates of topline. With the cost of production constant at 89 percent, there was a marginal change in operating profit margins. Net margin improved due to a reduction in finance charges; the latter occurred as a result of “elimination of notional interest on sponsor shareholders’ loan and decrease in exchange loss on deferred letters of credits”.

Growth in revenue was back on track in FY18 as it grew by 18 percent. This was attributed to better sales volumes as well as prices. Cost of production as a percentage of revenue also lowered to its lowest seen in a decade which allowed gross margins to improve. While other expenses increased in absolute terms, as a share in revenue there was negligible change allowing operating margins to improve as well. However, this could not be translated into a higher net margin as finance costs doubled due to higher working capital requirements, hence increase in average outstanding short-term loans.

The company saw yet another year of exorbitant growth in topline in FY19 at almost 39 percent. Given that the company and the sector overall benefits from public and private spending on infrastructure, and the fact that the government is focused on construction-led growth, the increase in revenue can be explained. Cost of production returned to its near 90 percent level, as a result of the inflationary pressure and average raw material consumption rates, reducing margins to their lowest seen in five years.

Quarterly results and future outlook

Mughal Iron and Steel Industries saw a marginal increase in its revenue year on year during 9MFY20. This was attributed to a fall in sales rate; in addition, sales were also affected in the third quarter due to the lock down imposed as a result of the outbreak of a pandemic. Cost of production also increased due to increase in raw material costs. Margins also reduced year on year due to an escalation in finance costs; the latter rose due to a rise in KIBOR rates in addition to increase in outstanding borrowings.

Sales volumes would be affected inevitably in the wake of the pandemic and a lock down which forced plants to be shut down. However, the company plans to manage cash flows smartly in order to continue catering to its customers.

Comments

Comments are closed for this article.