Roshan Packages Limited (PSX: RPL) was incorporated in Pakistan as a private limited company in 2002 and was converted into a public limited company in 2016. The principal activity of the company is the manufacturing and sale of corrugation and flexible packaging material.

Historical Performance (2019-24)

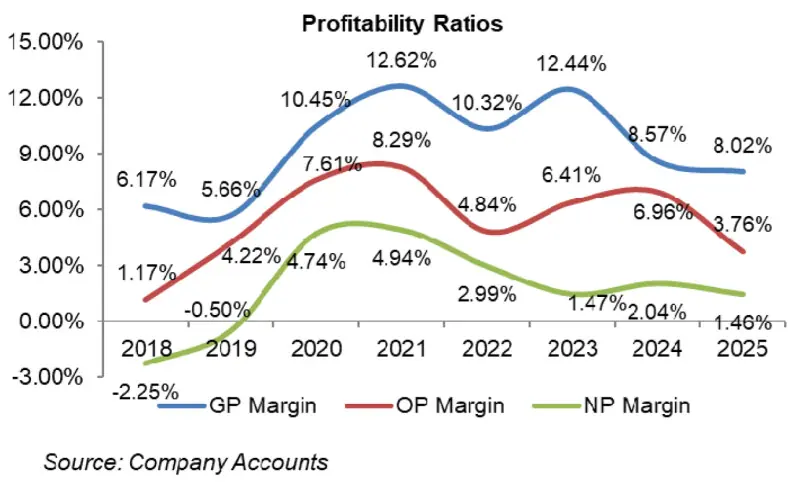

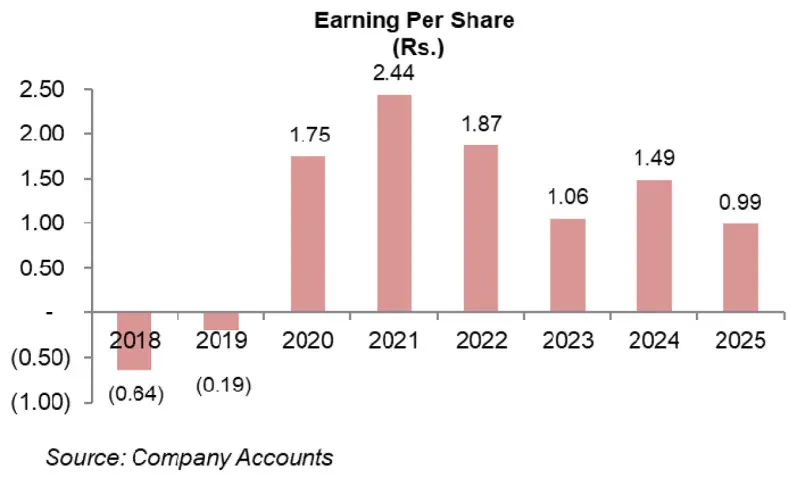

RPL delivered strong topline growth of 34 percent year-on-year to Rs 5.4 billion, driven by 18.7 percent volume growth to 39,012 MT and improved capacity utilization at the corrugation and flexible plants. Operating profit surged, lifting the operating margin to 4.2 percent, but higher finance costs and taxes kept the company in a net loss of Rs 27 million (loss per share: Rs 0.19), though losses narrowed sharply from 2018.

COVID disruptions led to a 3 percent year-on-year decline in revenue to Rs5.2 billion and an 8 percent drop in volumes. However, aggressive cost rationalization boosted the gross margin to 10.5 percent and operating margin to 7.6 percent. RPL returned to profitability, posting net profit of Rs 248 million with a net margin of 4.7 percent (earnings per share: Rs1.75).

A strong post-COVID rebound lifted revenue by 34 percent year-on-year to Rs7.0 billion, supported by higher packaging demand from e-commerce and food delivery. Margins peaked, with gross margin at 12.6 percent and operating margin at 8.3 percent, while lower interest rates reduced finance costs. Net profit rose 39 percent year-on-year to Rs 306 million (earnings per share: Rs2.44).

Revenue grew 27 percent year-on-year to Rs8.9 billion on higher dispatches (44,884 MT) and improved pricing. However, rupee depreciation, higher imported raw-material costs, rising energy tariffs, and a sharp increase in finance costs compressed margins.

Net profit declined 23 percent year-on-year to Rs 265 million, with net margin falling to 3.0 percent (earnings per share: Rs1.87).

Topline growth slowed to 16 percent year-on-year to Rs 10.2 billion, while volumes declined as RPL focused on top-tier customers. Inflationary pressures and aggressive monetary tightening pushed finance costs up 90 percent year-on-year, dragging net profit down 43 percent to Rs150 million. Operating margins recovered somewhat to 6.4 percent, but net margin slipped to 1.5 percent (earnings per share: Rs1.06).

Revenue remained largely flat at Rs10.3 billion (up 0.9 percent year-on-year) amid weak demand, but profitability improved. Lower exchange losses, stronger other income, cost controls, and deleveraging reduced finance costs, lifting net profit by 41 percent year-on-year to Rs211 million. Operating margin improved to 7.0 percent, gearing fell to 8 percent, and earnings per share recovered to Rs1.49.

RPL in FY25 and beyond

Roshan Packages Limited delivered a mixed but stabilizing performance in FY25, navigating a difficult macroeconomic and industry environment marked by subdued demand, cost pressures, and limited pricing flexibility. The company reported net revenue of Rs9.66 billion for the year, down from Rs10.33 billion in FY24, reflecting a year-on-year decline of around 6.5 percent. The contraction in topline was largely volume-driven across both corrugated and flexible packaging segments, as customers remained cautious amid slower economic activity. Despite this, revenue resilience was notable given the inflationary backdrop, indicating that the slowdown stemmed more from demand softness than aggressive price competition.

Profitability remained under pressure at the gross level. Gross margins eased to 8.0 percent compared to 8.6 percent in FY24, as higher input costs—particularly kraft paper and polymer-linked raw materials—could not be fully passed on to customers. Lower capacity utilization also weighed on cost absorption. Even so, margins remained broadly in line with sector norms, suggesting that RPL managed to defend its pricing position relative to peers in a competitive market.

Operating performance softened. Operating expenses increased, driven by higher administrative and employee-related costs, continued investments in quality, compliance, and sustainability initiatives, and general inflation in utilities and services. However, tighter control over selling and distribution expenses helped partially offset these pressures, preventing a sharper erosion in operating profitability.

At the bottomline, the year was characterized by stabilization rather than growth. Profit before tax declined to Rs240 million from Rs419 million, reflecting weaker operating earnings. However, a significant reduction in finance costs—supported by lower leverage and easing interest rates—along with normalization in the tax charge, helped cushion the impact. As a result, profit after tax stood at Rs141 million, while earnings per share came in at Rs0.99 compared to Rs1.49 in FY24. Although earnings declined year-on-year, the company remained firmly profitable, avoiding the volatility seen in earlier downcycles.

Operationally, Roshan Packages continued to leverage its diversified manufacturing footprint, spanning corrugated packaging facilities in Lahore and Karachi, flexible and co-extruded film plants in Lahore, and a paper mill subsidiary that provides partial backward integration. This structure supports supply reliability, cost control, and nationwide customer coverage. The company also maintained focus on sustainability and efficiency, expanding solar energy usage to reduce reliance on grid power, strengthening FSC Chain of Custody compliance, and increasing the use of recycled and upcycled materials. These initiatives not only support cost optimization over the medium term but also enhance the company’s positioning with environmentally conscious customers and export-oriented clients.

Looking ahead, the outlook for Roshan Packages hinges on a gradual recovery in domestic demand and improved capacity utilization. While near-term pricing power is likely to remain constrained, any normalization in volumes could support margin recovery through better fixed-cost absorption. Lower finance costs and a disciplined balance sheet provide downside protection, while ongoing investments in sustainability, energy efficiency, and product differentiation offer longer-term upside. Overall, FY25 can be seen as a year of consolidation, with the company prioritizing resilience and operational stability, setting the base for a more meaningful earnings recovery as market conditions improve.

Comments

Comments are closed for this article.