Pakistan’s UAE exposure is being read too narrowly. The immediate focus has been on the $3.5 billion repayment to Abu Dhabi, and understandably so. It is large, visible, and lands directly on the reserves story. But the deposit may prove just the tip of the iceberg.

The larger vulnerability that lies in the wider UAE corridor: first through remittances, and then through the many less visible ways in which Dubai has become embedded in Pakistan’s labour market, services economy, commercial intermediation, and external financing comfort.

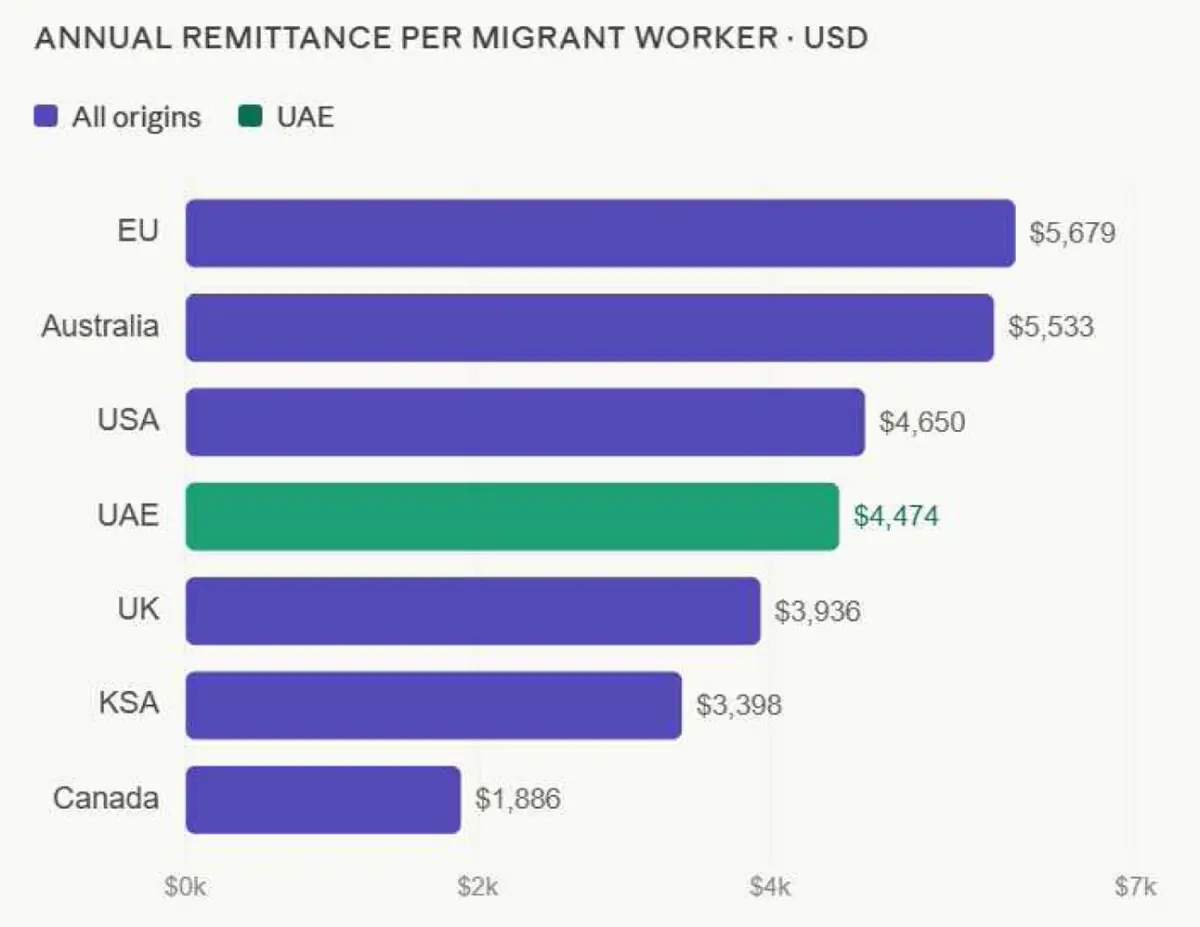

Start with remittances. The UAE is one of Pakistan’s largest remittance corridors, with annual inflows exceeding $8 billion that are more than twice the size of the current deposit repayment headline of just $3.5 billion. That alone should shift the analytical frame. A one-off repayment hits the stock of reserves. A deterioration in remittance flows hits the recurring external cushion. For an economy such as Pakistan’s, the latter is the more serious risk.

That risk should also not be overstated in the wrong direction. In all likelihood, it will not be a story of sudden repatriation of Pakistan origin workers.

However, the more plausible path is slower, and therefore easier to underread: weaker annual intake of new migrants, tighter scrutiny, more friction in approvals, and a gradual narrowing of labour-market access at the margin. That kind of shift may not produce one dramatic headline, but can produce a serious blow through cumulative pressure due to our overdependence on migrant flows.

Even that is only the visible part of the problem. The deeper exposure sits in the many quasi-formal ways in which Dubai has become integrated with Pakistan’s economy.

Over time, it has evolved from being merely a destination for labour and trade into a commercial wrapper for a growing layer of Pakistan-based activity. Freelancers, consultants, agencies, tech firms, small exporters, online sellers, and logistics intermediaries increasingly use Dubai entities to contract, invoice, bank, and hold working balances, even as much of the underlying work, payroll, and spending remain in Pakistan. In that sense, a part of Pakistan’s UAE-linked economic activity is real without being fully visible in the official numbers.

This is where the real vulnerability lies. A deterioration in access does not need to come through one formal policy action to have serious consequences. It can emerge through friction such as greater caution by banks.

More questions around shell structures; increased compliance burdens, and greater hesitation in client onboarding. Over time, this may lead to more difficulty in operating free-zone entities, and scrutiny of flows that previously moved with ease. Some of these channels may be predictable, but many are not. That is precisely the problem with depending on an external commercial ecosystem that was never fully institutionalized in the first place.

The damage often appears first in the form of inconvenience, not prohibition. By the time it becomes visible in the macro numbers, the underlying ecosystem will have already started contracting.

This is where the issue stops being a UAE story and becomes a Pakistan model story. Over time, Dubai has not merely served as a destination for Pakistani labour or a transit point for trade. It has become a workaround for Pakistan’s own weaknesses. When firms do not trust domestic tax administration, banking convenience, contract enforcement, regulatory consistency, or even the optics of operating directly from Pakistan, they used Dubai as an intermediary layer. That made commercial sense at the level of the firm.

But at the level of the economy, it created a silent dependency. A part of Pakistan’s services credibility, external earnings capacity, and urban economic activity came to rest on an ecosystem outside Pakistan’s own legal and economic architecture.

That is why the coming UAE shock should not be read simply as only a remittance risk, a reserve risk, or a labour-market risk. It could prove to be all of those.

More importantly, it is a dependency shock. It reveals how much of Pakistan’s external resilience has been built not on domestic reform, but on bilateral comfort, migrant absorption abroad, offshore commercial wrappers, and various forms of geopolitical rent. That model can survive for a while, but it can no longer be mistaken for strength.

Moreover, the immediate consequence of any weakening in the UAE channel is not greater diversification. It is greater concentration. As one external pillar becomes less reliable, Pakistan will have to lean even harder on another.

In practical terms, that means more dependence on other Gulf partners. That may provide short-term relief through deposits, deferred oil, or other bilateral support. But it deepens the same structural weakness.

The country moves from one concentration risk to another and calls it stability. It is anything but. In reality, it is rollover economics dressed up as strategic partnership.

That, in turn, raises the obvious but rarely stated question: what happens if tomorrow other partners makean ask Pakistan cannot comfortably meet? States do not operate on sentiment, nor should they. There are no permanent friends in international relations.

The problem begins only when a country’s external account, currency stability, fiscal balance, and even parts of its domestic economic activity become so dependent on bilateral goodwill that a deterioration in one relationship can rapidly alter the economic equation at home.

That is the real lesson of the UAE shock. It is not a lesson that bilateral relationships do not matter; they do. The lesson is that diplomacy cannot substitute for structural reform. Pakistan has repeatedly used external comfort to postpone domestic correction.

One year it is remittances; another deposits; deferred oil, or even geopolitical relevance. Each time, the same mistake follows: temporary cushioning is treated as if it were a solution to a structural problem.

A country that relies on another’s labour market to absorb its excess workforce, another’s free zones to host its commercial credibility, still other’s deposits to soften its balance-of-payments stress, and someone else’s political goodwill to bridge its financing gaps is not building resilience, butis renting it.

The easy line, after every shock, is that reform remains important. The harder truth is that shocks like this expose why reform keeps being delayed in the first place. External cushions allow the state to postpone hard choices.

The UAE story is one more reminder that such cushions are temporary, contingent, and politically rented. The larger they become, the more vulnerable the economy becomes to bilateral friction.

Pakistan should read the UAE shock accordingly. Not as an isolated financing event, nor as a narrow remittance concern. But as a warning that the old model of external dependence, whether through labour export, bilateral deposits, or offshore intermediation, is becoming too concentrated to remain safe.

Comments