The bonanza of inward home remittances continues, as inflows jumped by 11 percent in 7MFY26 to $23.2 billion. The remarkable part is that growth is coming off a high base, as remittances had already grown by 32 percent in the same period last year.

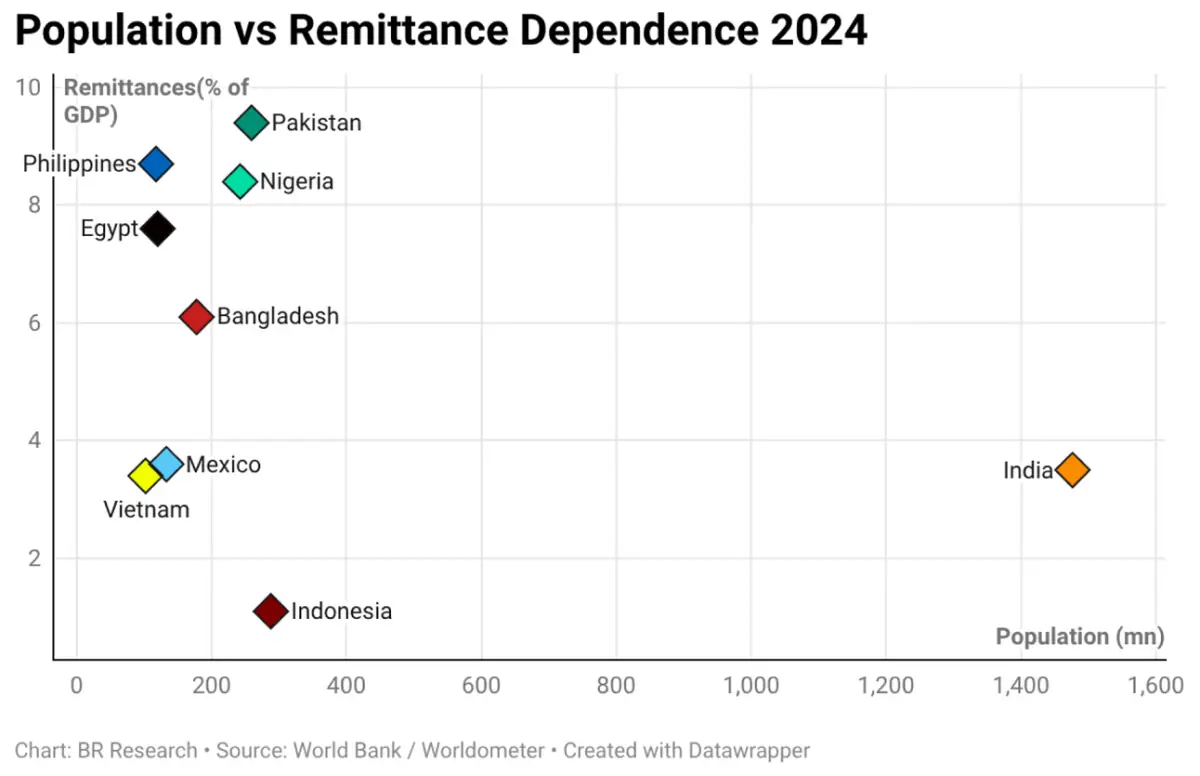

At this pace, annual inflows may touch $42 billion—around 10 percent of GDP—which would be the highest among countries with a population of 100 million or more.

READ MORE: Jul-Jan FY26: Workers’ remittances post 11pc growth

Although there is a growing urge among the masses (especially the middle class) to move abroad, the actual numbers are not astronomically high. In 2025, 762k people left Pakistan for work purposes, which is still below the peak of 947k recorded in 2015.

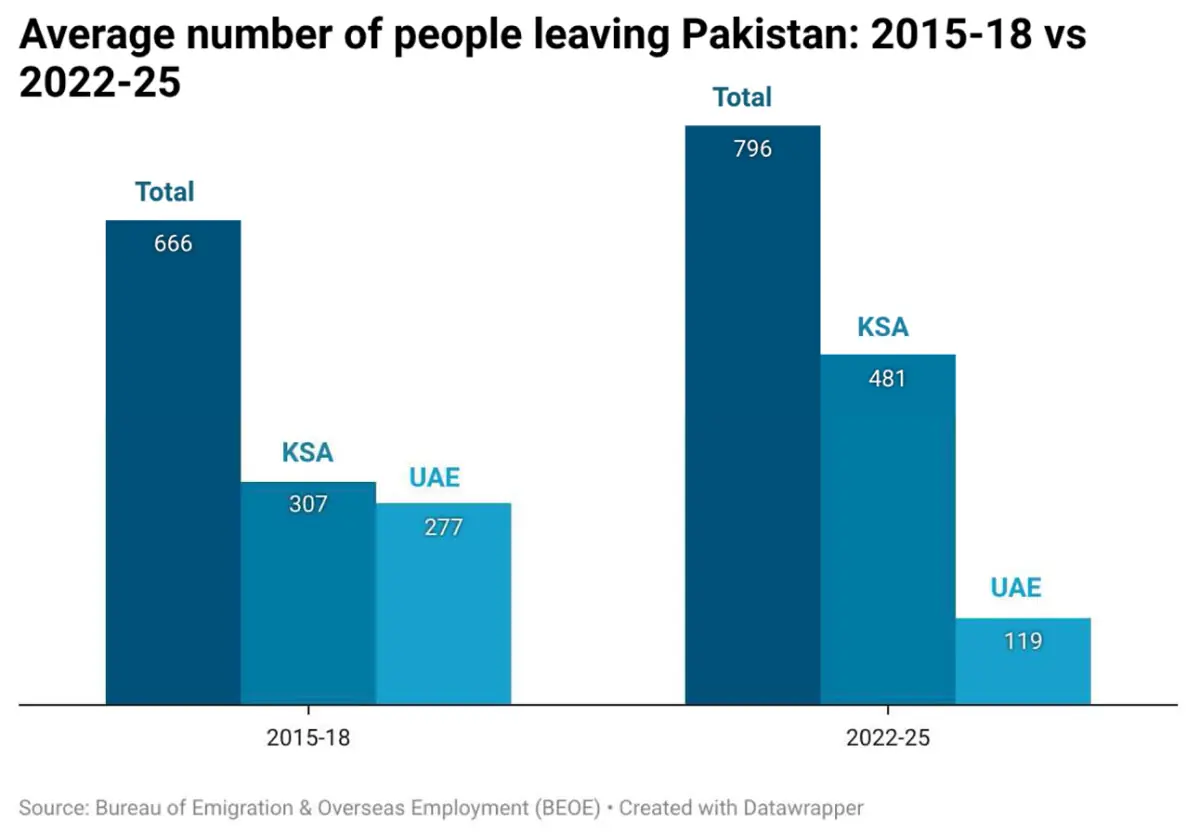

Overall, the number of people leaving annually averaged 774k in 2022–25, compared to 666k in 2015–18. This suggests that the overall exodus has indeed accelerated in recent years.

A more interesting—and intuitive—development is the sharp rise in the number of educated professionals leaving the country in search of better prospects. For example, during 2022–25, an average of 3,641 doctors left Pakistan annually, which is 69 percent higher than the average in 2015–18. Similarly, the outflow of engineers increased by 41 percent over the same period, compared to an overall increase of 18 percent in total emigrants.

One may wonder whether these emigrants are sending higher amounts, as remittance growth is clearly outpacing the increase in the number of people leaving. However, that may not be the case. For instance, remittances from the UAE jumped by 54 percent in 7MFY25 and then grew by another 14 percent in 7MFY26, despite the high base. Meanwhile, the number of people going to the UAE has fallen sharply—from 230k in 2023 to roughly a quarter of that, averaging only 58k in 2024 and 2025.

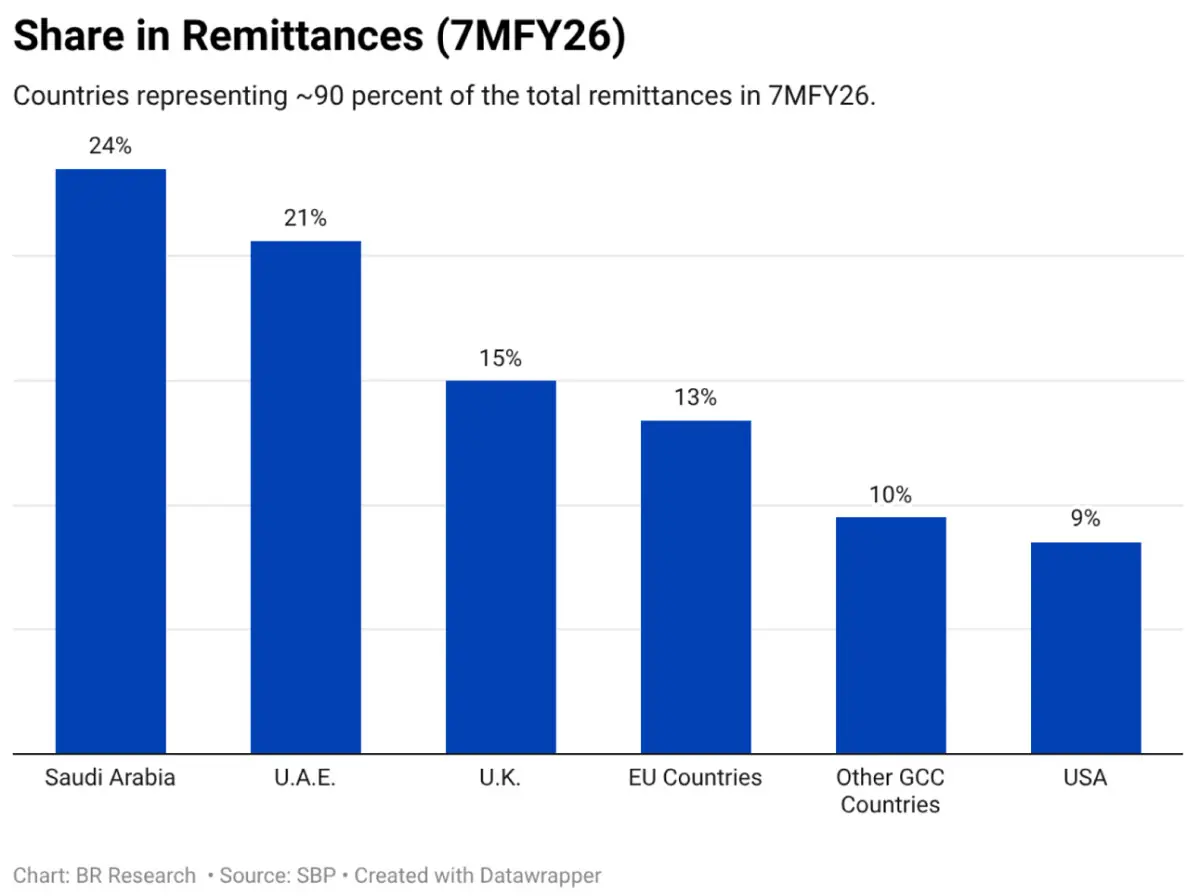

Today, the UAE contributes 21 percent of total remittances, and its exceptional growth stands in sharp contrast to the declining number of people moving to the Emirates. Clearly, there is more to the story.

One obvious explanation is the shift of remittances from informal to formal channels, driven by a crackdown on smuggling and illegal money-transfer routes, as well as stronger incentives for banks to attract formal inflows. Another possibility is that people are moving income (and wealth) to the UAE and sending back smaller amounts periodically for household consumption in Pakistan.

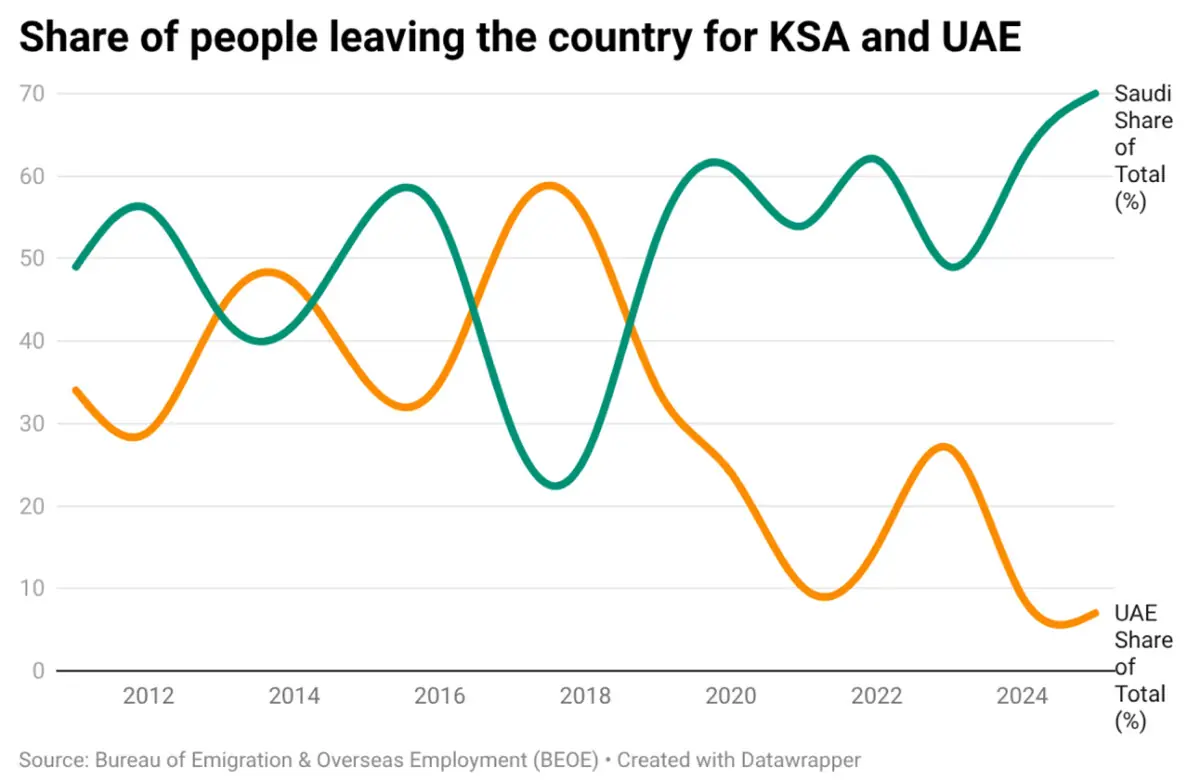

On the other hand, the number of people going to Saudi Arabia is rising at a much faster pace. During 2022–25, an average of 500k people went there annually—62 percent higher than the annual average in 2015–18. In contrast, the number of people going to the UAE declined by 70 percent over the same period.

Beyond economic demand in host countries, there is also a geopolitical angle to the changing pattern of worker destinations. For example, after Pakistan refused to send forces to Yemen in 2015, there was a significant decline in the number of people going to Saudi Arabia—falling by 35 percent, from an annual average of 366k during 2012–15 to 236k. Now, with improved relations, around 491k people annually have gone to Saudi Arabia over the last two years. Meanwhile, the number of people going to the UAE has fallen, partly due to visa-related issues, while geopolitical frictions may also be playing a role.

In 7MFY26, 45 percent of remittances are coming from Saudi Arabia and the UAE alone. This creates concentration risk, as history suggests that any geopolitical shift can materially impact inflows. The risk becomes more serious as reliance on remittances increases to finance imports, since remittances are a key factor in containing the current account deficit.

In 2025, remittances were almost a quarter higher than goods exports and nearly equal to total exports of goods and services combined. As a share of GDP, remittances are approaching 10 percent—again, the highest among countries with populations above 100 million. This is more than twice India’s level and 50 percent higher than Bangladesh’s. Pakistan has now even surpassed the Philippines.

These risks highlight the need to diversify foreign exchange earnings toward goods and services exports. Goods exports remain in poor shape, while services exports are growing at a healthy pace but are still only around a quarter of remittance inflows.

The government and the SBP can take comfort in the continued rise in remittances, which is supporting currency stability and fuelling consumption-led growth. At the same time, policy must increasingly focus on diversification.

Comments