Middle East conflict, Gulf market volatility, and Pakistan’s strategic opportunity

The escalating conflict in the Middle East has placed the Gulf region under intense global scrutiny. The economies of the Gulf Cooperation Council (GCC)—notably Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Bahrain, and Oman—are pivotal to global energy supply, financial markets, and regional stability.

Yet, the Gulf is showing signs of vulnerability, illustrated by recent developments in Dubai’s real estate equities.

Dubai real estate shock

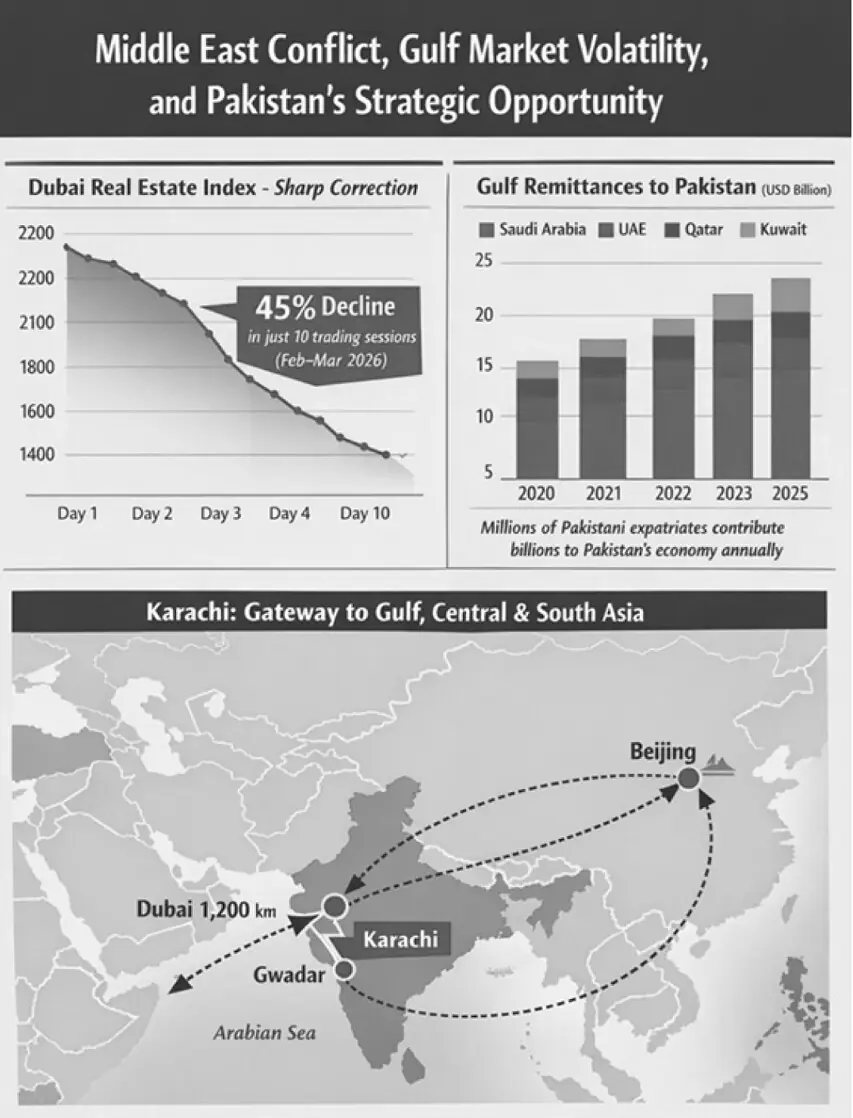

The Dubai Real Estate Index on the Dubai Financial Market has seen a dramatic correction, losing approximately 45% of its value in just ten trading days. This followed a strong rally earlier in the year, driven by speculative investment in property-linked equities.

Profit-taking and shifts in investor sentiment triggered a rapid unwinding of positions, producing one of the fastest sectoral drawdowns in Dubai’s market history.

While Dubai’s property sector continues to benefit from population growth, international interest, and its role as a global business hub, the speed and magnitude of this correction highlight how volatile sector-driven markets can be and the importance of prudent risk management.

Who stands to lose?

Beyond financial markets, a prolonged Gulf slowdown would have far-reaching consequences. Countries heavily dependent on Gulf labour and capital are most exposed. Among these, Pakistan is particularly vulnerable.

Millions of Pakistani expatriates work in the Gulf, sending billions of dollars in remittances annually. These inflows are vital to Pakistan’s economy, supporting households and foreign exchange reserves.

A faltering Gulf economy could therefore result in:

• Reduced employment opportunities for expatriate workers

• Lower remittance inflows

• Declining demand for Pakistani exports and services

• Diminished investment flows from Gulf sovereign wealth funds

Other Asian economies, including India, Bangladesh, and the Philippines, would also face similar pressures due to dependence on Gulf labor markets.

Historical context: Karachi’s strategic potential

Geopolitical disruption has historically reshaped economic geography. In the early 1990s, uncertainty over Hong Kong ahead of its 1997 handover to China prompted Fortune 500 companies to explore alternative regional hubs. Notably, Karachi was considered a prime candidate.

Karachi’s advantages were clear:

• Direct maritime access via one of South Asia’s largest ports

• Proximity to the Middle East, Central Asia, and South Asia

• An established financial sector and stock exchange

• A strategic geographic location connecting major trade corridors

Unfortunately, it was misfortunate that in the 1990s, Karachi became a battlefield for sectarian and ethnic violence. Much of the capital and multinational investment that could have flowed to Karachi instead went to the UAE and other Gulf states, helping them prosper. May God give them more, but it appears that the strategic moment Karachi lost in the 1990s may once again be returning, offering the city and Pakistan a renewed opportunity to reclaim its place as a regional commercial hub.

Although domestic and geopolitical challenges prevented this potential from being fully realized previously, Karachi’s geographic fundamentals remain unchanged.

Pakistan continues to occupy a unique position at the crossroads of South Asia, Central Asia, the Middle East, and Western China, with maritime access through the Arabian Sea. Infrastructure such as Gwadar Port further strengthens its potential as a logistics and connectivity hub.

Could regional instability reopen strategic space?

Prolonged instability in the Gulf could prompt multinational corporations to reconsider regional exposure. Pakistan—and Karachi in particular—could emerge as a natural gateway linking multiple markets across Asia and the Middle East.

The conflict’s trajectory, however, is not purely economic. Strategic analysts are debating scenarios in which Iran could pursue prolonged asymmetric warfare, stretching the conflict to exhaust American and Israeli resolve. Conversely, some scenarios envision dramatic escalation, potentially involving surprise strategic moves by Iran, possibly with tacit support from powers such as Russia and China.

This raises a stark strategic question:

Could Iran’s strategy of prolonging the war ultimately frustrate the United States and Israel into considering extreme military options—including, in theory, nuclear escalation—or might Iran instead attempt a bold strategic maneuver, altering the regional balance of power?

While speculative, these scenarios underscore the profound uncertainty in the region. For Pakistan, which sits astride critical trade routes and energy corridors, the stakes are both high and complex.

Crisis, risk, and opportunity

The current conflict represents a serious geopolitical and humanitarian challenge, with potential ripple effects across Asia and beyond. For Pakistan, the immediate risks are clear, given its economic interdependence with the Gulf. Yet history demonstrates that moments of disruption often create opportunities.

If Pakistan can combine its geographic advantage with political stability, investor-friendly policies, and robust infrastructure, the country could reassert itself as a regional commercial hub. Karachi, with its ports, financial sector, and strategic location, could once again serve as a gateway connecting global trade networks.

The ultimate question is not whether Pakistan has a geographic advantage—it does—but whether it is prepared to seize the strategic moment if the world’s attention shifts once more toward Asia’s emerging gateways.

Copyright Business Recorder, 2026

The writer is the CEO of Securities Exchange Management Suite and a former general manager of Pakistan Stock [email protected]

Comments