Sazgar Engineering Works Limited (PSX: SAZEW) was incorporated in Pakistan as a private limited company in 1991 and was converted into a public limited company in 1994.

The principal activity of the company is the manufacturing and sale of automobiles, automotive parts and accessories and household electronic appliances.

Pattern of Shareholding

As of June 30, 2025, SAZEW has a total of 60.446 million shares outstanding which are held by 9672 shareholders. Directors, CEO, their spouse and minor children have the majority stake of around 64.53 percent shares of the company followed by local general public holding 12.75 percent shares of the company. Joint stock companies account for 8.92 percent shares of SAZEW while foreign companies hold 7.80 percent shares.

Around 2.61 percent of the company’s shares are held by Modarabas & Mutual Funds and 1.28 percent by Banks, DFIs and NBFIs. The remaining shares are held by other categories of shareholders.

Performance Trail (2019-24)

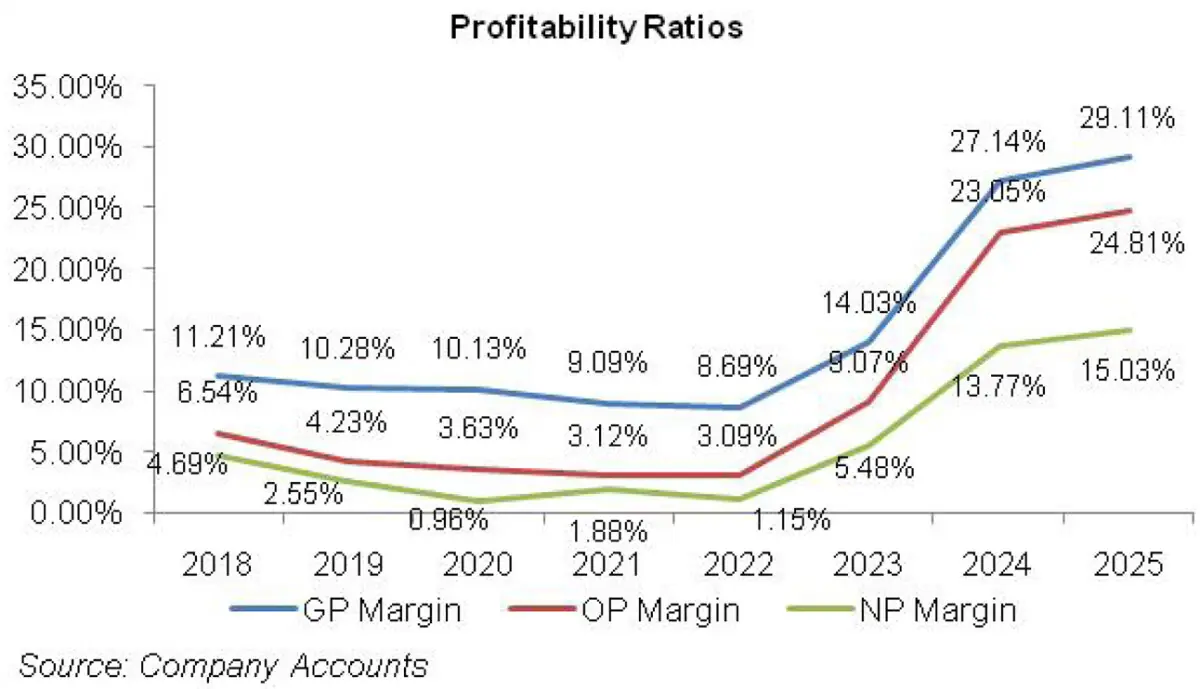

The topline and bottomline of SAZEW which were declining until 2020 registered a massive turnaround thereafter. The gross and operating margins of the company witnessed a downward journey until 2022 followed by a staggering rebound in the following years.

Net margin which dropped until 2020, slightly improved in 2021 only to slide back in 2022. In the subsequent years, net margin also considerably recovered. All the margins attained their optimum level in 2025 (see the graph of profitability ratios).

The detailed performance review of the period under consideration is given below.

In 2019, SAZEW’s topline slid by 18.89 percent year-on-year to clock in at Rs. 3218.523 million. This reflects the decline across the categories – auto rickshaws, automotive parts and home appliances.

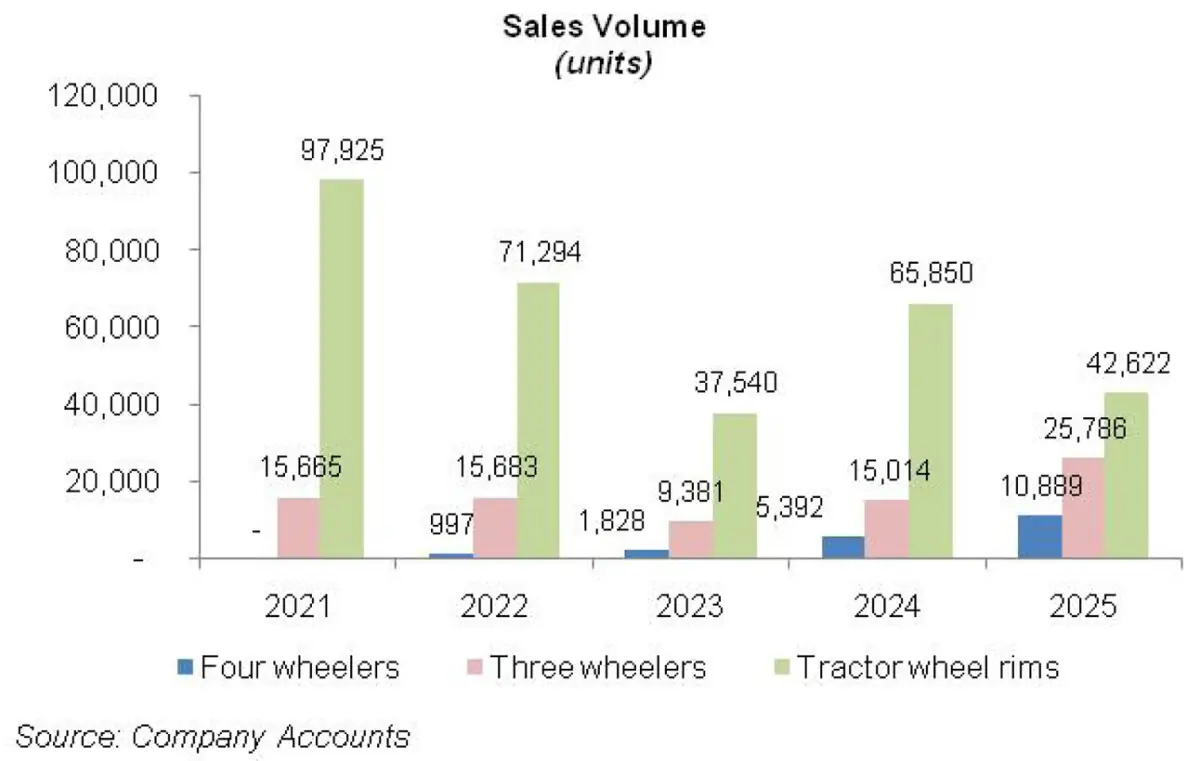

During 2019, SAZEW sold 15,845 units of Auto Rickshaws which were 28 percent lesser than the volume sold in 2018. The curtailed momentum of tractor industry sales also affected the sales of tractor wheel rims which shrank by 32 percent to clock in at 73,395 units.

Sale of home appliances was also affected due to reduced purchasing power of the consumers on account of rising inflation.

To top it off, due to the closure of Pakistan Steel Mills, the company became dependant on imported steel whereby constant depreciation of Pak Rupee resulted in an unabated increase in the prices of raw materials. Gross profit dipped by 25.67 percent year-on-year in 2019 while GP margin fell from 11.21 percent in 2018 to 10.28 percent in 2019.

Distribution expense remained in check due to lesser freight and octroi charges; however, administrative expense rose by 24.97 percent in 2019, depicting an increase in salaries and wages on account of inflation.

Other expense shrank by 57.87 percent year-on-year in 2019 on the back of lower provisioning for WWF, WPPF and doubtful debts. Other income didn’t provide any favor as it contracted by 68.43 percent year-on-year due to lesser reversals of provisions done in 2019.

All in all, the operating profit ticked down by 47.55 percent year-on-year in 2019 while OP margin fell from 6.54 percent in 2018 to 4.23 percent in 2019.

Finance cost multiplied by a whopping 396.26 percent in 2019 due to higher discount rate during the year coupled with long-term loans obtained for the four wheeler project and increased utilization of short-term borrowing facility.

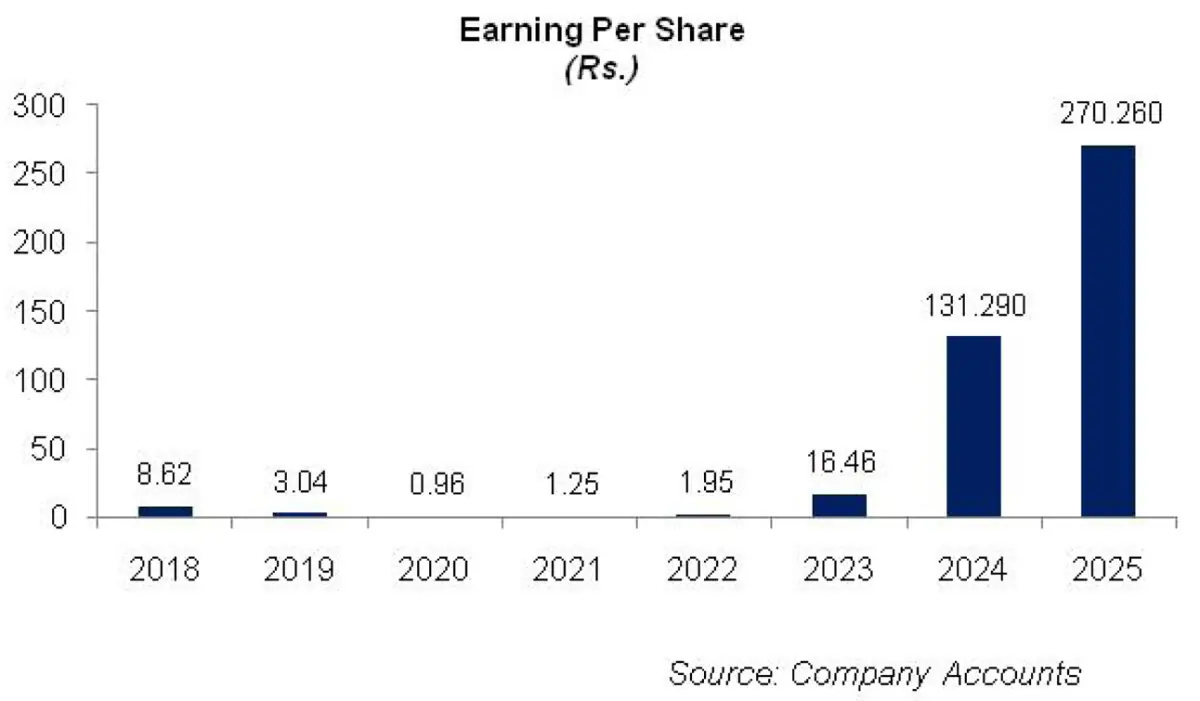

The bottomline went down by 55.92 percent year-on-year to clock in at Rs.81.999 million in 2019 with NP margin of 2.55 percent versus NP margin of 4.69 percent in 2018. EPS stood at Rs.3.04 in 2019 from Rs.8.62 in 2018.

In 2020, SAZEW topline further shrank by 10.15 percent year-on-year to clock in at Rs.2891.754 million. Owing to the outbreak of COVID-19, automobile sector badly suffered which had its affect on the sales of SAZEW. Not only did the sale of four wheelers and automotive parts decreased during 2020, severe economic headwinds also took its toll on the sales of three wheelers and home appliances. The off-take of three wheelers nosedived to 12,274 units in 2020, reflecting a 22.5 percent year-on-year drop.

Due to low capacity utilization and curtailed sales, cost of sales also inched down by 10 percent year-on-year in 2020. Gross profit contracted by 11.40 percent year-on-year while GP margin slightly dropped to 10.13 percent in 2023.

Operating expense rose up not only due to increase in the salaries and wages but also due to increased advertising and promotion budget as the company launched a new model of Cargo Loader during 2020 with three variants. Other expense contracted by 44.72 percent in 2020 due to lesser provisioning done for WWF and WPPF on account of reduced profitability.

Other income posted a staggering growth of 309.44 percent in 2020 on account of profit on Islamic banking deposits and gain on sale of fixed assets. However, this couldn’t prevent the operating profit from shrinking by 22.99 percent in 2020. OP margin also fell to 3.63 percent in 2020.

Finance cost surged by 163.71 percent due to increased borrowings during 2020 and higher discount rate for most part of the year.

Net profit lessened by 66.30 percent year-on-year in 2020 to clock in at Rs.27.636 million with NP margin of 0.96 percent. EPS weakened to Rs.0.96 in 2020.

After experiencing the successive years of lackluster demand, 2021 brought silver lining for SAZEW as its revenue grew by a stunning 39.49 percent to clock in at Rs.4033.61 million in 2021. The sales growth came on the back of a robust rise in the demand of three wheelers, four wheelers and tractor wheel rims while the sale of home appliances inched down.

The topline growth was also the result of price increase as the company had to pass on certain effect of increase in iron prices to the customers. Due to exorbitant raw material prices, GP margin declined to 9.09 percent despite 25.16 percent growth in gross profit.

Operating expense grew significantly due to increase in ocean freight charges as well as salaries expense. Higher profit related provisioning inflated operating expense by 48.72 percent in 2021. Other income also improved by 17.66 percent in 2021 due to higher profit from Islamic bank deposits.

Operating profit grew by 19.87 percent year-on-year in 2021 while OP margin dwindled to 3.12 percent. A tremendous support to the bottomline was provided by finance cost which plunged by 66.93 percent year-on-year on the back of lower borrowings and downward revision in discount rate.

The result was a 174.28 percent year-on-year rise in bottomline which clocked in at Rs.75.799 million in 2021. NP margin also slightly improved to 1.88 percent in 2021 while EPS stood at Rs.1.25.

In 2022, SAZEW posted topline growth of 154.72 percent which culminated into the record high sales revenue of Rs.10.274 billion. The robust topline was the result of the success of the company’s four wheeler project during 2022 which multiplied by 245.38 times in 2021 to reach Rs.5.46 billion. During the year, SAZEW introduced a four wheeler under the brand name of “BAIC” which played a pivotal role in achieving robust topline growth in 2022. The sales of three-wheeler also buttressed the topline while home appliances and tractor wheel rims category didn’t perform well.

Extraordinarily high prices of iron coupled with Pak Rupee depreciation drove the cost of sales up by 155.84 percent. While gross profit grew by 143.49 percent year-on-year in 2022, GP margin shrank to 8.69 percent. Record high inflation, steep rise in freight charges as well high advertising budget resulted in 131.42 percent taller operating expense incurred in 2022. Other expense also posted a sizeable increase of 82.25 percent on account of higher provisioning for WPPF.

While operating profit posted 152.51 percent boost, OP margin slipped to 3.09 percent in 2022. Finance cost which provided an ultimate breather to the bottomline in 2021, turned ruthless yet again in 2022 with multiple upward revisions in discount rate during 2022. This suppressed the growth momentum of bottomline which grew up by 55.46 percent in 2022 to clock in at Rs.117.84 million in 2022. NP margin lessened to 1.15 percent in 2022 while EPS moved up to Rs.1.95.

After an overwhelming sales and profit achieved by the company in 2022, the subsequent year proved to be even more encouraging as not only did the topline grow by 76.89 percent year-on-year in 2023, its bottomline and margins multiplied staggeringly. SAZEW’s net sales clocked in at Rs.18,174.297 million in 2023. The topline growth was the result of vigorous performance by the four wheeler segment.

The sales of four-wheeler multiplied by 83.35 percent year-on-year in 2023 to clock in at 1828 units. Conversely, the sales volume of three-wheelers and tractor wheel rims dropped by 40.18 percent and 47.34 percent respectively to clock in at 9,381 units and 37,540 units respectively in 2023. During 2023, the company also commenced the production of SUV vehicles and also introduced hybrid electric vehicles in the local market by the brand name of “HAVAL”. Despite high prices of raw materials, which were further fueled by Pak Rupee depreciation, gross profit magnified by 185.51 percent in 2023 while GP margin inclined to 14.03 percent from 8.69 percent in 2022.

Distribution expense grew by 37.28 percent in 2023 due to higher freight and octroi charges, commission, travelling & conveyance charges incurred and also because of provision for warranty claims booked during the year. Administrative expense also hiked by 61.87 percent in 2023 due to higher payroll expense as SAZEW’s workforce grew from 1117 employees in 2022 to 1197 employees in 2023. Other expense spiked by 496.29 percent in 2023 due to tremendous rise in profit related provisioning.

Other income acted favorably and grew by 65.68 percent year-on-year in 2023 on the back of higher profit from Islamic banking deposits. Operating profit multiplied by 419.72 percent in 2023 while OP margin also surged to 9.07 percent from OP margin of 3.09 percent recorded during last year. Finance cost escalated by 211.45 percent in 2023 on account of unprecedented level of discount rate. This was despite the fact that the company paid off all its short-term liabilities during the year and considerably reduced its long-term borrowings. SAZEW’s net profit improved by 744.44 percent to clock in at Rs.995.077 million in 2023 with EPS of Rs.16.46 and NP margin of 5.48 percent.

In 2024, SAZEW’s net sales grew by 217.16 percent year-on-year to clock in at Rs.57,642.469 million. The growth was primarily supported by the rising demand of the company’s flagship HAVAL SUV vehicles. The sale of four-wheelers registered a staggering growth of 194.97 percent in 2024 to clock in at 5,392 units. This was coupled with 60 percent growth recorded in the sales of three wheelers which clocked in at 15,014 units and 75.41 percent growth recorded in the sales of tractor rims which was recorded at 65,850 units in 2024. During the year, the company also exported its three-wheelers to Japan, Liberia, Tanzania and Afghanistan.

Besides impressive sales volume, the company was also able to pass on the impact of cost hike to its consumers, particularly in the four wheeler category. This is evident from an unparalleled GP margin of 27.14 percent recorded by SAZEW in 2024. In absolute terms, gross profit strengthened by 513.71 percent in 2024. Distribution expense multiplied by 207.72 percent in 2024 mainly on the back of higher sales commission, freight & octroi charges, increased salaries of sales force, provision for warranty claims as well as increased advertising & promotion budget allocated for the year.

Administrative expense surged by 59.87 percent in 2024 on account of elevated payroll expense which was the result of high inflation as well as expansion of workforce from 1197 employees in 2023 to 1392 employees in 2024. Other expense mounted by 876.36 percent in 2024 due to massive provisioning done for WWF and WPPF. Higher other expense was almost offset by 2637.67 percent stronger other income recorded by the company in 2024. This was the result of sale of scrap, rectification charges as well as gain recognized on the sale of fixed assets in 2024. SAZEW posted 705.51 percent healthier operating profit in 2024 with OP margin of 23 percent.

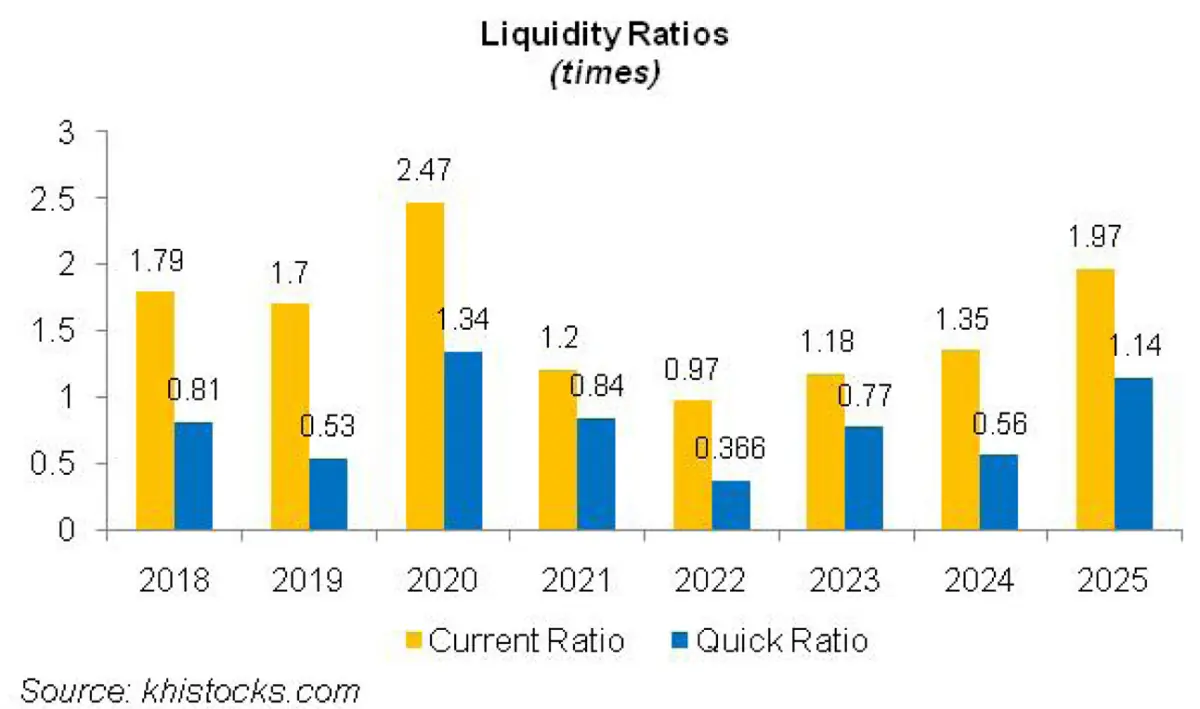

Despite soaring discount rate, SAZEW’s finance cost grew by only 0.66 percent in 2024. This was because the company had no outstanding short-term borrowings as of June 30, 2024. Its long-term financing under Musharakah arrangement also significantly declined during the year. With huge amount of cash & balances, the company has a gearing ratio of 0 percent as of June 30, 2024. Net profit grew by 697.49 percent to clock in at Rs.7935.676 million in 2024. This translated into EPS of Rs.131.29 and NP margin of 13.77 percent in 2024.

In 2025, SAZEW recorded 88.57 percent growth in its net sales which clocked in at Rs.108.694.500 million. This was on the back of economic stability achieved during the year. Not only did lower inflation and down ticking discount rate provided growth momentum to automobile sales, vehicle prices also remained stable due to appreciation of Pak Rupee. The government also emphasized on promoting New Energy Vehicles (NEV) to curtain oil import and to support environmental sustainability. SAZEW’s three wheeler and four wheeler categories posted 71.75 percent and 101.95 percent growth in sales volume in 2025 (see the graph of sales volume).

The phenomenal growth in four wheeler category was mainly backed by the sale of HAVAL vehicles. Tractor sales volume dipped by 35.27 percent in 2025 due to weaker demand. Automotive parts segment also remained lackluster during the year due to lower demand of tractor wheel rims. Conversely, home appliances division (marketed under the brand name “Whirlpool”) boasted considerable growth in 2025. Cost of sales surged by 83.48 percent in 2025 due to inflationary pressure and elevated energy tariff, however, the company was able to record 102.23 percent growth in its gross profit in 2025 with GP margin attaining its optimum level of 29.11 percent.

Improved GP margin was primarily the consequence of higher margins attained in the four-wheeler category. 91.86 percent higher distribution expense recorded during the year was the result of higher freight charges, sales commission, advertising & promotion expense, provision for warranty claims and increased salaries of sales force incurred. Administrative expense also mounted by 46.18 percent in 2025 due to higher payroll expense which was due to inflationary pressure as well as workforce expansion from 1392 employees in 2024 to 1552 employees in 2025.

Higher profit related provisioning culminated into 99.31 percent bigger other expense recorded in 2025. However, it was nearly offset by 62.79 percent higher other income recorded during the year which was the result of higher profit on bank deposits. The company’s bank deposits tremendously grew from Rs.7.76 billion in 2024 to Rs.16.596 billion in 2025. SAZEW recorded 103 percent higher operating profit in 2025 with OP margin of 24.81 percent. Finance cost escalated by 36.34 percent in 2025 due to higher bank charges and increased discount rate. The company didn’t have any short-term borrowings on its books as of June 30, 2025. Its long-term borrowings in the form of diminishing Musharakah facility also considerably shrank during the year. The company has 0 percent gearing ratio as its outstanding borrowings are completely offset by its cash & ban balances. Net profit grew by 105.86 percent to clock in at Rs.16,336.202 million in 2025. This translated into EPS of Rs.270.26 and NP margin of 15 percent in 2025.

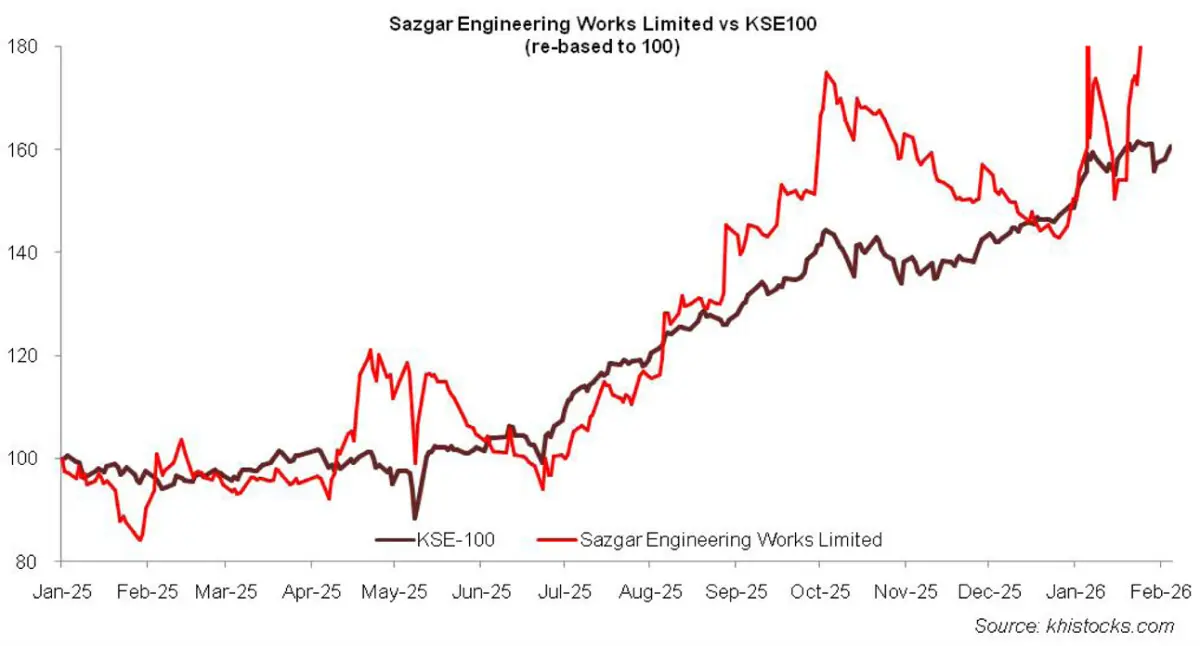

Recent Performance (1HFY26)

During the first half of the ongoing fiscal year, SAZEW posted 51.80 percent stronger topline to the tune of Rs.67,845.86 million. During the period under consideration, sustained economic stability led to improved consumer confidence resulting in the rebound of automobile industry. SAZEW recorded 39.32 percent higher sales volume in the four wheeler category which clocked in at 7700 units in 1HFY26. Conversely, three wheeler segments posted a dip of 6.84 percent in its sales volume which clocked in at 11,952 units in 1HFY26. Tractor wheel rims volume also plunged by 3.84 percent to clock in at 22,163 units in 1HFY26. Cost of sales surged by 60.34 percent in 1HFY26 due to higher raw material prices particularly energy tariff. Gross profit improved by 30.57 percent in 1HFY26; however GP margin dipped to 24.69 percent from 28.70 percent recorded in 1HFY25.

Higher sales volume of four wheeler, continuous expansion of operations and introduction of new models and variants resulted in 61.38 percent elevated distribution expense and 80 percent higher administrative expense in 1HFY26. Increased provisioning for WWF and WPPF appears to be the cause of 27.95 percent greater other expense recorded in 1HFY26. Other income strengthened by 66 percent in 1HFY26 seemingly due to higher profit of bank deposits. While discount rate was curtailed during the period, the company’s bank balances kept attaining new heights to clock in at Rs.25.226 billion as of December 31, 2025 versus Rs.16.596 billion recorded as of June 30, 2025.

SAZEW’s operating profit grew by 27.75 percent in 1HFY26 with OP margin clocking in at 20.69 percent versus OP margin of 24.58 percent recorded in 1HFY25. Finance cost soared by 33.15 percent in 1HFY26 due to higher bank charges and increased borrowings. While the company didn’t have any short-term liabilities on its books until June 30, 2025, it obtained short-term loan of Rs.3.316 billion during the period under consideration to meet its working capital requirements. SAZEW posted net profit of Rs.8440.565 million in 1HFY26, up 27.40 percent year-on-year. This translated into EPS of Rs.139.64 and NP margin of 12.44 percent in 1HFY26 versus EPS of Rs.109.60 and NP margin of 14.82 percent recorded in 1HFY25.

Future Outlook

The marvelous profitability and margins posted by the company in the recent quarters speak volumes of the fact that its SUVs and hybrid EVs are well received by the market. More than 80 percent of the company’s revenue comes from the sales of its four wheelers. Ever since the introduction of its models, BAIC and HAVAL, the financial performance of the company has reached new unparalleled heights.

With the improvement in macroeconomic indicators – declining inflation, discount rate and stability of Pak Rupee - gradual recovery is also seen in the automobile sector which is expected to continue in the near term. The company is also eyeing export market and has also approved the expansion of its four wheeler manufacturing facilities to meet the growing demand. SAZEW successfully launched its CKD Plug-In-Hybrid Electric Vehicle (PHEV) HAVAL H6 1.5L on August 16, 2025 with the plan to roll out TANK-500 and CANNON PHEVs by March 31, 2026.

While the concessions provided to the new entrants under the Auto Policy 2016-21 are ending in June 2026, the relaxation of used car imports (subject to 40 percent regulatory duty) may challenge the volumes of locally produced vehicles.

Comments