Pakistan’s E&P sector entered FY26 under pressure from lower oil prices, constrained gas offtake, and declining finance income, with sector earnings in 2QFY26 estimated to fall by around 16% year-on-year.

While oil production grew by about 4%, gas volumes declined by a similar margin due to weak demand from power and fertilizer sectors. At the same time, increased exploration activity and frontier discoveries have strengthened medium-term production prospects but added volatility to costs and near-term earnings.

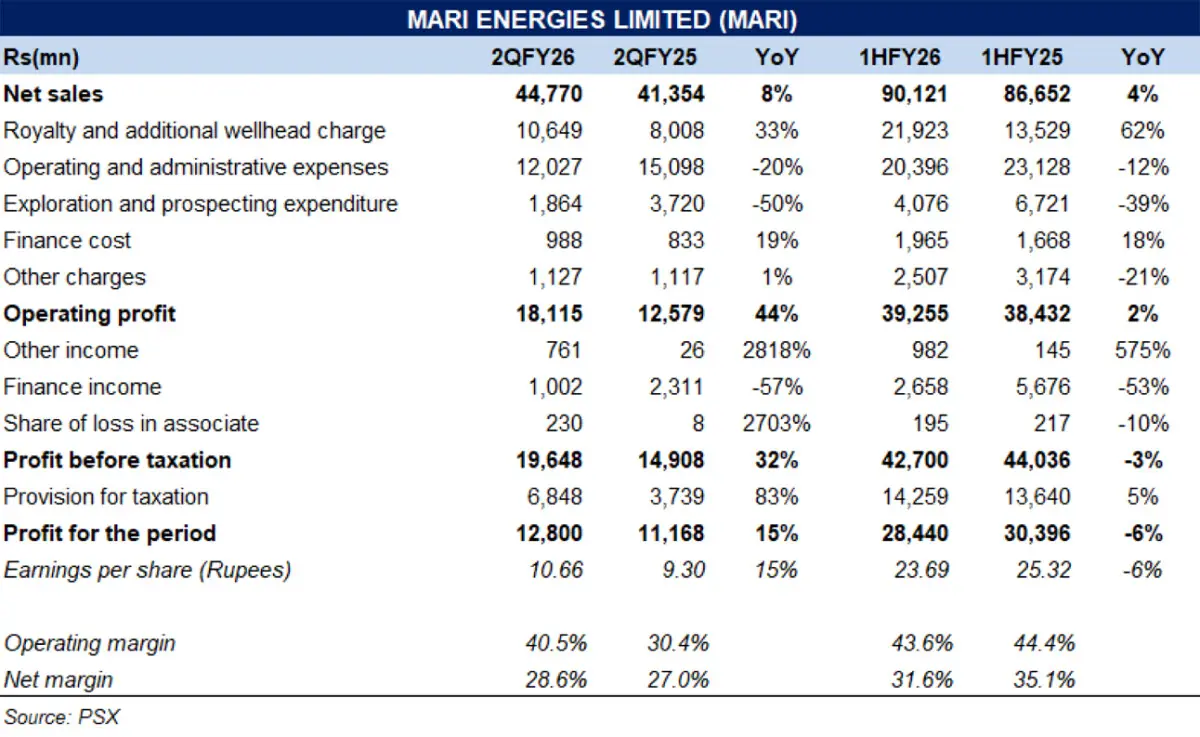

Against this backdrop, Mari Energies Limited (MARI) posted a mixed yet resilient 1HFY26 performance, with modest revenue growth offset by rising royalties, lower finance income, and shifting production dynamics.

MARI reported net sales growth of 4 percent year-on-year in 1HFY26. Despite the topline growth, profitability weakened, with earnings dipping by 6 percent year-on-year. The divergence between revenue growth and earnings decline highlights thepressures facing the company—particularly higher royalty payments, elevated operating costs, and reduced finance income.

In absolute terms, profit after tax declined to Rs28.4 billion in 1HFY26 from Rs30.4 billion in 1HFY25, while gross margins narrowed to 53 percent from 58 percent, and net margins fell to 32 percent from 35 percent.

Royalty expenses emerged as the most significant drag on profitability, rising by 62precent year-on-year to Rs21.9 billion in 1HFY26. This increase reflects the full-period impact of additional royalty on the Mari D&P lease, which structurally raises the company’s cost base.

At the operational level, Mari’s performance was shaped by a mixed production profile. Oil output increased modestly, while gas production remained constrained due to lower offtake from fertilizer plants and operational disruptions at key reservoirs.

In 2QFY26 specifically, earnings rose 15 percent year-on-year, driven by a combination of higher oil production, a 20 percent reduction in operating expenses, and a 50 percent decline in exploration costs. However, finance income declined sharply due to lower interest rates, reduced cash balances, and exchange losses, reinforcing a broader sector trend of shrinking non-core earnings.

Despite near-term earnings pressures, MARI continues to strengthen its long-term growth profile through exploration and portfolio expansion. The company is actively pursuing new block acquisitions and frontier exploration, with potential upside from gas ramp-up.

Additionally, MARI’s planned investment in Mari Minerals reflects a strategic move toward diversification, although its financial impact is likely to remain long-term rather than immediate.

MARI’s earnings trajectory will depend on three critical variables: gas allocation policy, exploration success, and macro-financial conditions.In the near term, the company faces structural headwinds from constrained gas demand, rising royalty burdens, and declining finance income. These factors are likely to keep earnings growth muted despite incremental production gains.

However, the medium-term outlook appears more constructive. Continued exploration activity, frontier discoveries, and potential gas finds from new reservoirs could materially improve production volumes and revenue visibility.

Comments