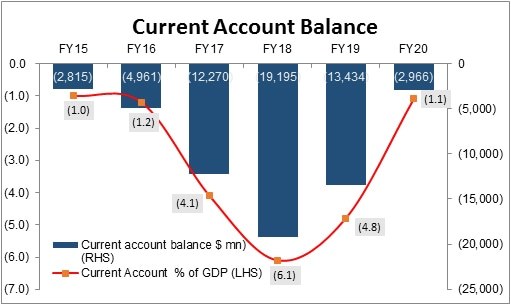

The current account deficit stood at $2.96 billion (1.1% of GDP) in FY20 –the lowest since FY15 in absolute and GDP terms. It was the need of the hour and tightening policies – higher interest rates and currency depreciation—resulted in reduced imports. In the last quarter, COVID helped CAD to ease further. Imports fell by 18 percent or $9.5 billion to $42.4 billion. Exports are down by 7 percent. Pre-COVID exports were up by 1 percent in 9MFY20.

Some people argue over the point of exchange rate adjustment when exports are stagnant. Well, the exchange rate (and interest rate) adjustments are imperative for curbing consumption (or imports); but not enough for boosting exports (or manufacturing). Policy stability and energy at competitive rates are necessary for promoting investment. The problem is that energy prices in Pakistan are linked to dollar (due to lopsided power producers’ contracts), and with currency depreciation, energy is becoming even more expensive. That is why, fixing the energy mess is a must to boost exports and substitute imports.

In given circumstances, SBP has two tools to control current account – exchange rate and interest rates. With interest rates down from 13.25 percent to 7 percent in no time, the demand is likely to boost. There are early signs of recovery. Imports are likely to pick in FY21, and that may put pressure on the current account deficit. That is why SBP may use exchange rate as an instrument to control. Any further monetary easing would put further pressure on currency. It is important to have a delicate balance. Further exchange rate adjustment will bring inflation home. It is better to use interest rate tool wisely. Further easing is not advisable.

The current account fall picked pace due to COVID. In Apr-Jun, the CAD stood at $282 million. The toll was $652 million and $540 million in the third and second quarter of the year respectively. The deficit in the first quarter was $1.5 billion. Thereafter, the impact of higher rates and currency adjustment started reflecting in the current account. Had there not been any COVID, the current account deficit for full year would have been in vicinity of $3-3.5 billion.

There is not much gain due to COVID to justify huge interest rate adjustment especially, when the foreign exchange reserves growth is stopped. The FX reserves of SBP were at $12.8 billion by first week of March. It touched the bottom of $9.9 billion in June before inching up to $12.1 billion. All the capital and financial inflows are from multilaterals. There are no market-based flows. How long can multilateral flows keep coming? How will the current account be financed next year? To attract foreign flows – higher rates or cheap currency are the options SBP has. As FDI needs policy stability and energy at competitive rates.

The imports in FY20 did not come down for free. Economic slowdown is the cost the country had to pay. In June, there is some surge in food and machinery imports. Power generation machinery imports and mobile phone imports went up significantly. Petroleum imports are up as compared to last month; but still much less than pre-COVID levels. Quantity imports (based on PBS data) in Jun-20 are at 90 percent of Jun-19; but in value the imports are almost half. Let’s see how long this low price sustains –one can safely say that these are inversely proportional to COVID cases.

The next jump in imports could come from the transport segment. The import in FY20 (on PBS) is down to half. There will be some increase in it. The demand for CKD imports would increase. Automobile sales are inversely proportional to lower interest rates. The demand may grow. At this point due to supply disruption, the assemblers are working at lower capacity. One leading player is operating on one shift as its number of its employees at any given point were in quarantine in the last month or so. They are now hiring new people, and will be on double shift soon. Others would have similar trajectory. This will inch up imports in this segment.

The story of exports is not too encouraging in the grand scheme of things. The good omen is that exports have recovered fast, and impact of COVID would be less on Pakistan as compared to countries like Bangladesh. The exports stood at $4.2 billion in Apr-Jun as compared to quarterly average of $6.1 billion in the first three quarters. Without COVID, exports would have been at previous year level of around $24 billion in FY20. The average $6 billion a quarter may come back soon. But beyond that, the growth would be slow without stable policies and competitive energy rates.

The decline in exports in last quarter is overall compensated by combination of fall in imports and increase in remittances. The surprise is in high remittances –especially in June at $2.4 billion. In Apr-June remittances stood at $6.1 billion versus $5.6 billion average in the previous three quarters. This is against many estimations. This section highlighted in April that remittances may remain resilient in 4QFY20 before falling. (For details read “Current Account outlook better – or it is?" published on 24th April 2020)

In a nutshell, the normalization of remittances may partially offset the expected increase in exports. Once the life returns to any semblance of normalcy (with fall in COVID cases) imports of goods and services will increase to put pressure on CAD.

Comments

Comments are closed for this article.