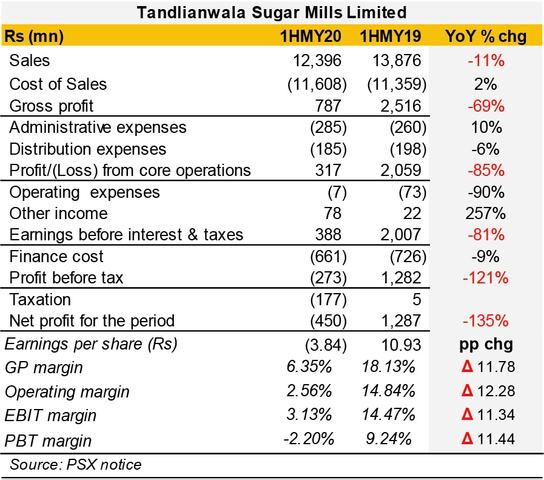

Last week, Punjab’s third largest listed sugar mill announced its half yearly accounts on the bourse. These are no ordinary times for the milling industry, and not just due to Covid-19. Milling operations in the province are under severe public scrutiny, as the industry deals with the fallout of the Sugar Inquiry Commission.

Although TSML managed to skirt the forensic inquisition, the six-month financial snapshot reads like an appeal for innocence on industry’s behalf. Despite the longest ever bull run for domestic retail prices, the company has taken a heavy beating on all indicators of profitability. Margins dropped by a whopping 11 percentage points across the board, as year-on-year top line also witnessed trimming by the same extent.

What happened? Several explanations, all of which lead to same line of causation: shortage of raw material, sugarcane. For over six months now, industry representatives have attributed the upward spiral in retail sugar prices to shortage of cane that led to crop trading at a 21 percent premium over government notified rate. So far as the sugar segment is concerned, the industry’s stated position is that it is an extremely low margin business, made worse by suspension of export policy.

Yet, units with economies of scale in the past have salvaged their profitability by raking in profits from the value-added segments, namely distillery and top gas. While ethanol has historically constituted less than a quarter of net revenue for TSML, its contribution margin has averaged over 50 percent. Except shortfall in cane availability led to even weaker supply of molasses, a crushing by-product used as raw material for ethanol production.

As a result, the capital-intensive division saw its segment sales contract by over 42 percent year-on-year, leading to a segment gross loss, a first in recent memory. In turn, top gas - which utilizes by-products of ethanol distillery – also continued to post losses (although its contribution to both topline and profitability is marginal). Meanwhile, higher cost of sugarcane also trimmed down margins in the sugar segment, partially mitigated by exchange gain recorded on export proceeds realization.

Yet, the real mystery is the failure of revenue from domestic sugar sale to take off, despite the increase in retail price by close to one-third (during 1H-MY20 compared to same period last year). Remember, the accounts cover the mostly pre-Covid period of Sep-2019 to March-2020.

Historically, sugar sales are seasonal and peak during summers and Ramzan/Eid season – both of which coincided with Covid-led lockdown. That does not bode well for domestic sales during 2H-MY20. Industry insiders have already hinted frequently that monthly consumption is down by 10 percent, which may lead to high carryover inventory before next crushing season. Come December, is the industry eyeing another round of export quota?

Comments

Comments are closed for this article.