Treet Battery Limited (TBL), a listed subsidiary of Treet Corporation Limited (TREET), reported a meaningful financial turnaround in the first half of FY26 (July–December 2025), achieving a net profit after tax of Rs19 million against a net loss of Rs142 million in the same period last year — a full earnings reversal of Rs162 million. At the consolidated level, TREET demonstrated strong broad-based improvement, posting a 6.5 percent revenue uplift to Rs6.9 billion alongside gross margin expansion of 700 basis points and a 32 percent surge in operating profit. These results collectively affirm that the structural turnaround initiated in FY25 is deepening rather than plateauing.

TBL - Revenue & Volume Decline

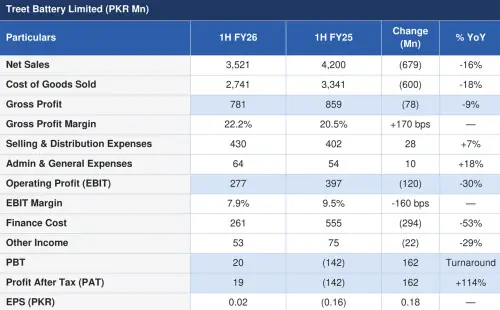

TBL reported net sales of Rs3,521 million in 1HFY26, a decline of 16 percent from Rs4,200 million in 1HFY25. The revenue contraction was predominantly driven by structural demand compression in the backup power (UPS) segment, rather than internal operational failure. A sustained reduction in load-shedding hours across major urban and industrial centers significantly eroded urgency-driven battery replacement demand.

Simultaneously, rapid proliferation of solar installations has fundamentally altered backup power requirements — households transitioning to solar have progressively displaced conventional lead-acid battery backup systems. Structural oversupply in the broader market and reduced consumer purchasing power further constrained the addressable premium segment.

TBL - Gross Margin Improvement

Despite the 16 percent topline decline, cost of goods sold fell 18 percent to Rs2,741 million, resulting in a gross margin improvement of approximately 170 basis points to 22.2 percent from 20.5 percent in the prior period. This reflects favourable raw material dynamics — particularly in lead procurement — alongside enhanced procurement strategies and a deliberate sales mix restructuring that prioritized higher-margin product categories while reducing reliance on lower-margin lines. Cost discipline and organizational restructuring further supported the margin recovery. In absolute terms, gross profit contracted 9 percent to Rs781 million, but the directional margin improvement signals structural cost optimization.

TBL - Operating Profit & Cost Structure

Operating profit declined to Rs277 million from Rs397 million in 1HFY25 — a 30 percent contraction — primarily attributable to the revenue shortfall. Selling and distribution expenses rose 7percent as the company-maintained market investment, while administrative expenses increased 18 percent.

EBIT margin contracted 160 basis points to 7.9 percent. Other operating expenses also almost doubled, reflecting higher warranty provisions linked to the company’s strengthened post-sale service commitments — a strategic investment in customer retention and competitive differentiation as product quality becomes a key battleground.

Finance Cost — Transformative Reduction

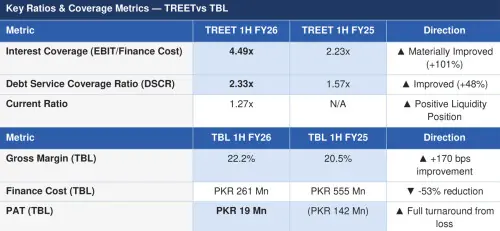

The single most material positive development in TBL’s 1HFY26 results was the 53 percent reduction in finance cost. This reflects the cumulative 1,150 basis point monetary easing cycle since the SBP policy rate peaked at 22 percent, with the rate descending to 10.5 percent by December 2025. The relief from financing charges was instrumental in the company’s earnings reversal from aRs142 million loss to a Rs19 million profit. Management has indicated plans to restructure its ownership and leverage profile in the battery segment.

Profitability vs. Sector Peers

In the context of Pakistan’s battery industry — which continues to navigate demand compression, pricing pressure, and financial cost volatility — TBL’s earnings trajectory distinguishes it from peers. While Exide Pakistan saw PAT decline 95 percent and Atlas Battery reported a 68 percent PAT decline in comparable periods, TBL achieved a full earnings reversal to profitability.

Critically, TBL appears to be managing the industry downturn through margin discipline rather than volume-chasing, maintaining the highest operating margin profile in its peer group. In cyclical industries, earnings direction frequently matters more than absolute scale.

Treet Corporation Limited

Treet Corporation Limited (TREET), the parent holding entity encompassing razor and blade manufacturing, battery operations, pharma (haemodialysis concentrates), packaging, and solar/lithium-ion initiatives, delivered robust consolidated financial performance in 1HFY26, with improvements recorded across revenue, margins, profitability, and balance sheet quality.

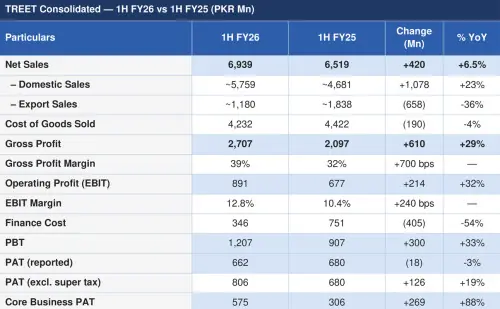

Revenue — Domestic Surge Offsets Export Decline

Consolidated net sales rose 6.5 percent to Rs6,939 million. Domestic sales surged 23 percent year-on-year, contributing approximately 83 percent of total revenue, underpinning the company’s resilient market position and effective execution of domestic sales strategies. Conversely, export sales declined 36 percent year-on-year — a deliberate strategic pricing rationalization to correct long-standing margin pressures rather than market share loss. Blade volumes stood at 796 million units, marginally below 812 million in the prior year (-2% YoY), confirming that revenue growth was driven by price and mix improvement rather than pure volume expansion.

Gross Margin — Core Structural Strength

The standout performance metric was the 700-basis point gross margin expansion to 39 percent, from 32 percent in 1HFY25. Cost of goods sold declined 4 percent year-on-year while gross profit grew 29 percent. Management attributes this to better product mix optimization, pricing discipline, improved cost management, and manufacturing efficiencies — factors that suggest structural rather than cyclical improvement. With a 39 percent gross margin, TREET’s blade and razor segment significantly outperforms its largest historical domestic competitor (Gillette Pakistan operated at approximately 20 percent gross margin in FY25), underlining a durable cost advantage.

Operating Leverage & OPEX

Operating expenses grew 22 percent year-on-year, reflecting strategic investments in brand development (Genesis and Estela launches), higher advertising and promotional spend, ERP system upgradation, and trademark registration fees in export markets.

Despite this OPEX inflation, operating leverage was strongly positive — operating profit rose 32 percent with the EBIT margin expanding 240 basis points to 12.8 percent. Interest coverage doubled, while the Debt Service Coverage Ratio improved, indicating materially improved capacity to service financial obligations from core operations.

Finance Cost & PAT

Finance costs declined 54 percent reflecting the SBP monetary easing cycle and a deliberate reduction in borrowing utilization funded partly by divestment proceeds channelled toward debt repayment. PBT surged 33 percent year-on-year. Reported PAT of Rs662 million was marginally below the prior year’s Rs680 million due to a super tax impact on capital gains. Excluding this one-off, underlying PAT improved to Rs 806 million (11.62% margin), while core business PAT nearly doubled to Rs575 million (8.29% margin vs 4.70% in 1HFY25) — reflecting authentic, operations-driven earnings quality improvement.

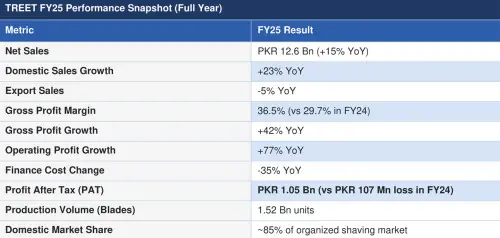

FY25 Performance — Brief Review

FY25 marked TREET’s definitive financial turnaround, erasing the losses incurred during the FY21–FY24 over-leverage and macro-shock cycle. The company reversed aRs107 million loss in FY24 into a Rs 1.05 billion profit after tax — a comprehensive earnings recovery underpinned by revenue growth, margin expansion, and aggressive debt reduction.

Net sales grew 15 percent year-on-year to Rs12.6 billion, powered by a 23 percent domestic revenue increase even as exports softened 5 percent amid global pricing pressures. The gross profit margin expanded from by 700 basis points — as COGS grew only 4 percent, demonstrating strong operating leverage. Finance costs fell 35 percent as the SBP rate easing cycle took effect and the company actively reduced leverage. Operating profit surged 77 percent year-on-year. Production volumes remained stable at 1.52 billion units with an 85 percent domestic market share in the organized shaving segment and export presence across 40+ countries. The FY25 recovery laid the financial and operational foundation for the more ambitious strategic investments now being executed in FY26.

Strategic Developments & Operational Outlook

Genesis & Estela — Premium Segment Entry

TREET’s most significant strategic move entering FY26 is the simultaneous launch of Genesis (men’s premium shaving) and Estela (women’s grooming) — approximately 35 SKUs across the range, with synchronized availability in 800+ retail outlets. Genesis is positioned at the premium tier previously dominated by Gillette, but at approximately 30 percent lower price, targeting the 15–20 percent premium market segment. Estela fills a structurally under-served women’s grooming category in Pakistan. Both launches coincide with Gillette Pakistan’s exit from local manufacturing operations — a market gap that TREET is uniquely positioned to capture with its 85percentplus organized market share, nationwide distribution, and enhanced manufacturing capabilities.

Battery Segment — Lithium-Ion Transition

TBL is actively repositioning its battery business from traditional lead-acid to lithium-ion, having partnered with a major Chinese manufacturer to launch lithium-ion batteries and inverters across approximately five SKUs (including tower and wall-mounted solutions). The strategy is phased: imported solutions first to learn market preferences, followed by local assembly, and eventually domestic battery management system development. The company’s 75-year brand heritage and established distribution network provide a credibility advantage in a warranty-intensive product category where consumer trust in supplier longevity matters significantly. The automotive segment (approximately 60 percent of TBL revenue) continues to provide revenue stability, and TBL holds the number one position by volume in the growing maintenance-free segment.

Cost Efficiency Initiatives

TREET has deployed three structural cost-management levers: (i) solarization — approximately 1.2 MW at the Treet plant and over 2 MW at the battery facility, reducing power costs by more than 50 percent relative to requirement; (ii) localization of components including terminals and plastic parts; and (iii) automation of assembly lines through Industry 4.0 initiatives. These structural cost improvements, combined with ongoing Kaizen and TPM programs, support the sustainability of margin improvements rather than one-off gains.

Export Strategy

Export revenues currently represent approximately 20–30 percent of TREET group revenues, down from a historic 50 percent split as the global market shifted toward system razors where TREET had limited presence. Management targets a return to a 50 percent-plus export contribution within three to five years by bringing handle-making and cartridge assembly in-house through the Genesis platform. China remains a notable export market for TBL blades — a testament to the technological depth of its blade manufacturing capability, which competes against only six to eight global players.

Key Risks & Considerations

Several risk factors warrant investor attention: (i) TBL’s high short-term leverage creates sensitivity to interest rate reversals; (ii) structural demand compression in the backup power segment shows no near-term reversal, placing the burden of revenue recovery on automotive segment growth and the pace of lithium-ion market penetration; (iii) TREET’s export decline of 36 percent in 1HFY26 requires careful monitoring to ensure the strategic pricing rationalization does not become entrenched market share loss; (iv) the Genesis and Estela launches involve significant upfront OPEX investment in a price-sensitive domestic market, with payback timelines dependent on premium category development; and (v) smuggling and counterfeiting — estimated at approximately 20 percent of total shaving product sales — remains a structural headwind to volume and pricing.

Conclusion

The 1HFY26 results for both Treet Battery Limited and Treet Corporation Limited demonstrate that the FY25 turnaround was not cyclical but structural. TREET’s 700 bps gross margin expansion, 32 percent operating profit growth, 54 percent finance cost reduction, and near doubling of core business PAT reflect the compounding benefits of operational discipline, debt deleveraging, and strategic product investment. TBL’s earnings reversal — from Rs142 million loss to Rs19 million profit — against a challenging sector backdrop characterized by lead-acid demand contraction and peer profitability compression, validates a margin-over-volume strategic stance. With brand launches (Genesis, Estela), lithium-ion entry, export re-expansion plans, and a more efficient cost base, the Treet group is building multiple organic growth levers for the medium term. The trajectory warrants continued monitoring of leverage at TBL and the pace of premium segment adoption, but the directional indicators across the group are broadly positive.

Comments