As per the International Monetary Fund Report (IMF), there are only four (4) countries in the world where the interest paid on public debt is more than 7.5 percent of the Gross Domestic Product (GDP). In Pakistan the ratio is 7.71 percent. Others are Egypt with 9.8 percent, Brazil with 8.5 percent and Sri Lanka with 7.80 percent.

Except Brazil, which repaid USD15 billion of IMF debt in 2015, the other two are under the IMF programmes. Furthermore, Sri Lanka and Ghana are included in the list of countries which have defaulted in foreign and domestic debt.

This statement simply means that debt servicing has become alarming.

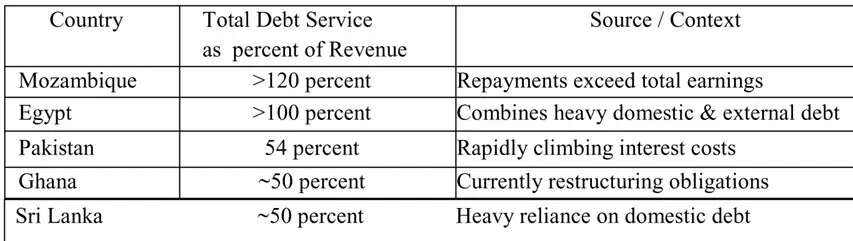

The position of the relevant countries is as under:

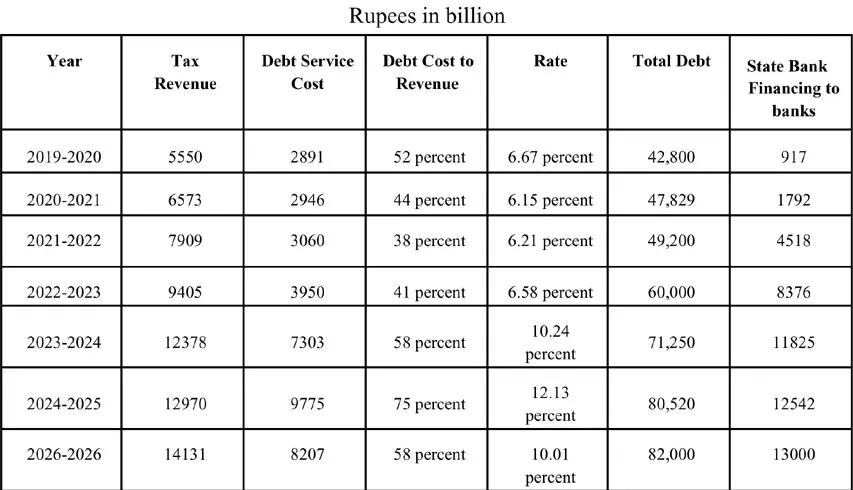

The table of total tax revenue, debt servicing cost, total debt and relevant percentages is as under:

The second table demonstrates that Pakistan is hit by two simultaneous shocks. Firstly, there is constantly increasing debt which almost doubled in five years from 42,800 billion to 82,000 billion in 2026. Each year we add on average Rs 4000 to 5000 billion to national debt. And secondly, the rate on such debt has increased from an average of below 6.5 percent to around 10 percent. The discount rate, which was being reduced correctly, will again increase the interest cost; therefore, in the forthcoming budget, the cost of interest servicing may again reach the level of around 60 percent of revenue. The table further reflects that out of the total debt a major portion of around 50 percent is financed by the commercial banks (given in table below) and for that the funds are made available by the State Bank of Pakistan.

The funds made available by the State Bank of Pakistan carry interest which represent income for the Federal Government as non-tax revenue. This means that these financial arrangements have nothing to do with the common man of Pakistan. Even a common sense economics does not recognise these arrangements.

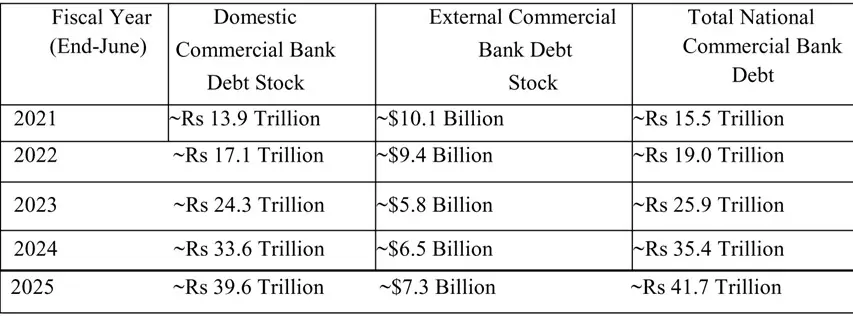

The total national public debt outstanding from commercial banks skyrocketed over this 5-year period due to structural deficits and a complete shift away from borrowing directly from the central bank (SBP).

As per the latest report of March 2026 of UNCTAD, the rising cost of debt is squeezing development prospects in many developing countries. Rising borrowing costs are leaving developing countries with less money for public spending, as debt servicing absorbs a growing share of government revenues. In many cases, mounting liquidity pressures risk turning into deeper crises. During 2018–2024, ninety nine (99) developing countries lost fiscal space. Pakistan is amongst 4 (four) top scorers.

For much of the past decade, developing countries have been paying more and more to borrow, leaving less money for schools, hospitals, climate action and other critical public investments. The consequences are now visible in public finances: higher interest bills mean governments have less resources for other priorities. In the favourable global financial environment that followed the global financial crisis, many countries increasingly turned to private credit. Though abundant and relatively affordable at the time, this funding left countries more exposed to external shocks. From 2022, the tide turned sharply as central banks in developed countries raised their policy interest rates to tame inflation at home. These benchmark rates influence the cost of borrowing worldwide – especially for debt from private investors and commercial banks, but also from official lenders such as multilateral development banks. As a result, borrowing costs across the developing world climbed markedly. This is duly reflected in the rate of interest of Pakistan’s debt in the last five years.

Higher borrowing costs have also weakened debt sustainability – the ability of governments to manage and repay debt – increasing the risk of severe economic strain. In September 2025, 49 percent of countries eligible for concessional financing from the International Monetary Fund (IMF) were either in or at high risk of debt distress. In many cases, these challenges reflect liquidity problems rather than outright insolvency. In other words, governments often struggle to meet short-term payment obligations even though their debts might still be manageable over the longer term. Yet containing such pressures is increasingly difficult.

Weak growth and trade prospects as well as limited access to the global financial safety net – emergency lending mechanisms provided by, for example, regional financial arrangements or institutions such as the IMF – restrict the ability of many countries to stabilize their finances. Pakistan is an example. Liquidity squeezes can therefore harden into deeper crises. Three quarters of the countries judged by the IMF and the World Bank to be in debt distress or at high risk of it in September 2025 had been in that position since at least 2018. In effect, many governments are being forced to default not formally on their debts but on their development ambitions. For example, Dow Medical College and King Edwards Medical College were established by colonizers. There is no example in the public sector, especially after 2000. Now our middle-class has to pay the fees desired by the private sector with the institutions run by the private sector.

In Pakistan, expenditure on law and order, health, education and other amenities, which are provincial subjects, have been firewalled against this increasing debt servicing cost deducting a pre-determined share of Provinces at 57.5 percent of the total Federal Tax revenue by way of Clause (3A) of Article 160 of the Constitution of Pakistan. This means that expenditure on health, education and other public amenities is not affected by increasing interest service. This is theoretically correct; however, the primary question is whether or not this ‘deemed’ divorce/ separation between two actors really firewalls the negative effect of increasing debt service cost in Pakistan. The answer to this question is in the negative for various reasons, which are given in the following paragraphs.

Despite substantial increase in the share of total revenue in $ terms the share of provinces in 2026 is still $ 28 billion when the tax collection is Rs 14,000 billion against Rs 7,909 billion in 2020-2021 on account of devaluation of rupee against $. This means that there is effectively no increase in spending on people despite doubling of tax collection in the past five years. This clearly shows that this deemed immunity is not there. Increasing inflation and fixed costs, majority being salaries, effectively absorb over 70 percent of total utilization of funds on public benefits by the provinces. Consequently, there is nothing left for development.

Out of the total taxes collected in 2021-2022, 62 percent were direct tax collection. These are now 51 percent on face of it. However, if the data is properly thrashed out the effective direct taxes remain above 60 percent of total revenues. These exclude charges like Petroleum Levy, which are not the part of divisible pool.

The problem in Pakistan is bigger than what has been demonstrated above. When the tax collection was Rs 7909 billion the tax rate on companies was 29 percent, which was an exceptional increase from 25 percent as the desired rate. In 2026, the rate of tax on companies is 39 percent. Similarly, the sales tax rate increased from 15 to 18 percent over the years. The purpose of demonstrating this rate change is to reflect the fact that the increase in tax collection from Rs 7,909 billion to Rs 14,000 billion is effectively on account of inflation and increase in tax rates. There is effectively no increase in tax base to provide space for equitably managing the tax burden.

In summary, there is an effective stagnation in the fiscal account for the last five years and the country is entering into a bigger and deeper debt trap and fiscal crises.

Unlike the general perception there is no IMF prescription and recommendation for medium- and long-term improvement. But the time has come to accept that Pakistan’s fiscal system cannot continue to operate in the present framework/scenario.

In this perspective there is news of fundamental changes in the NFC Award for allocation between Federation and Provinces. The author has his views on the same; however, that is not the subject of this article. The problem is deeper and broader than the measures which can be adopted by tinkering with the basis of the NFC Award.

The primary problem is whether Pakistan with a population growth of over 2.5 percent can sustain this model and formula of economic management. Let us admit that ‘Q’ Block has no answer. The answer lies in settling the broader national consensus by taking up the fundamental socio-politico-economic issues of Pakistan.

Copyright Business Recorder, 2026

Comments